Europe's door to Chinese tech investment is still ajar

Europe has learned to block Chinese acquisitions of strategic assets. Chinese factories in Europe now pose harder economic security challenges.

Europe has become more alert to the risks posed by Chinese foreign direct investment (FDI) in sensitive technologies. The 2010s were a European garage sale of high-tech firms to China, enabling Chinese investors to acquire intellectual property, know-how and supply-chain leverage. That era is ending. Following a wave of takeovers of semiconductor companies – including Silex, Okmetic, LFoundry and Nexperia – many member-states strengthened their screening mechanisms. Large member-states and the UK have since blocked or unwound numerous Chinese acquisitions, particularly after Beijing supported Russia’s invasion of Ukraine in 2022.

Europe has become more alert to the risks posed by Chinese FDI in sensitive technologies.

The EU has reinforced national action with a tighter FDI screening framework and is preparing legislation to condition certain greenfield investments – where Chinese firms build plants directly in Europe – on technology transfer. Europe is pulling in two directions: restricting Chinese takeovers in high-tech sectors while seeking Chinese capital in areas where it lags, such as batteries. The challenge is to close the remaining loopholes without deterring investment that could strengthen Europe’s industrial base. The EU and the UK must bolster screening capacity, focus on transactions posing genuine security risks, and develop tools to address vulnerabilities stemming from greenfield investment.

A flurry of legislative action

In December 2025, the European Parliament and the Council of Ministers reached a political agreement on tightening the EU’s FDI screening framework. This marks the first substantial overhaul of the regulation, which since 2020 had left screening optional and uneven across member-states.

The agreed changes are significant:

Mandatory screening in all member-states: the updated framework makes previously optional screening mandatory. Bulgaria, Greece and Ireland introduced mechanisms only in 2025, while Croatia and Cyprus are still finalising theirs.

A common set of sectors: member-states must screen investments in defence and dual-use goods, AI, quantum, semiconductors, critical raw materials, critical energy, transport and digital infrastructure, electoral systems and systemic financial market infrastructure.

Closure of the EU-subsidiary loophole: the revision extends screening to investments routed through EU-based entities ultimately controlled by non-EU actors.

Even before the latest clampdown, Chinese FDI in the EU had fallen sharply. But its composition is changing: investment has shifted from mergers and acquisitions (M&A) to greenfield projects, concentrated in the automotive and battery sectors and increasingly directed towards more accommodating member-states such as Hungary.

These dynamics leave two key problems largely untouched. The first is that the updated screening framework still leaves final decisions mostly at national level. The second is that it is designed primarily around M&A, not greenfield investment. M&A deals can transfer sensitive intellectual property or relocate strategic manufacturing, while greenfield projects can create different exposure risks, such as bypassing EU trade defences with limited local value added or employment or embedding security risks.

To address these concerns and help European industry catch up in areas where it lags behind China, the EU is preparing the Industrial Accelerator Act. The aim is to raise manufacturing to at least 20 per cent of EU output by 2030 through requirements that parts of strategic value chains be ‘made in Europe’. A leaked draft would require certain Chinese investments – such as in the electric vehicle supply-chain – to include technology transfer, joint ventures and local employment. But the proposal, reflecting France’s more dirigiste instincts, faces strong resistance from more liberal member-states, including Germany and the Nordic countries. The risk is that Europe has solved yesterday’s China problem – takeovers – but not tomorrow’s: industrial location.

The risk is that Europe has solved yesterday’s China problem – takeovers – but not tomorrow’s: industrial location.

The rise and fall of Chinese investments in European high-tech

Between 2000 and 2023, China’s state banks and official creditors channelled around €138 billion into EU economies. AidData has shown this capital increasingly targeted critical infrastructure, critical minerals and high-tech assets such as semiconductors. Attempted acquisitions were remarkably successful, with an 80 per cent completion rate.

From 2015 to 2018, Chinese buyers acquired a string of strategic semiconductor assets and faced little resistance. This did not represent a random shopping spree but a comprehensive targeting of the entire value chain, spanning intellectual property, tools, wafers, foundries and power chips – in line with the Made in China 2025 industrial policy strategy, which set a goal of 70 per cent self-sufficiency for semiconductors.

At the time, political scrutiny in Europe was relatively minimal and co-ordination across member-states virtually non-existent. The prevailing assumption was that ownership did not matter much as long as plants stayed open and jobs were preserved. For example, Silex in Sweden became a global leader in MEMS – a type of semiconductor with telecommunications, scientific and other applications – in the early 2000s. In 2015, NavTech, a Chinese company, bought Silex in a transaction involving Chinese state funds. Soon after the deal, Silex announced plans to build a plant in China, heightening concern about knowledge transfer and inadvertently supporting Chinese military technology. Similar dynamics were observed in the adjacent machine-building sector, with the most controversial example being the 2017 sale of German high-end industrial robot producer Kuka to China’s Midea Group.

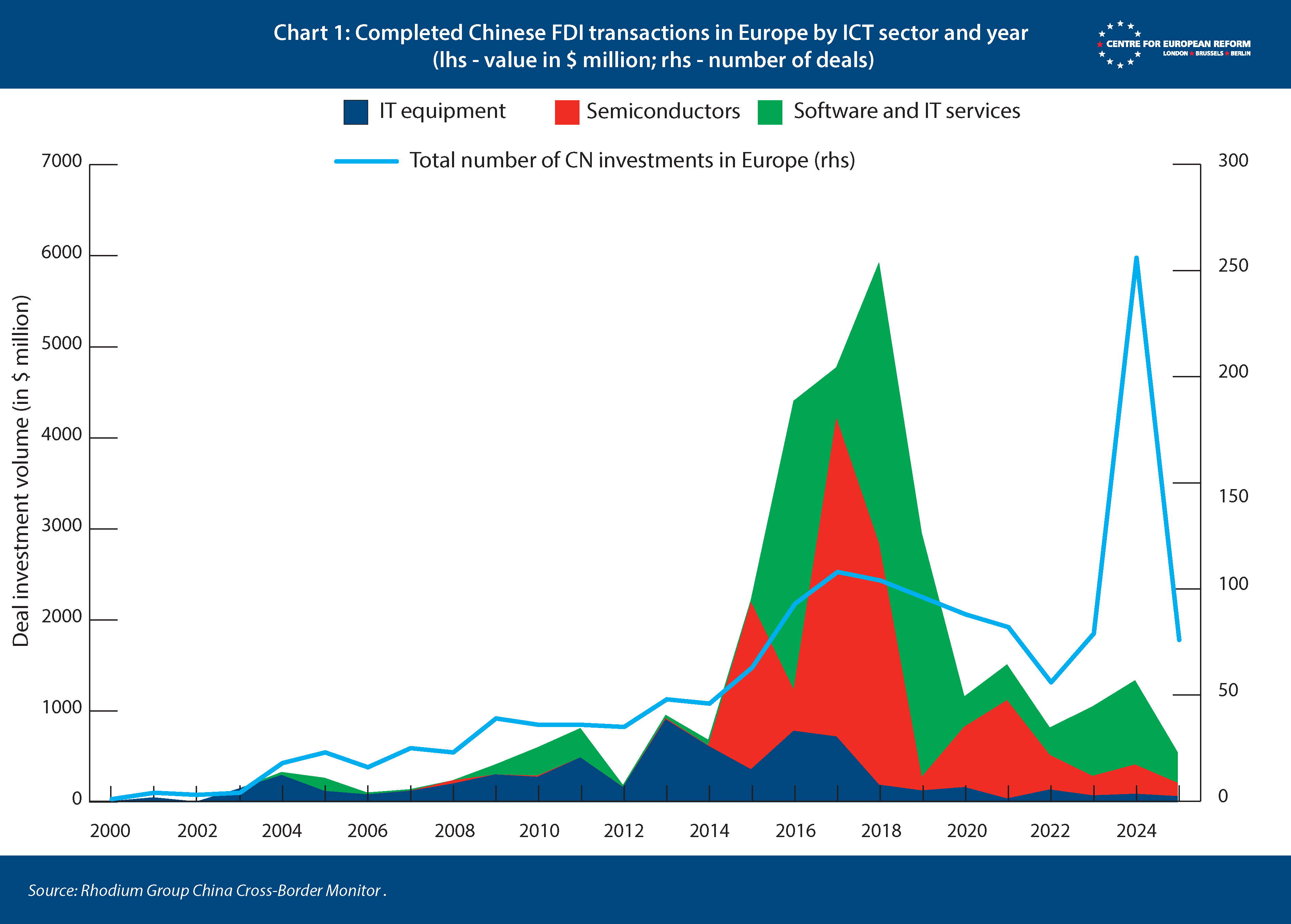

However, this permissive era has largely ended. The risks of China acquiring semiconductor and tech assets in Europe have receded as member-state governments increasingly block takeovers, although there was a spike of smaller deals in 2024 (see Chart 1). A first line of sporadic resistance emerged around 2016–21, often driven by the US cajoling European governments. For example, the 2016 attempt by China’s Fujian Grand Chip to buy German semiconductor equipment maker Aixtron was initially cleared by Berlin, but later derailed after US intelligence agencies raised concerns and the US blocked the acquisition of Aixtron’s US business.

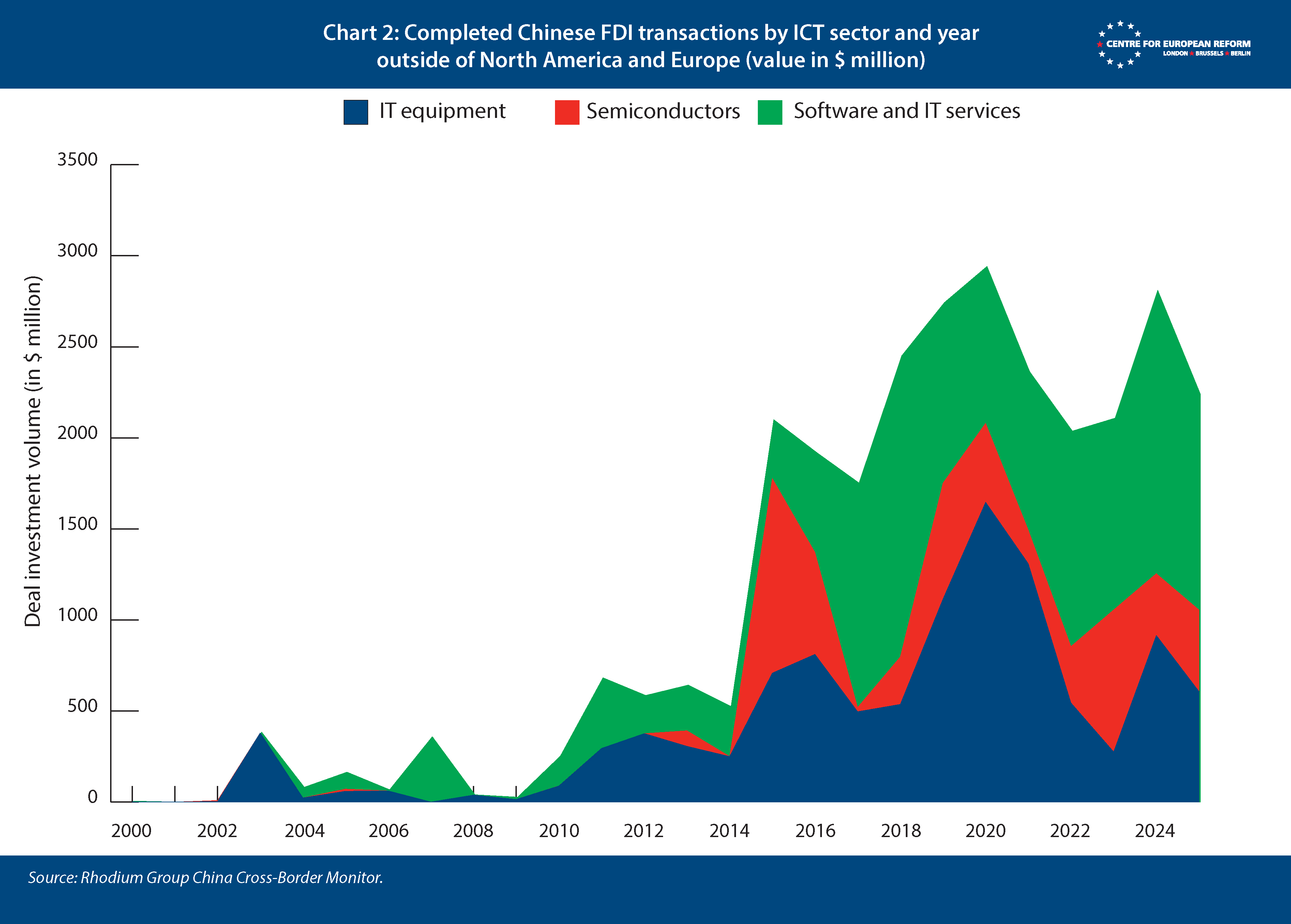

Since then, several key countries housing most of Europe’s tech sector have all tightened screening, particularly after China’s support for Russia’s invasion of Ukraine. Germany (Elmos, ERS and Siltronic in 2022), Italy (LPE in 2021), the Netherlands (Nexperia in 2025) and the UK (Newport Wafer Fab in 2022) have all intervened to block or unwind Chinese acquisitions of sensitive semiconductor assets. These cases suggest China’s ability to buy into Europe’s semiconductor stack is narrowing. Meanwhile, Chinese FDI in information and communications technology (ICT) has increased – and remained high – outside Europe and North America, demonstrating China’s focus on other regions as European countries and the US have clamped down (see Chart 2).

Shift toward permissive member-states and the EU’s response

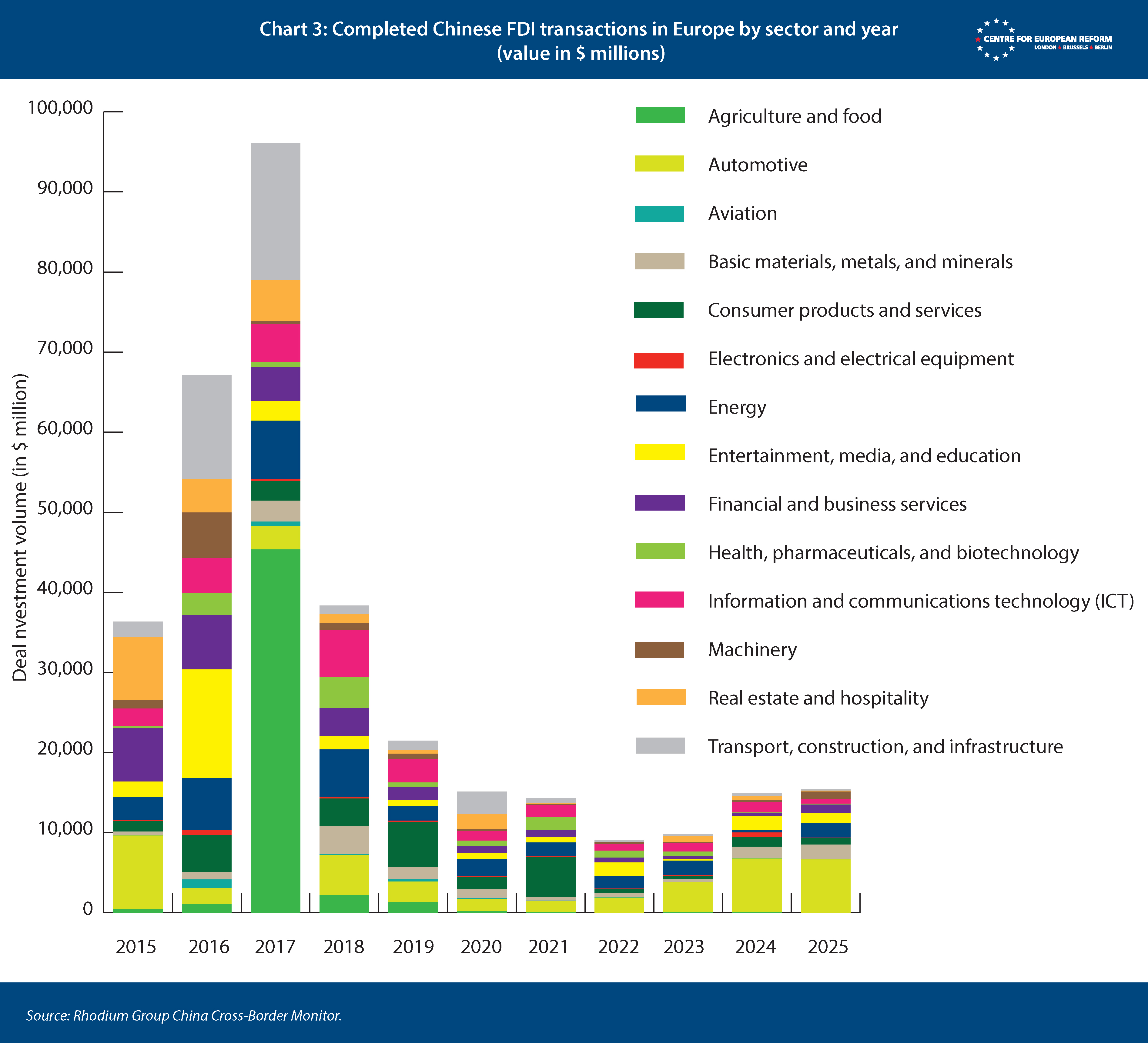

The drop in China’s FDI in the European tech sector is mirrored by an overall collapse of Chinese FDI, across all sectors in Europe since 2018. Chinese investment in Europe is now picking up again from a low base, largely thanks to the automotive and battery sectors. Overall, Chinese companies invested $10 billion in the EU and the UK in 2024, around 50 per cent more than the year before, and these levels seem to have held for 2025. The car and battery sector now makes up around half of Chinese investment in Europe (see Chart 3).

The geography of investment is changing too. The main destination is no longer countries like France or Germany but countries with permissive environments, most notably Hungary and other parts of central Europe, as well as Spain. Hungary captured 44 per cent of all Europe-bound Chinese investment in 2023, more than the UK, Germany and France combined, and a still sizeable 33 per cent in 2024. China’s preference to invest in those countries undoubtedly reflects their relatively looser investment screening and the fact that Spain and Hungary are lower-cost car-making hubs for foreign producers serving the EU market.

With access to the EU market via Hungary or Spain, Chinese carmakers can circumvent the EU’s current countervailing duties of up to 35 per cent tariff on imports of China-made battery EVs (established in late 2024). In this way, the tariffs can help to localise production of EVs in Europe. But the risk is that Chinese FDI creates pure assembly plants for imported Chinese content, undercutting established or emerging European businesses in their home market, potentially without strong value added or employment benefits. For example, the Spanish government and battery firm CATL are locked in negotiations about the latter’s wish to bring 2,000 Chinese workers to build a new €4.1 billion battery factory in Zaragoza.

China may also wield state-owned enterprises and financing to direct greenfield investments toward member-states aligned with Chinese policy positions, potentially creating Trojan horses disrupting EU foreign policy unity. In September 2024, for example, Spanish Prime Minister Pedro Sánchez suddenly urged the European Commission to reconsider its WTO-compliant duties on Chinese-made EVs, marking a notable U-turn as China’s Envision Group promised a $1 billion green hydrogen industrial park in Spain. Additionally, Chinese firms’ batteries and other products may come with operational, data, and cybersecurity concerns – even if they’re manufactured in Europe.

Policy recommendations

Many member-states have expanded FDI screening and are applying the rules more strictly. The EU’s improved FDI screening framework is expected to enter into force in the summer of 2026 with an implementation phase of up to 18 months. But the status quo leaves important gaps:

First, China can still channel investment through countries with weaker or incomplete FDI screening regimes. Member-states retain primary authority to authorise FDI, so unless they confer powers to Brussels, the EU’s powers will remain structurally constrained. The new framework merely requires governments to explain how they take account of Commission opinions and other member-states’ concerns – a bureaucratic exercise that hardly presses them to tighten investment controls. Second, Beijing may shift towards smaller and less visible deals allowing it to fly under the radar. Third, greenfield investment remains a blind spot in the EU’s screening architecture. This is not just a theoretical risk: in 2023-24, ICT was the only sector beyond automotives to attract a meaningful volume of Chinese greenfield investment, driven above all by Nexperia’s €185 million expansion of its Hamburg plant and Okmetic’s €400 million silicon wafer facility in Finland.

The EU’s improved FDI screening framework is expected to enter into force in the summer of 2026.

To tackle the first two challenges, the EU and national governments should continue to strengthen their screening capabilities to effectively monitor and respond to Chinese and other FDI in a risk-based manner. With more resources from the next multiannual financial framework, the EU’s seven-year budget going into effect in 2028, the EU should support member-states with weaker screening mechanisms on a voluntary basis and expand screening co-ordination with international partners, like the UK and Japan. In the long-term, leaders should centralise authority in Brussels, which would harmonise screening and ensure projects are in the entire bloc’s interest.

In the short term, national governments could dedicate a small percentage of their increased defence spending to economic security efforts like FDI screening. The Chinese acquisition of Imagination Technologies in the UK in 2017, which resulted in chip IP with defence applications flowing to China, demonstrates how enhanced screening efforts align with member-states’ defence push.

To address the third challenge – the shift in Chinese FDI toward greenfield investments – the EU should amend the FDI screening mechanism to require member-states to review and co-ordinate on greenfield projects above a certain deal size, in sensitive technology areas and from countries of concern. In doing so, the Commission should take care to avoid onerous new processes for investments with low-security risks. For example, new rules should not prevent or create new obstacles for investment like that of US chipmaker Onsemi, whose announced manufacturing site in the Czech Republic – enabled by the European Chips Act – will help supply chips for EVs and data centres. While such an approach would not provide definitive guardrails against risky Chinese greenfield investment, it would enhance transparency and build up national capacity to condition certain greenfield investment if needed.

The decline in Chinese FDI into Europe suggests that most Chinese firms can serve European demand from China as a supply hub. European policy-makers should therefore be clear-eyed: investment conditionality cannot deliver on its own. China’s own catch-up strategy combined technology transfer and local content rules with extensive direct and indirect subsidies and tightly managed market access. Trade and investment policies are complements, not substitutes: firms localise production in response to access conditions, and shifts in trade barriers reshape FDI through tariff-jumping and supply-chain reorganisation. To attract meaningful technology transfer in sectors where China leads, such as batteries, Europe will need to align demand-side instruments – trade defence, procurement and market-access rules – with its FDI screening framework.

The decline in Chinese FDI into Europe suggests that most Chinese firms can serve European demand from China as a supply hub.

Conclusion

Over the last decade, Europe has made real progress in protecting its technological base. The period in which Chinese firms could quietly acquire strategic semiconductor and other high-tech assets across the continent is largely over. Member-states are showing greater willingness to intervene where security risks are clear, and the EU is setting stronger minimum standards across the bloc. Yet loopholes remain – particularly around greenfield investments, uneven national enforcement and smaller deals that evade scrutiny – and closing them will require stronger EU and member-state capacity as well as, over time, greater EU-level control. The case for centralising powers in Brussels is ultimately political: it constrains member-state governments that actively court Chinese investment for short-term gains, undermining European unity and single market cohesion. That is a problem that no amount of ‘co-ordination’ or technical ‘capacity-building’ can solve. Europe can reduce the risk of China setting up low-tech, low-value-added assembly plants that rely overwhelmingly on Chinese inputs by tightening trade restrictions on Chinese imports and applying EU-wide local content requirements across the single market – but such measures remain controversial.

At the same time, Europe is asking more of Chinese investment than it is likely to deliver. Chinese FDI in geographical Europe (including the UK), is now modest, roughly €10 billion a year today, compared with a peak of €90 billion in the 2010s. The decisive factor will not be how Europe manages Chinese capital, but how successfully it strengthens its own competitiveness. That means deepening the single market, easing regulatory constraints, improving labour and capital allocation, and targeting industrial policy where Europe can realistically compete, including in semiconductor niches where it can defend and expand its indispensability, such as chipmaking equipment. Ultimately, Europe’s China policy cannot substitute for economic reform at home. Protecting against hostile takeovers and strategic dependencies must go hand in hand with enabling competition and innovation, and getting that balance right will determine whether Europe remains a serious industrial power.

James Green is a research fellow and Sander Tordoir is chief economist at the Centre for European Reform.

Add new comment