Energy shock 2.0: Lessons from 2022 for the Hormuz crisis

If the Strait of Hormuz stays closed, Europe will face as serious an energy crisis as it did in 2022. This time, energy poverty policies must be more targeted, and electrification more ambitious.

For the second time this decade, Europe is facing an energy crisis prompted by a war someone else started. At the time of writing, the Strait of Hormuz remains largely closed, with fewer than 15 tankers a day passing through, compared to 140 before the war. Iran remains in control of the strait, and is reportedly demanding up to $2 million in crypto payments for ships to pass. They would only be allowed through if they are registered in countries that did not take part in the war or allow their bases to be used by the US or Israel. Iran is also making maximalist demands for a permanent cessation of hostilities, including tolls on the strait, the right to enrich uranium, an end to sanctions and the removal of US troops from bases in the Middle East. Negotiations are yet to move Iran from these positions.

For the second time this decade, Europe is facing an energy crisis prompted by a war someone else started.

By comparing the current situation with the energy shock that followed Putin’s full-scale invasion of Ukraine in 2022, it is possible to sketch best and worst-case scenarios for the European economy, based on oil and gas supplies already lost due to damaged infrastructure, and the potential long-term closure of the strait. In a worst-case scenario, the energy shock will be worse than in 2022, but the macroeconomic and energy context has changed.

Europe can learn lessons from what went right and wrong last time, and adjust policy accordingly. Governments can support people being plunged into fuel poverty without subsidising fossil fuels for everyone. Demand is weaker than it was, so policy-makers should avoid a rush to tighten macro-economic policy. And two fossil-fuel crises in four years show that governments should accelerate the energy transition.

The Strait of Hormuz: Best and worst cases

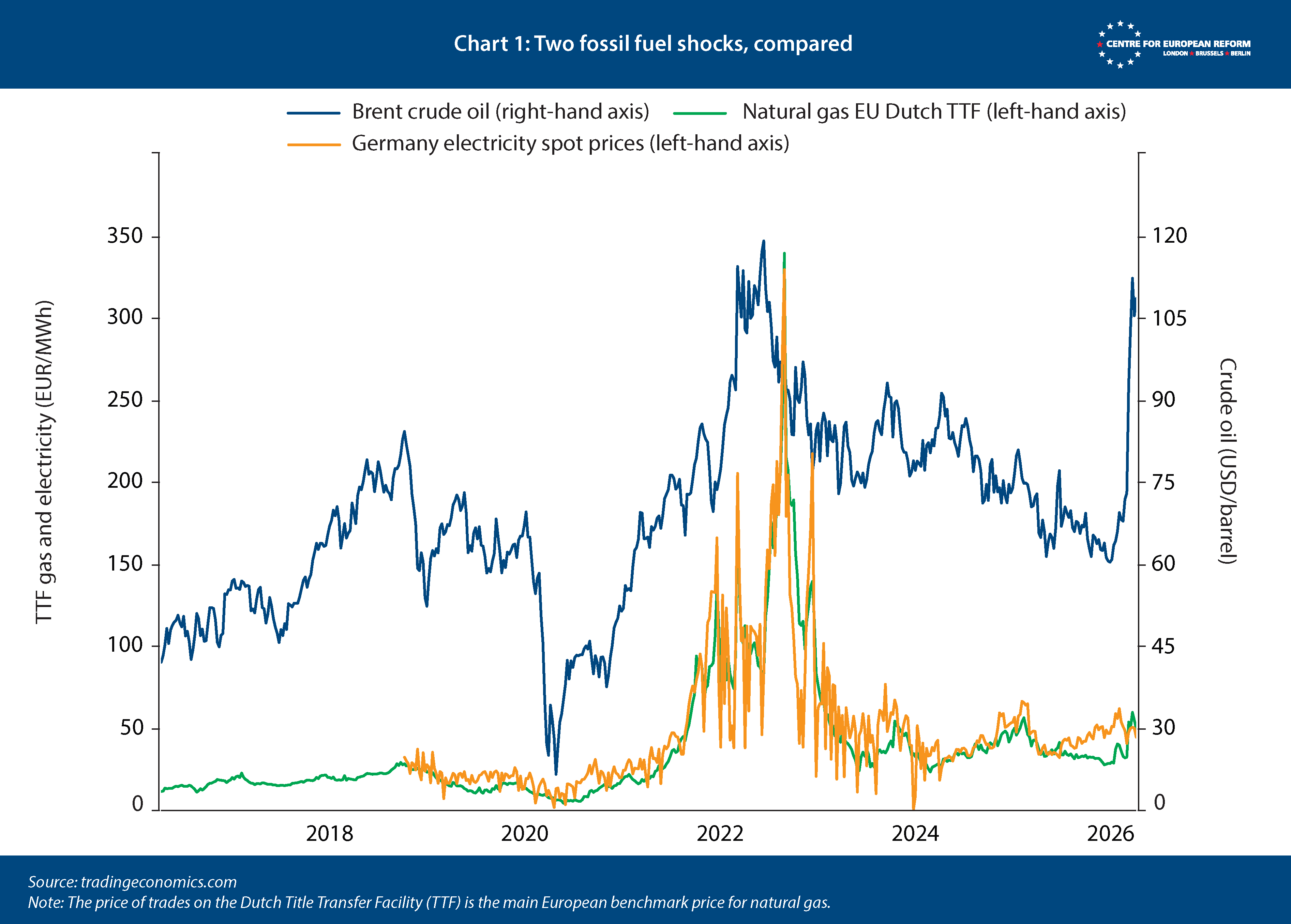

So far, the oil price rise is similar to that at the height of the 2022 shock, while gas and electricity price increases have been more muted (Chart 1). This is because oil markets are more forward-looking than gas and electricity markets: oil and its derivatives, like petrol and jet fuel, can be stored more easily than gas, and then sold at a later date for more money, which means that prices rapidly rise when future supply is likely to be curtailed. The 2022 shock started out as a gas shock as Russia curtailed its gas pipelines to Europe: because electricity generation relies on gas power plants at times of high demand, electricity prices then spiked. Today, the Hormuz chokepoint is preventing most oil and LNG exports from the region from reaching the global market. Europe’s gas supply is more diversified than in 2022, so the price spike has – for now – been limited. But that may not last, because liquefied natural gas (LNG), like oil, is a global commodity.

The loss of LNG supply so far is about 1.5 million tonnes a week, or about 18 per cent of global supply. Less than 10 per cent of the pre-war flow of 2.8 million tonnes per day of crude and oil products are getting through the strait. Even in the best-case scenario, with Iran allowing trade through the strait to resume, severe damage to key oil and gas facilities mean that supply will be lower than before the war, and slow to recover. Qatar has lost 17 per cent of its LNG export capacity: repairs will take three to five years, cutting 12.8 million tonnes of LNG per year or about 2.5 per cent from global LNG supply. More than 3 million barrels per day of oil refining capacity in the Gulf region – about 3-4 per cent of global refining capacity – are offline, either due to attacks or because refineries' crude oil storage is full. Oil refining bottlenecks have forced cuts in crude oil production, which in turn has reduced supplies to refineries outside the Gulf. All these facilities are slow to restart, so it will take weeks or months to resume operations if the Strait of Hormuz reopens.

Unlike Asia, Europe is not facing an immediate supply shortage. Over 90 per cent of Gulf LNG generally flows to Asia, and only a few European countries, especially Italy and Belgium, are directly affected by Qatar’s halt to LNG production. Asia is also the destination for over 80 per cent of Gulf oil and oil products flowing through the strait. Asian governments have already started to implement rationing and other measures to manage oil and gas consumption. If the cease-fire holds and the strait is reopened – even with tolls that would add $1 a barrel to the price of Gulf crude – Europe will suffer a limited price shock, temporarily slowing growth and raising inflation. However, the worst-case scenario – a long-term or even permanent closure of the strait – would result in a European energy shock similar in scale to the 2022-23 energy crisis.

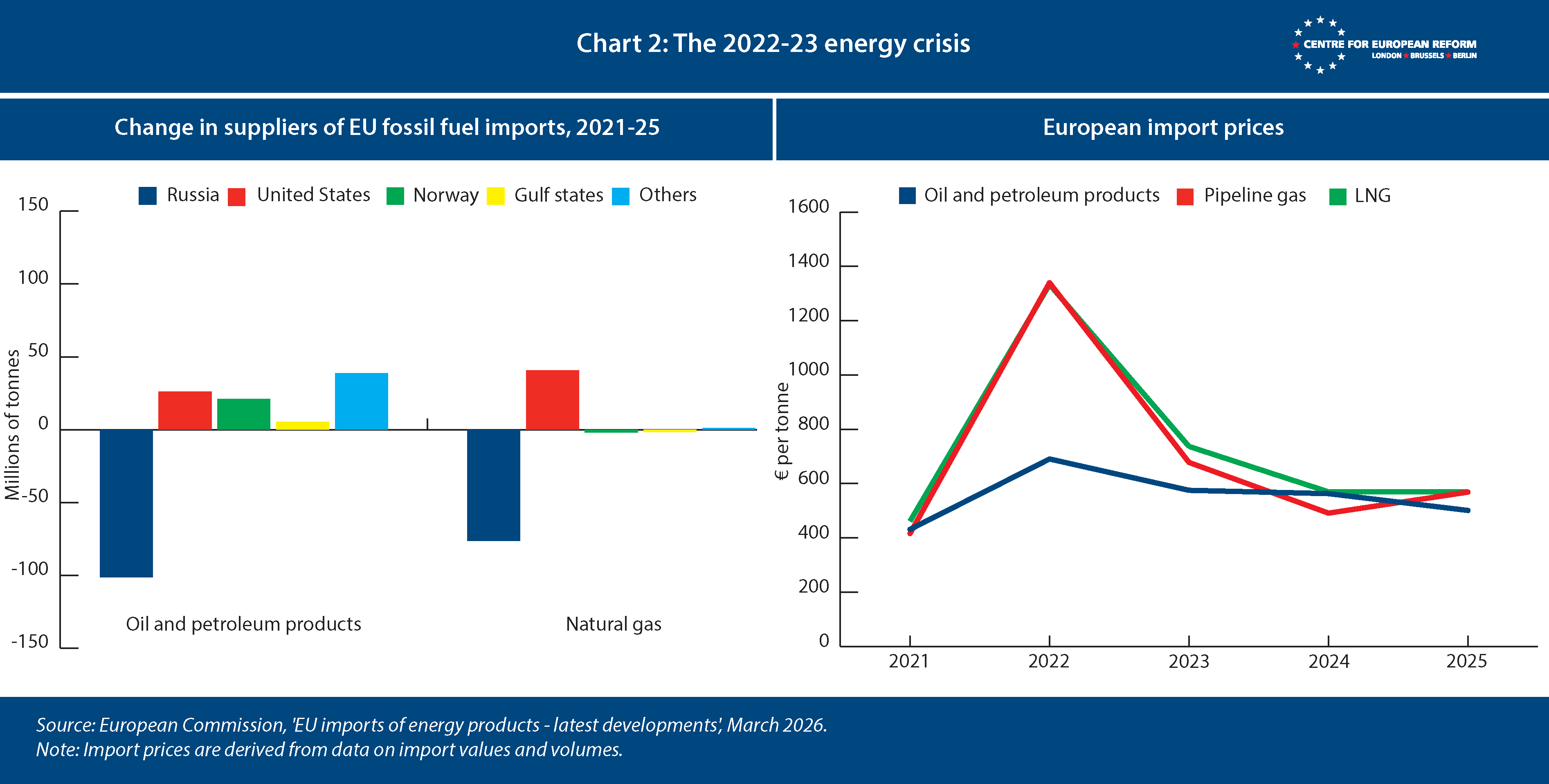

We can get a sense of the scale of the fossil fuel shock by considering how European prices reacted to the loss of Russian supplies in 2022-23. At the beginning of 2021 – before Russia started to curtail pipeline gas exports in preparation for the invasion – Russia provided EU countries with 60 per cent of their pipeline gas imports and 25 per cent of oil and refined products. It then took Russia’s supply cutoff, Europe’s import restrictions and the ensuing huge rise in energy prices – for both gas and oil – for Europe to replace Russian energy with other sources of supply. Imported oil prices rose by more than 50 per cent between 2021 and 2022, while imported gas prices tripled (see Chart 2).

If the Strait of Hormuz remains closed, Europe will face a larger oil supply shock than in 2022. Russian oil and refined products fell from 25 per cent of European imports in 2021 to 3 per cent by the beginning of 2023, amounting to about 100 million tonnes displaced from Russia to other exporters. But Russia continued to export to non-Western countries, limiting global price rises. Today, the Hormuz blockage is keeping 20 per cent of global oil supply off the global market: this amounts to an annual loss of up to 1,000 million tonnes of oil exports. European import prices for oil and refined products rose by about 50 per cent in 2022. Given the substantially larger disruption to oil markets if oil exports from the Gulf continue to be cut off, price increases would be much greater.

If the Strait of Hormuz remains closed, Europe will face a larger oil supply shock than in 2022.

On gas, Europe cut its imports of pipeline gas by about 75 million tonnes between 2022 and 2025, and replaced it with 50 million tonnes of LNG, largely from the US. The surge in European demand for LNG had a global impact: prices in both Europe and Asia tripled in 2022 before falling back as more supply came onstream. Given that the Gulf also supplies about 75 million tonnes of LNG, global LNG prices – which Europe will pay – could see similar rises to those in the 2022-23 crisis. In those European countries that are still largely dependent on gas power generation, electricity prices could also rise by similar amounts to the spikes in 2022-23.

The roll-out of renewables since 2022 will help to curtail the effects of gas price hikes on the cost of electricity in some countries. In Spain, which after Germany is the EU country to have added the most renewable power capacity to its grid since 2022, gas now makes up only 21 per cent of its electricity mix (down from 30 per cent in 2022), and sets the power price only 15 per cent of the time. Several nuclear plants in France were offline at the worst possible time in 2022, but the fleet is now functioning normally, which will curb French electricity price rises. Italy, however, which generates 47 per cent of its electricity with gas, is much more exposed to the increase in gas prices. So is the UK, because gas contributes to 31 per cent of its electricity mix and sets the electricity price about 85 per cent of the time.

Europe is also in a better position to shift from fossil-fuelled technologies than four years ago. Europe has seen a surge in heat pump and electric vehicle (EV) uptake since 2022. EVs accounted for 17 per cent of the EU market in 2025, up from 9 per cent in 2021, while hybrid-electric cars captured 35 per cent of the market. A range of lower-priced EVs have been introduced, making them affordable to more consumers – and with increasing oil prices, the cost of running an EV will improve, relative to petrol.

Overall, European policy-makers should assume that a plausible worst case for the crisis is a worse oil shock than 2022-23 and a similar gas shock, but a smaller electricity shock on average, with more variation across countries. That does not mean, however, that they should simply repeat the policies they enacted last time – either macroeconomic policy or expensive and inefficient attempts to shield consumers from rising prices.

Principles for macroeconomic policy

How should fiscal and monetary policy respond to the energy shock? The European Central Bank (ECB) was cautious during its last meeting, with ECB president, Christine Lagarde, saying “we will not act before we have sufficient information on the size and persistence of the shock”.

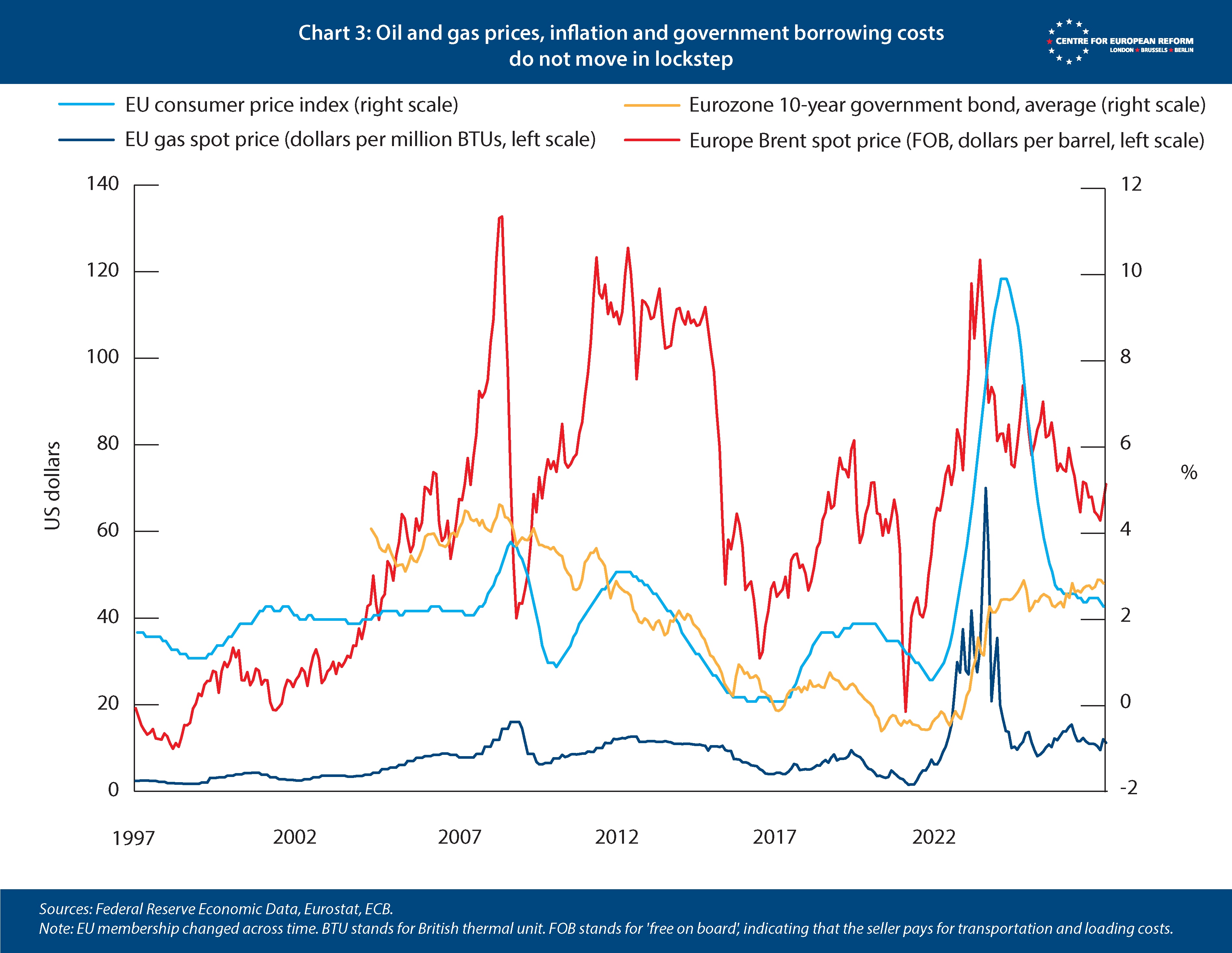

The inflation shock after the 2022 energy crisis does not offer a simple guide to action. A big jump in inflation followed the rise in energy prices. But there were several other imbalances in the European economy at the time. Consumer demand came roaring back after Covid lockdowns were lifted, fuelled by savings built up during the pandemic. Supply was also constrained by problems in global distribution, with ships stuck in the wrong locations, and some manufacturing plants slow to restore production. The economy today is more balanced, with European demand weaker and the supply side less constrained by the effects of the pandemic.

As Chart 3 shows, there is not a mechanical correlation between energy prices, inflation and government borrowing costs. Aggregate demand matters. Energy prices – particularly oil – rose sharply after the 2008 financial crisis, raising inflation above target. The ECB mistakenly raised interest rates in 2011 as energy and commodity prices rebounded from the financial crisis, only to cut them again as the euro crisis blew up. That crisis, coupled with austerity, subsequently pushed down inflation and sovereign bond yields (the benchmark for borrowing costs across the economy).

The 2026 energy price shock will certainly raise inflation. How much inflation rises, however, depends on how long the Iranian regime keeps the Strait of Hormuz closed. The 2022-23 spike in inflation was larger and more persistent than central banks had forecast, but that was driven as much by pandemic imbalances as the energy crisis. But given the weaker state of European consumer demand in 2026, compared with 2022, there is less likelihood that inflation will persist, feeding through into higher wage demands and requiring sharply higher interest rates to move the economy back to balance. Consumers and businesses will build up savings to pay for higher energy bills over the coming winter, which will also reduce consumption and investment. In fact, eurozone households have structurally higher savings rates than their US counterparts, and have spent less of their excess Covid-lockdown savings. All this cautions against quick moves to tighten monetary policy.

The same goes for fiscal policy. Debt burdens rose after the pandemic and 2022 energy shock, and governments are paying more to service their debt. Eurozone and UK government borrowing costs have risen since the Iran war started, but that is to be expected as investors assume that higher inflation will force central banks to raise interest rates. If weakening consumption and investment feed through into rising unemployment, governments would make the situation worse by raising taxes or cutting spending. They should wait until the economy recovers.

Principles for energy support measures

Energy demand is highly ‘price inelastic’, meaning that higher energy prices do not lead to large falls in energy consumption in the short term. Because most European countries are energy importers, higher energy prices automatically make them poorer. Demand has to fall to bring the economy back into balance. Government’s core function in an energy price shock is to distribute the costs in a way that minimises the damage to the broader economy while tackling poverty. People will cut back on other purchases to refuel their cars and pay their energy bills. That can happen chaotically, with poorer people cutting discretionary spending to pay for energy and food (which, as a result of higher fertiliser costs, will also rise in price). Alternatively, governments can steward the process.

Policy-makers should draw up public information campaigns to reduce energy consumption that is less needed to sustain domestic economic activity. That principle is behind the International Energy Agency’s advice to work from home, turn down thermostats and reduce gas boiler flow temperatures, and temporarily impose lower driving speed limits. Governments should draw up contingency plans now to ration fossil fuels to maintain production in strategic energy-intensive industries, in case Iran succeeds in keeping the strait closed.

Policy-makers should draw up public information campaigns to reduce energy consumption that is less needed to sustain domestic economic activity.

Governments should resist the temptation to provide blanket energy bill rebates, fuel tax cuts or price caps in an effort to tackle poverty, as happened in 2022-23, because that would increase consumption of scarce fuels. EU governments spent €540 billion on emergency measures – most of which were untargeted measures to lower prices. That raised demand for scarce energy resources, with knock-on impacts for industry and for poorer countries which could not afford to pay as much as Europe for LNG. It also weakened the incentives for businesses and households to invest in green tech to reduce their exposure to high and volatile fossil fuel prices. By entrenching the belief that government would bail out consumers in future fossil fuel shocks, another round of untargeted subsidies would weaken energy security and undermine the energy transition.

We are seeing similarly wrong-headed, untargeted policy decisions happen today. Spain has already allocated €5 billion to cuts to VAT on energy and fuel duties. This is an order of magnitude more than the €400 million earmarked for EV subsidies in 2026, and almost twice the sum Spain devoted to all its measures for electric mobility between 2021 and 2025 (€2.7 billion, including both EV subsidies and investment in charging infrastructure). Italy’s emergency measures including fuel duty cuts will cost it €1 billion over two months – more than the €600 million recently allocated to EV subsidies. Poland’s cuts in fuel taxes will cost €370 million a month.

France’s approach is better: the government is targeting hardest hit sectors, while also preparing a plan to electrify the French economy faster, doubling subsidies by 2030. French state-owned energy company EDF is allocating €240 million to support measures for the electrification of transport, heating and industry.

Instead of untargeted energy price support, governments should provide time-limited cash transfers to poorer households to help them pay their energy bills, and subsidies and cheap loans for electrification options such as EVs and heat pumps.

By providing cash, governments will incentivise poorer households who can economise on fuel to do so, while enabling them to pay higher food costs. Cash transfers are easier to target at the genuinely needy than bill support, because welfare systems are set up to provide payments based on income. Governments have less data on household energy consumption. Governments should impose windfall taxes on oil and gas companies to fund temporary support measures, as after the 2022 crisis, with a collective agreement at the EU level.

Governments need to hasten the shift from fossil fuels in transport, heating and industry. The Hormuz crisis provides another reminder that Europe, a continent poor in hydrocarbons, needs to go faster. To push consumers and businesses to invest in both areas, and prepare for future energy crises, governments should prioritise maintaining the price signal. Governments should, however, increase targeted subsidies for green tech and provide cheap finance for heat pumps, EVs and solar panels to help consumers who cannot currently afford the initial investment needed for these technologies. To reduce the electricity price relative to natural gas and petrol, taxes and network costs can be shifted from electricity bills into general taxation to reduce its price relative to natural gas and petrol. These moves would be far more efficient uses of public funding than untargeted measures that mute price signals.

Governments need to hasten the shift from fossil fuels in transport, heating and industry.

Conclusion

Europe is facing its second fossil fuel crisis in four years, and the lesson is clear: to improve its energy security, it must rapidly shift away from oil and gas imports and towards home-grown clean electricity. Fossil fuel markets are being destabilised by authoritarian governments in Russia, the Middle East and, at least for now, the US. By providing support for the most vulnerable households and allowing the price mechanism to push other consumers, businesses and energy suppliers towards renewables and electric technology, Europe will come out of the Iran crisis in a stronger position.

Elisabetta Cornago is assistant director and John Springford is an associate fellow at the Centre for European Reform.

Add new comment