China shock 2.0: The cost of Germany's complacency

- There is a growing consensus a new China shock is reverberating across global goods markets. Nowhere is that shock more consequential than in Germany. Its manufacturers in core industries – cars, machinery, chemicals and aircraft – are being simultaneously squeezed out of China and other foreign markets, and at home.

- The shock is worsening. Analysts had estimated China would only export 10 million cars a year by the end of the decade. But China’s 2025 fourth quarter exports, annualised, already hit that mark. The car sector is not unique. In 2025, China’s overall export volumes grew at more than twice the pace of global trade. And they gained strength in early 2026, with first quarter export volume growth at 15 per cent.

- In its new five-year plan (2026-30), China shows no sign of changing course. It is committed to displacing imports in the few sectors where it still depends on foreign supply. China is set to continue expanding manufacturing supply even as household demand remains weak and the property drag persists, implying more exports.

- The textbook expectation – that an economy this large must eventually rebalance through stronger imports, currency appreciation or falling competitiveness – is not materialising. China is intervening to stymie currency appreciation, while its vast domestic savings mean it could plausibly sustain an external surplus of 10 per cent of GDP, with no hard limit on the foreign financial claims it can accumulate.

- The risk for Berlin, which already struggled to adjust when China’s surplus jumped from 2 to 5 per cent of GDP from 2022 to 2025, is acute. Much of the demand generated by Germany’s fiscal expansion, after relaxing the debt brake, could leak straight into Chinese imports and throttle Germany’s recovery. Global car, machinery and chemicals production could concentrate further in China, eroding innovation in traditional manufacturing centres and increasing China’s ability to coerce Berlin by threatening to throttle supply the way it did for rare earth minerals.

- For a long time, Berlin struggled to see the problem clearly. As the world’s archetypal surplus economy, Germany saw itself as part of a coalition of exporting nations and resisted scrutiny of policies underpinning large trade surpluses. But China’s surplus now dwarfs Germany’s. French diplomats have put China’s imbalanced growth model at the top of the G7 agenda and called for the EU to more strongly defend its home market.

- Germany remains hesitant, even as China has already eaten much of German industry’s lunch and is preparing to start on dinner. The EU has launched a scatter of product-specific trade defences and a piecemeal buy-European industrial policy. But China’s trade surplus with the EU is still growing at around 30 per cent annually, showing these efforts are too slow and too narrow.

- Germany faces a structural demand shock from a state-distorted rival that cannot be addressed like past competitiveness challenges: Berlin and Brussels must either bolster their trade defences and industrial policy or prepare to offset the social and economic costs of deindustrialisation at China’s hand.

Germany’s Chinese phantom pain

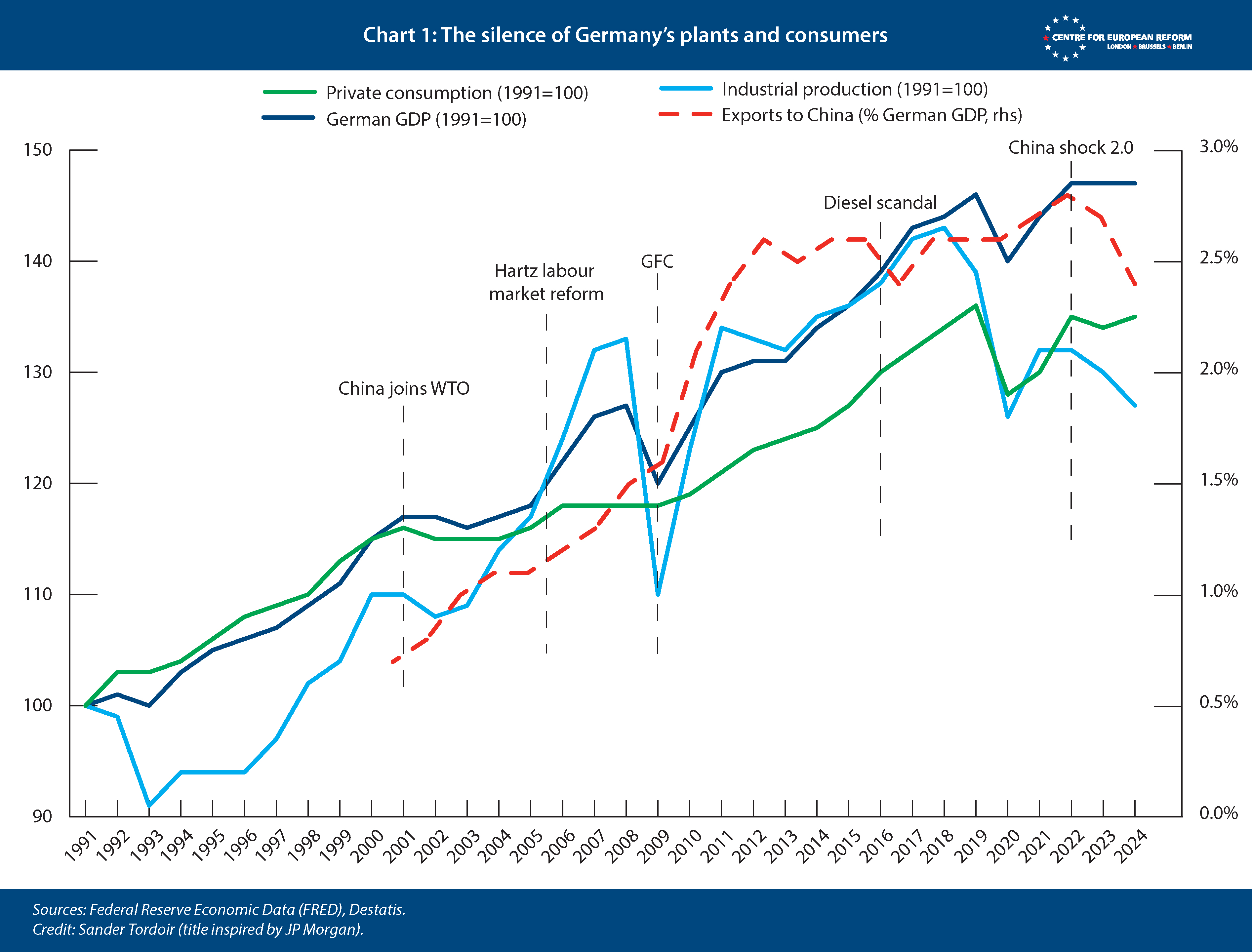

Germany is in a macroeconomic situation unique in its post-Cold War history. Output remains around 6 per cent below its pre-pandemic growth path – a hit of a similar magnitude to the UK’s Brexit shock.1 For decades, private consumption and industrial production alternated as Germany’s engines of growth, broadly rising in line with GDP. This pattern mirrored phases of domestic demand-led growth after reunification and export-led growth after the 2008 global financial crisis. That is no longer the case (see Chart 1). Industrial production has been falling for six years, while private consumption never recovered from the pandemic shock.

Germany’s political debate is frantically searching for culprits. High energy prices and EU bureaucracy dominate the conversation. Neither explanation is fully satisfactory. The Netherlands, Denmark and Poland have grown strongly since 2019, despite being subject to the same EU rules as Germany. The European Commission estimates that the gains from its flagship regulatory simplification agenda – the ‘omnibus’ packages – amount to roughly €15 billion a year, or just 0.07 per cent of EU GDP: useful, but nowhere near enough to offset Europe or Germany’s industrial decline.2 Similarly, while the 2022-23 energy shock hit German manufacturing hard, energy prices had largely come down from their highs before the Iran war and were always structurally higher in Europe and Germany than in the US and China.

Germany’s difficulty in diagnosing the drivers of its malaise resembles a Phantomschmerz – a pain felt where something vital has already been lost. That missing limb is export demand, chopped off by China’s profound pressure on Germany’s industrial base.3 According to analysis published by Bloomberg in late 2024, roughly 40 per cent of Germany’s GDP shortfall can be traced to lost export markets, another 40 per cent to higher energy prices, and the remaining 20 per cent to weak domestic demand, bureaucracy and other factors.4 By focusing overly on bureaucracy, German politics has got the 80-20 rule the wrong way around.

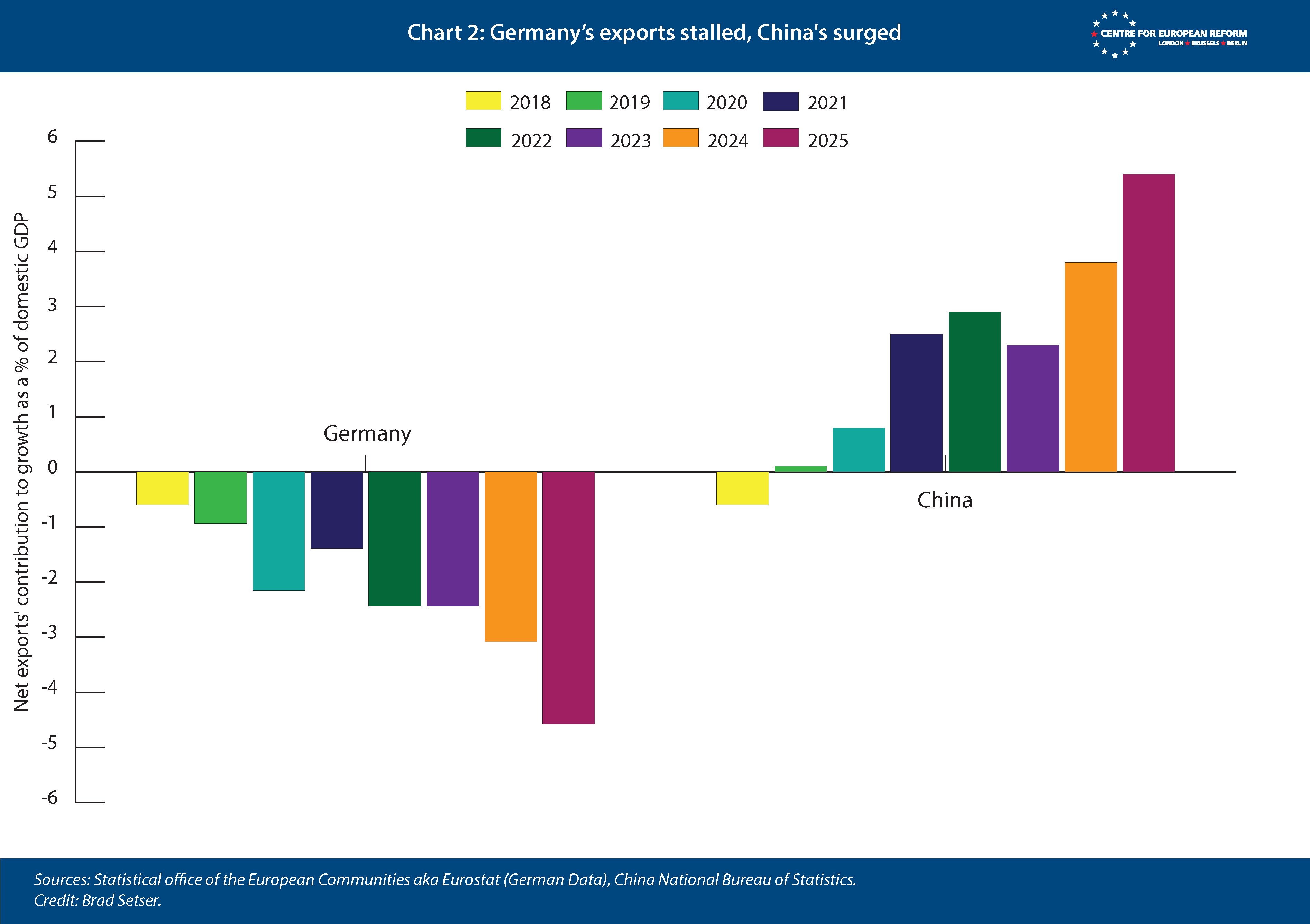

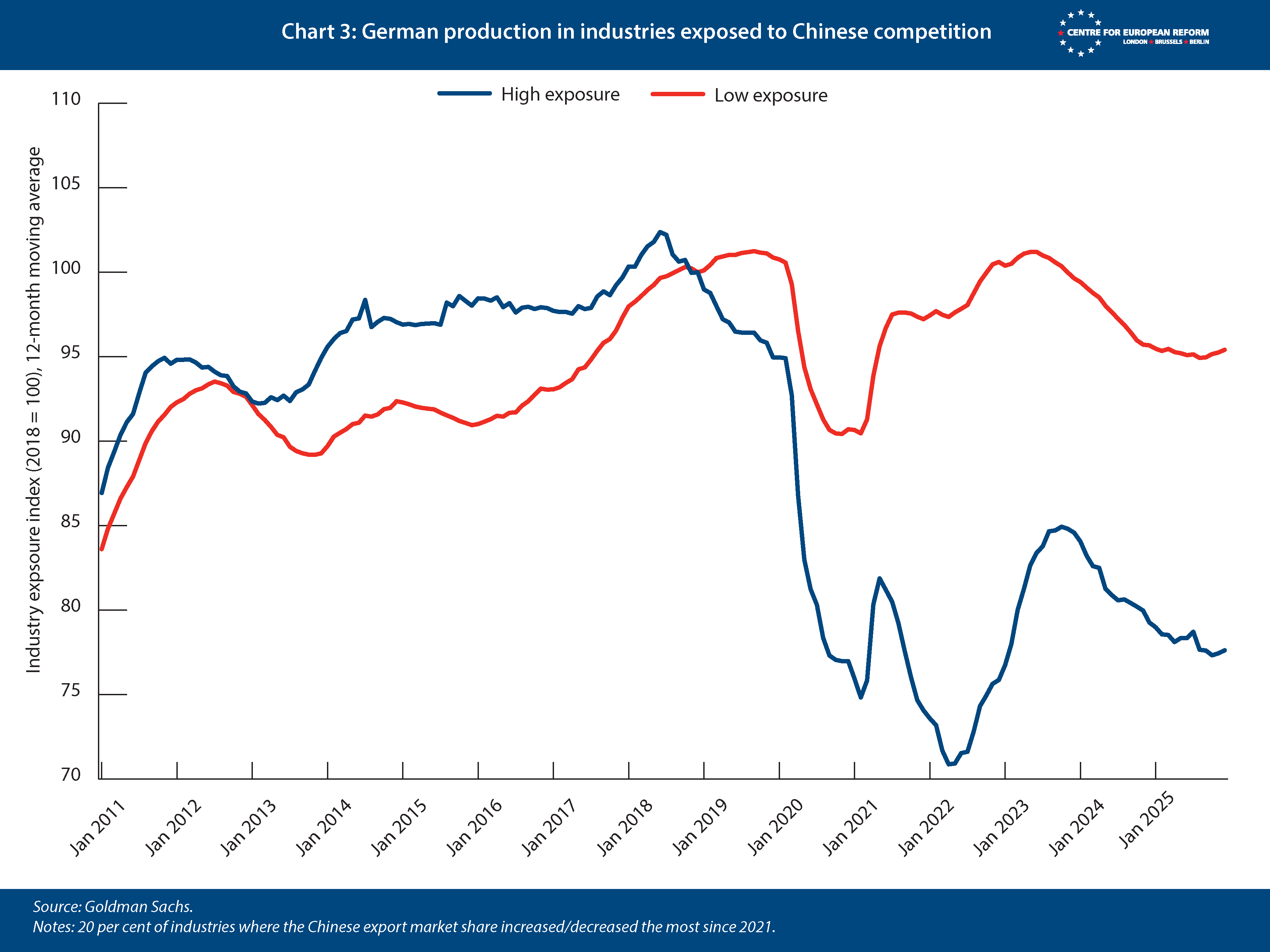

The economic damage China is wreaking upon Germany is rising. The cumulative drag from declining net exports has accelerated since the end of 2023, clocking in at a total of 3 per cent of German GDP. Note that these declines in German exports happened well after the 2020 Covid-19 pandemic and the Russian gas shock of 2022 (Chart 2). The damage has translated to industrial production – with industries most exposed to Chinese exports shrinking relatively more (Chart 3). Yet, even if the China shock is now the most important cause of Germany’s malaise, it is the one Berlin remains least willing to confront.

The three drivers of China shock 2.0 persist

To understand why Germany’s missing export demand is not simply cyclical, it is necessary to look at the mechanics of the second China shock.

Since the pandemic, China’s export volumes have risen by more than 40 per cent while imports have barely grown.5 That has supported China’s growth: the net export contribution of 6 percentage points to GDP since 2019 is exceptionally high for one of the world’s largest economies. But it also means that China is taking demand from the rest of the world without giving much back. German manufacturers are being displaced in China, in third markets and increasingly at home as well.

This is driven not only by China’s growing technological sophistication, but by three overlapping distortions.

First, China’s very high savings rate and weak household consumption depress domestic demand. In the 2010s, weak consumption was masked by investment, in the form of a turbocharged property boom. In the 2020s, that engine flipped into reverse, and falling house prices, when combined with pre-existing weak pensions and limited healthcare, have kept precautionary savings high and household demand low.6

Second, Beijing has responded by doubling down on industrial policy. In priority sectors such as semiconductors, machinery, cars and aircraft, the government’s provision of direct subsidies, free land, cheap machinery and state-backed lending have sharply expanded supply that weak domestic demand cannot absorb. The International Monetary Fund (IMF) estimates these subsidies amount to 4.4 per cent of GDP, roughly $800 billion a year. That is substantially more than EU countries are set to spend on rearmament.7 The OECD has calculated that manufacturers in China receive subsidies that amount to between three and nine times those available to advanced economies.8 Competition between Chinese local governments to support national priority industries leads to massive domestic overcapacity, pushing down domestic prices and forcing firms seeking profits to export, including foreign firms. Volkswagen, Germany’s leading car firm, is localising car design and the supply chain for parts in China – building factories that are decked out with Chinese robots.9

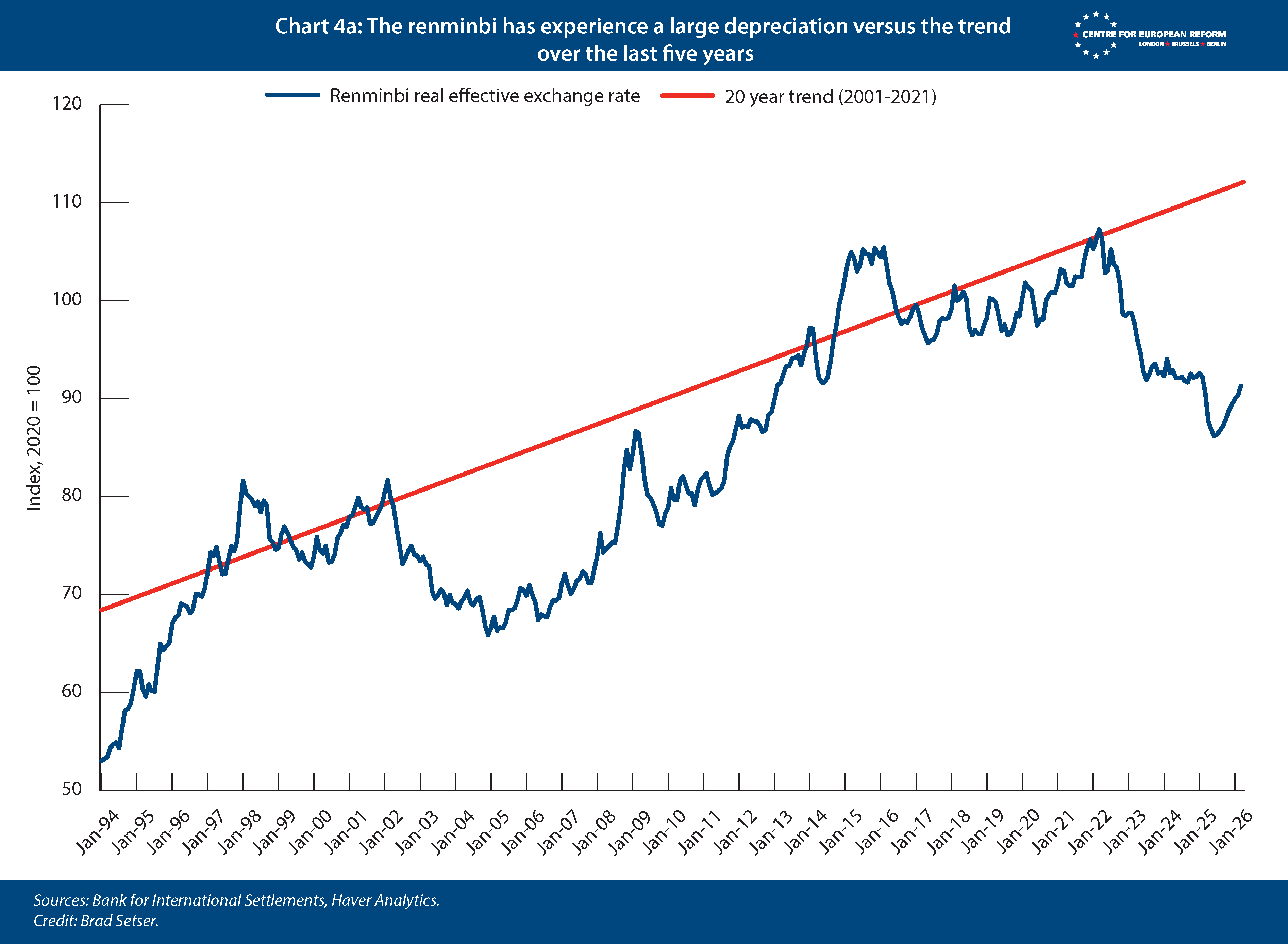

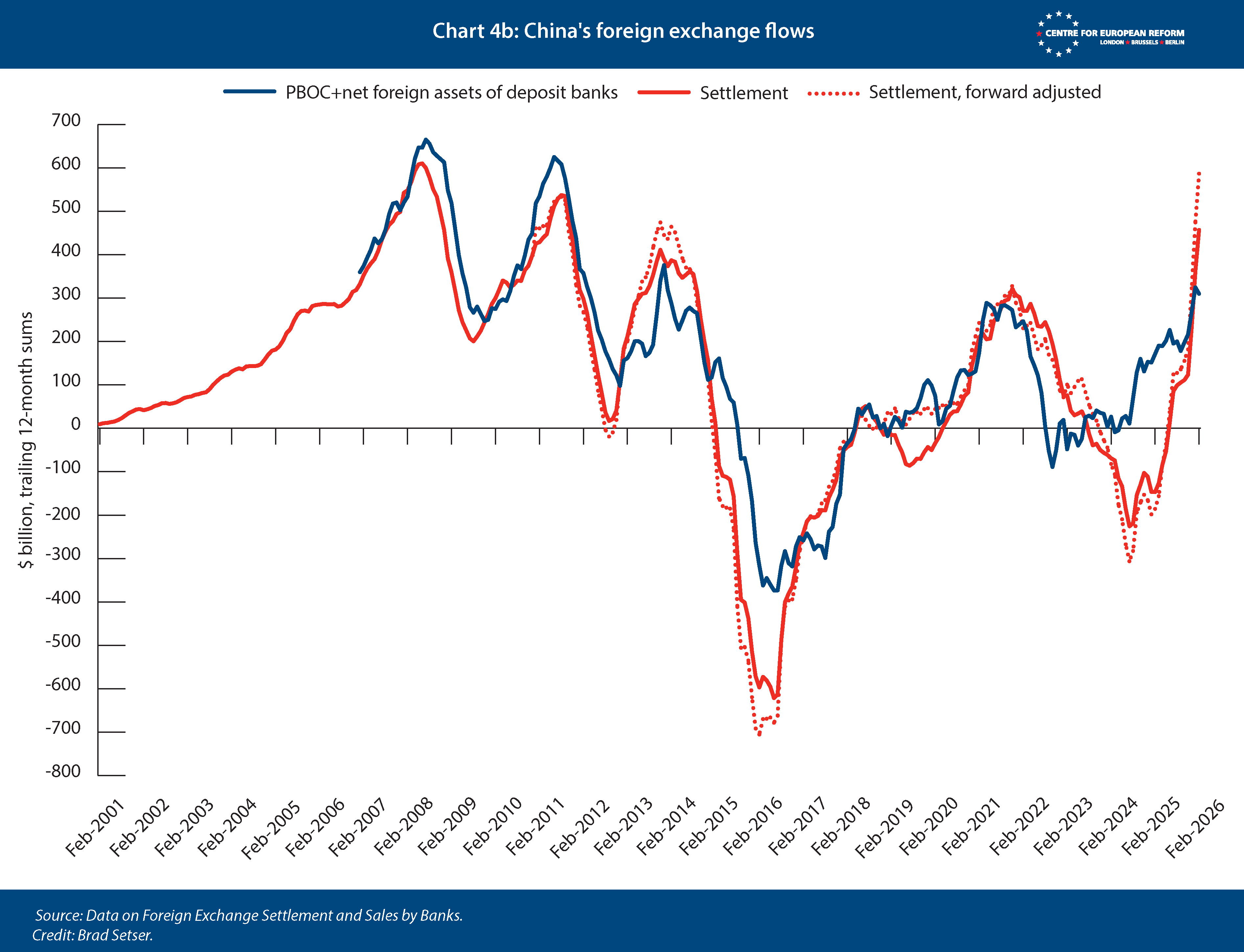

Third, China benefits from an undervalued exchange rate. A country running large current account surpluses would normally see its currency appreciate as it repatriates the foreign exchange earnings into domestic currency. In turn, this would curb Chinese exports and increase demand for imports. Instead, China’s currency fell as China’s central bank cut rates to offset the property downturn and guided the currency down (Chart 4a). Once pressure from the rising trade surplus meant the renminbi would rise, Chinese state banks – likely under the guidance from the central bank – bought dollars, at times heavily, to resist the currency’s appreciation (Chart 4b). The IMF estimates the renminbi may now be undervalued by 16 per cent.10

The true undervaluation may be even larger, as the IMF’s calculations rest on dubious Chinese data reporting. There is a large gap between the current account surplus, measuring China’s net balance of trade in goods and services, earnings on investments, and transfer payments with the rest of the world, and the customs goods surplus, which measures actual goods crossing the border. In 2022, China unilaterally changed the methodology that it uses to estimate the goods surplus that it reports in its broader current account – a statistic used by many institutions and analysts around the world. China now counts the production and sales of foreign firms that happen entirely within China as trade deficit with itself.

As a result, its official surplus in goods trade is far smaller than actual shipments picked up by the customs data. China also adjusts the value of the exports reported in its customs data down, arguing – without supporting evidence – that the dollar value of exports reported to customs exceeds the actual number of dollars received in payment for these goods. Furthermore, China should have a surplus in investment income, not a deficit, as market interest rates on China’s sizeable foreign asset holdings have gone up, not down, over the past few years. This suggests that China’s true current account surplus is above 5 per cent of its GDP, a number that, based on the IMF’s elasticity estimate, would push the estimated undervaluation up to around 30 per cent.11

Made in Beijing, felt in Berlin

At the global scale, China shock 2.0 is similar in magnitude to the first China shock that followed the country’s 2001 World Trade Organisation (WTO) accession. The easiest way to think about both episodes is through China’s manufacturing surplus. The first China shock pushed China’s manufacturing surplus to just under 1 per cent of world GDP. Over the past three to four years, a second major surge – what we call China shock 2.0 – has added almost another percentage point.

The first shock reshaped global manufacturing and harmed many low-wage industrial regions, including in the US. Research on the US shows that workers in areas most exposed to Chinese import competition saw wages stagnate and labour force participation fall.12 The literature on ‘deaths of despair’ captured how the import shock was one of the factors explaining a fraying social fabric in affected regions, marked by rising rates of divorce, suicide and drug addiction – an eerie warning shot for Germany’s car and machine-building cities like Wolfsburg and Stuttgart.13

But the concern about the first China shock was not primarily an argument about strategic dependence, nor necessarily about the long-term productive core of the economy. There was still a plausible view that the sectors lost – such as toy, furniture, or basic electronics production – were not central to future dynamism, and that the broader gains from cheaper imports and technological upgrading could outweigh the local damage. There was also an important offset, which was especially relevant for Germany. During the first China shock, some sectors in Europe expanded on the back of growing trade with China, selling chemicals, cars and manufacturing equipment into a rapidly industrialising economy. Germany, given its specialisation in capital goods, benefitted.

This time is different, and it has far more direct consequences for Germany.

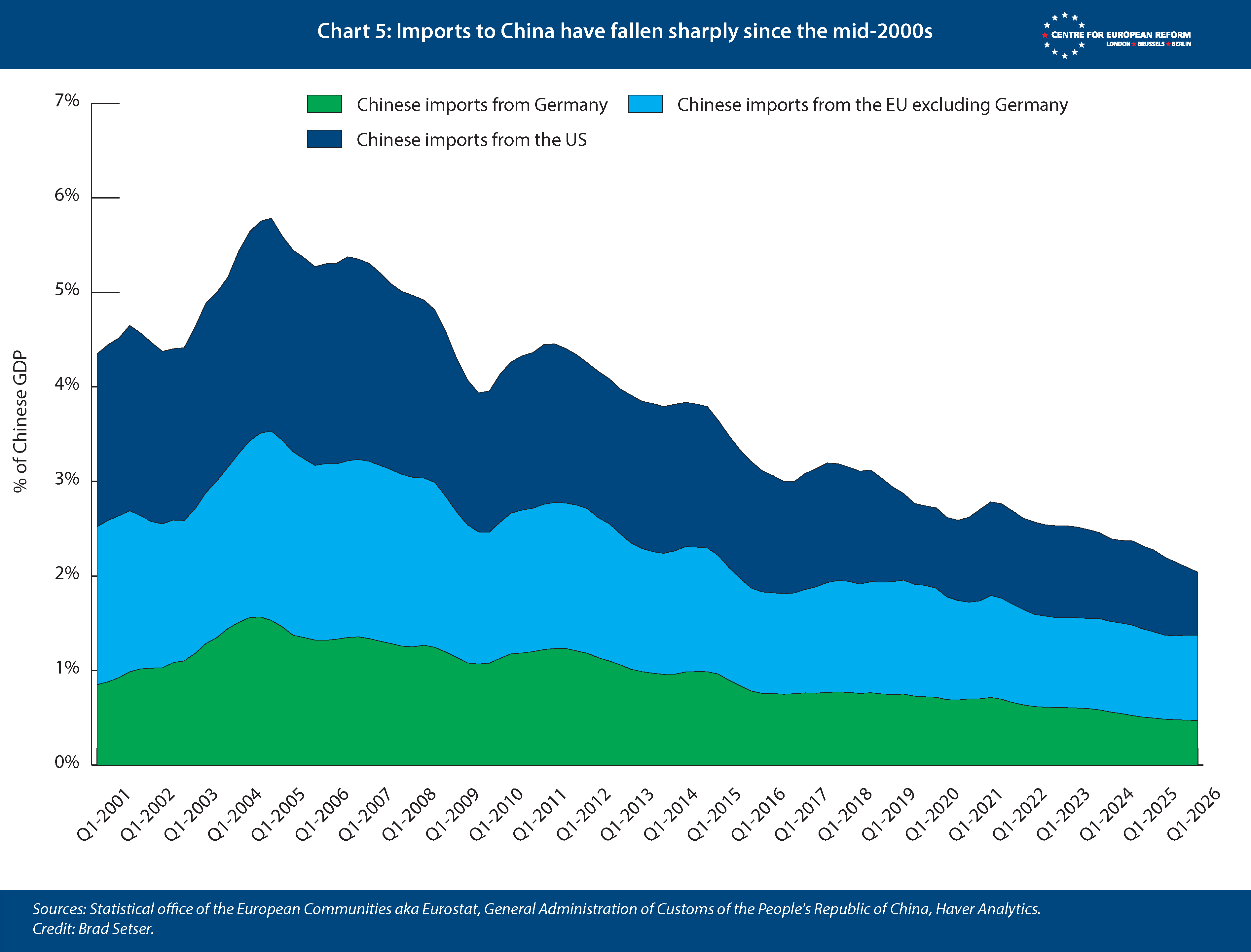

Chinese exports are again surging, but imports are not rising alongside them. In volume terms, Chinese imports have barely grown over the past six years. In dollar terms, manufactured imports, including imported components, have now stalled for a decade; excluding semiconductors, they have fallen outright. China simply does not share demand with trading partners: its imports of manufactured goods relative to GDP have fallen since its 2001 WTO accession (Chart 5). The result is a more than $1 trillion rise in Chinese exports without a balancing rise in imports, and a manufactured goods surplus of around $2 trillion – roughly on par with Italy’s national income.

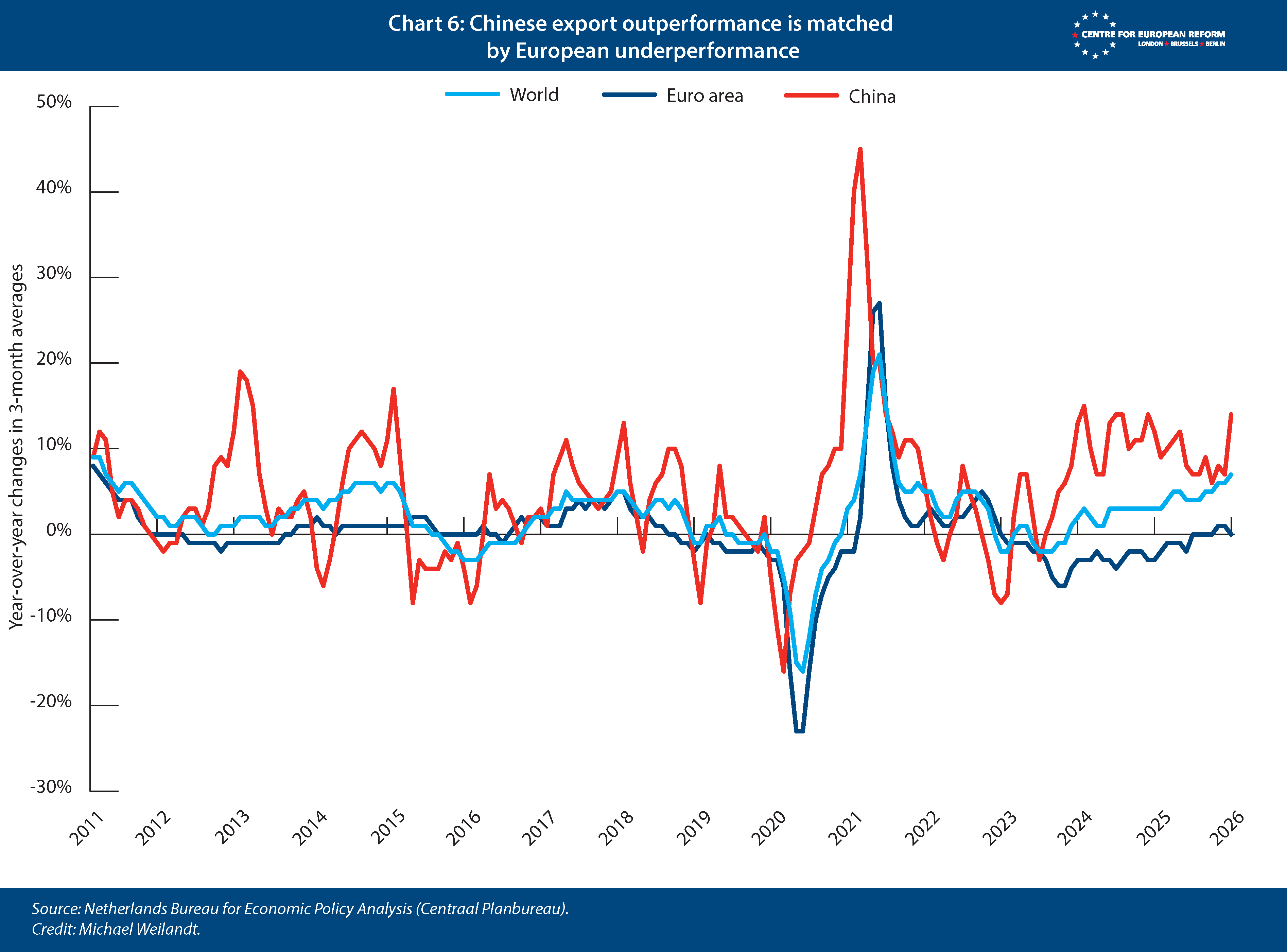

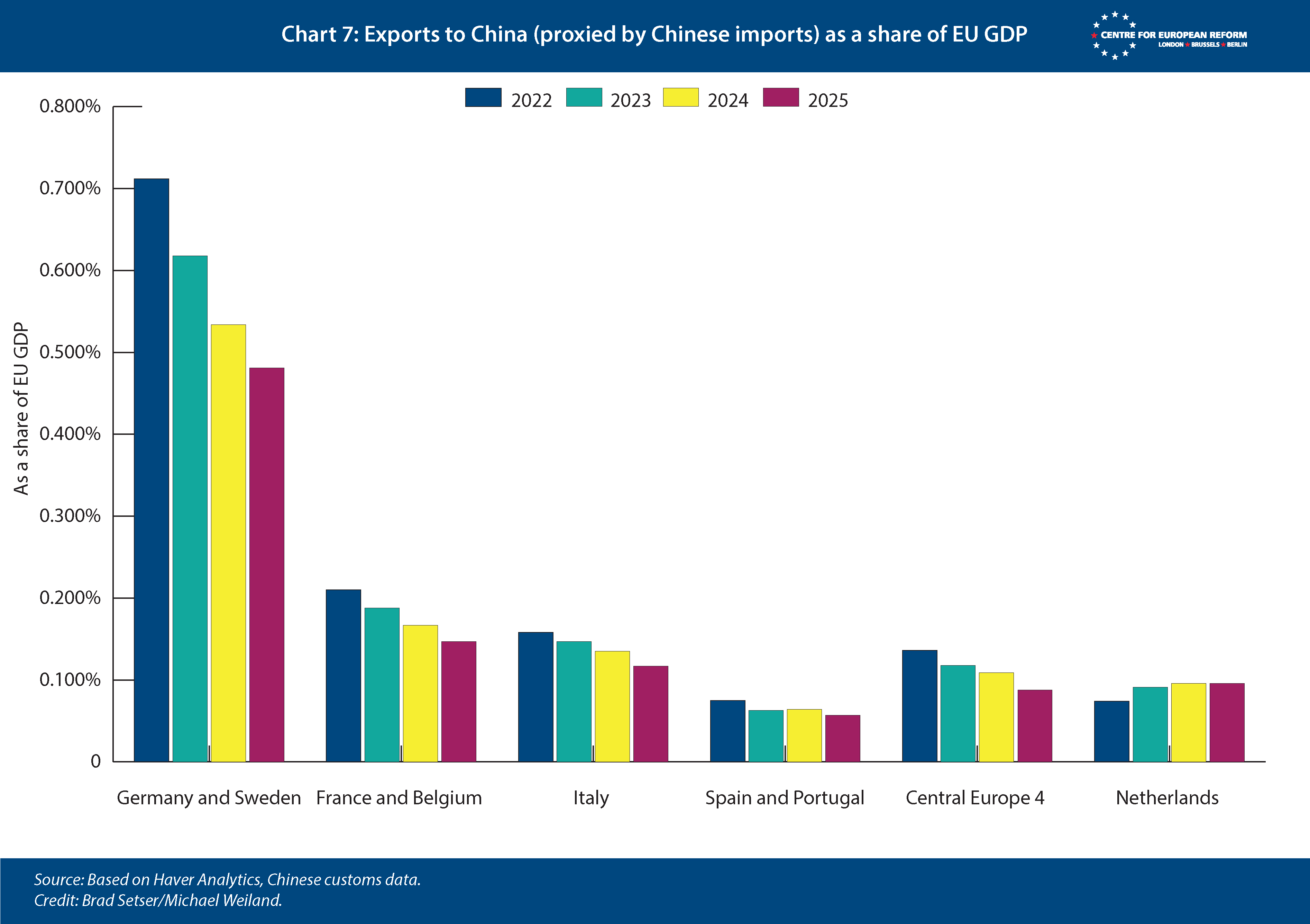

With Chinese exports rising and imports flat, others, by definition, must lose market share. Given the size of Europe’s manufacturing exports, it is hit hard – and Germany, most of all. Chinese export outperformance, growing two times faster than global trade, has been matched by European export underperformance (Chart 6). German exports to China have fallen particularly sharply: by about one percentage point of GDP. German firms are losing market share inside China as domestic champions replace imports, while overcapacity and price war at home pushes Chinese firms to expand aggressively into export markets. But Germany is not alone. All major European countries other than the Netherlands, which is buoyed by Dutch chipmaking equipment giant ASML, have also seen their exports to China fall (Chart 7).

The damage to Germany from losing the China business is substantial. According to Jürgen Matthes of IW Köln, at the peak of the China export boom in 2021, around 1.1 million German jobs depended directly or indirectly on final demand in China – almost 2.5 per cent of total employment.14 Since then, German exports to China as a share of GDP are down by more than 40 per cent. That implies a loss of more than 400,000 Germany-based jobs linked to exports to China, and with current dynamics, there is much further to fall. Demand outside of China may offset some of the jobs tied to this lost production, but Beijing is also pushing German products out of third countries’ markets and increasingly in Europe as well. The Federal Reserve notes the product similarity with China’s exports has risen the most for the eurozone amongst major advanced economies, as China increasingly specialises in Europe’s industrial strengths.15 As a result, those dynamics are mirrored at the sectoral level.

The spectre of Germany’s lost solar industry now looms over its core sectors

China is increasingly dominant in the sectors that form the productive core of Germany’s economy: cars, machinery, specialised chemicals, electrical equipment, aircraft manufacturing and clean tech capital goods. This was well-telegraphed in China’s ‘made in 2025 industrial strategy’. Another one of China’s flagship industrial policy projects, aptly called the ’10,000 little giants’, specifically has targeted Germany’s Mittelstand – its ecosystem of middle-sized, innovative industrial suppliers and firms.16 But Berlin has done little about China’s strategy and is now absorbing the consequences.

A solar spectre haunts these sectors: in 2010, Chinese production of solar photovoltaic (PV) panels depended on imported German equipment. Now, global solar PV production relies on equipment imported from China.

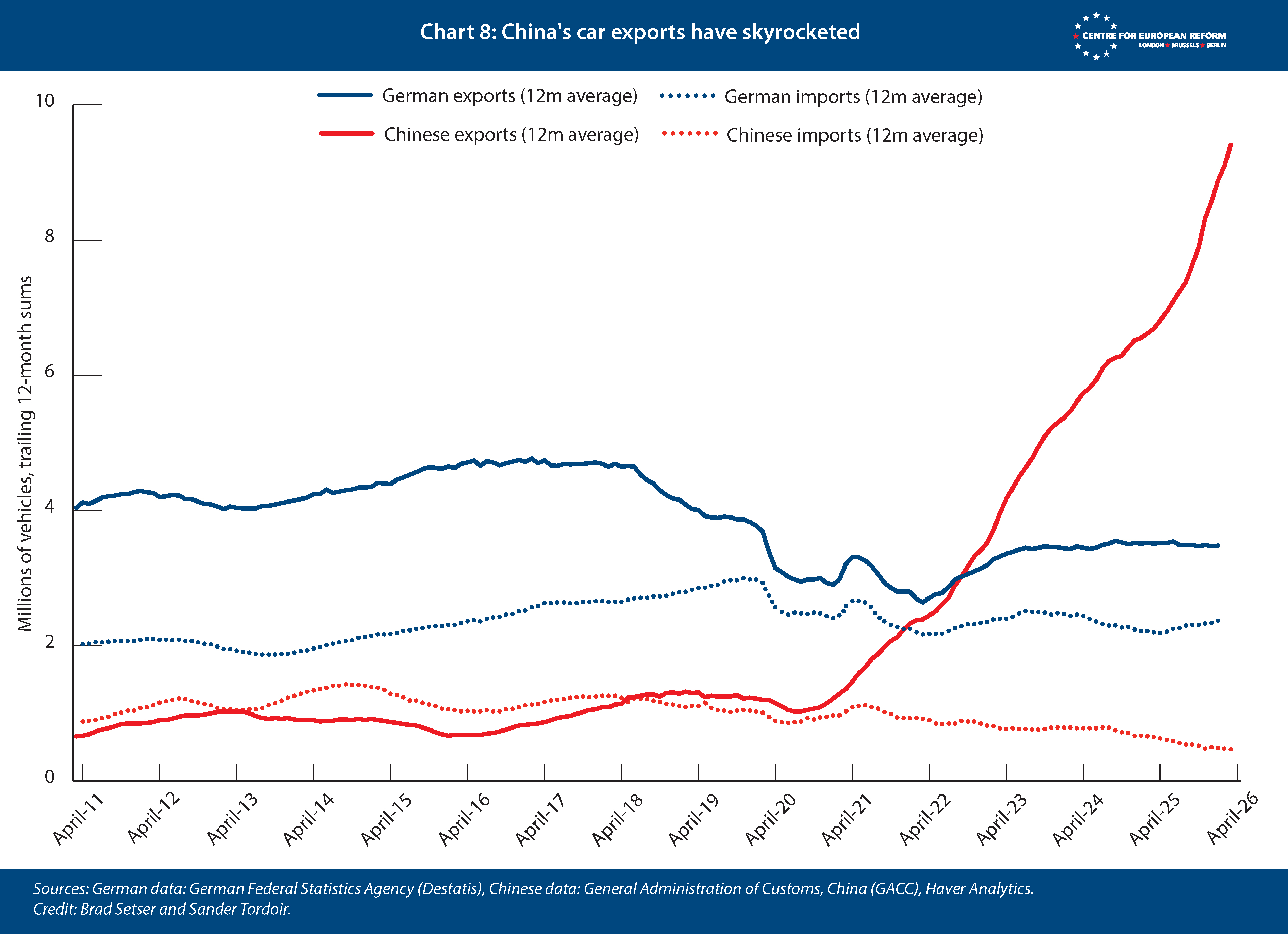

What is especially worrying for Europe’s most car-centric economy is that China’s global car exports continue to surge (Chart 8). China is already by far the world’s largest car exporter, and it still has vast spare capacity to ramp up further.17 It now has factories capable of producing 55 million cars a year, equivalent to around 65 per cent of global demand.18 With a production capacity of at least 25 million electric vehicles (EVs) and a domestic EV market that is only about half that, China is able to meet all incremental global demand for EVs.19 There is substantial pressure on global manufacturers to locate their EV production for global markets in China, to take advantage of the Chinese industrial ecosystem.20

Thanks to 100 per cent tariffs and rules that prohibit Chinese connected vehicle technology, the US market is largely closed to Chinese cars. China itself is also exceptionally closed: it now imports only around 2 per cent of its own 25 million car market. That means Germany and China are effectively competing for the remaining roughly 50 million-car market in the rest of the world – of which China already occupies around 20 per cent. Chinese car exports also show no sign of letting up and have been accelerating over the past few months.

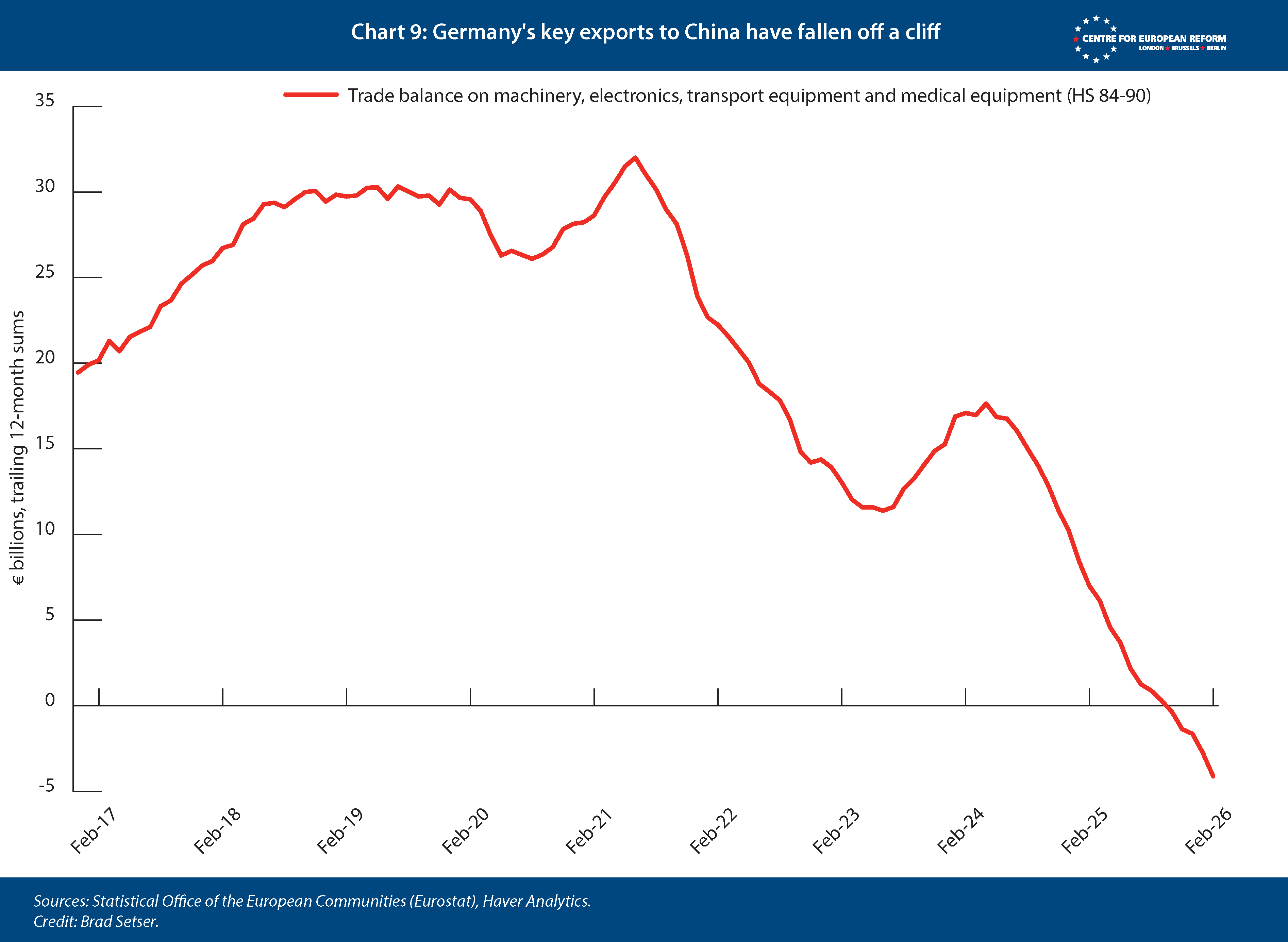

Beyond Das Auto, similar dynamics continue to unfold in a variety of sectors that have long been the hallmark of the German economy. Germany used to dominate the global production of machinery and technology-intensive capital goods. But since mid-2025, Germany has been buying more capital goods from China than vice versa – a symbolically powerful tipping point (Chart 9). Without policy intervention, a wider set of German factories, hospitals and infrastructure nodes will end up being equipped with Chinese machinery and robots, whilst German machine-builders are set to lose their European export markets.

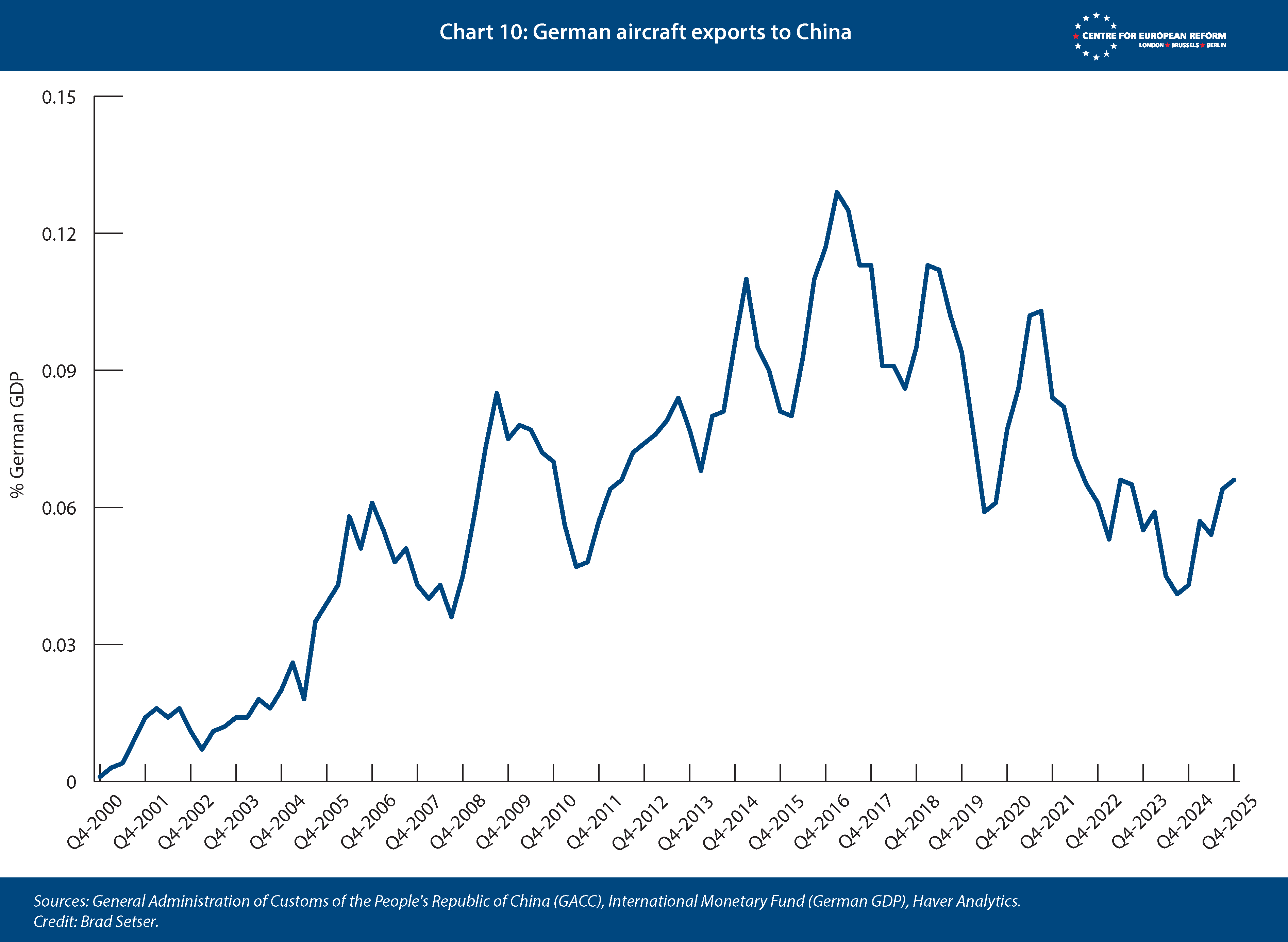

Aircraft manufacturing was one of the last sectors where Germany was still holding its own in China, with Airbus building its A320 family of planes in Hamburg. But even here the outlook is darkening. Germany’s aircraft exports to China have fallen by 50 per cent from their peak, as Airbus has localised its production for China in China (Chart 10).21 Boeing has largely been shut out of China in retaliation for the US tariffs. But China’s own rising production is a long-term threat; even Airbus’s Tianjin output will be squeezed if China succeeds in scaling up production of its indigenous narrow-body aircraft – which it of course will also want to export.

Chinese pressure also continues to strengthen in ‘low-carbon technology goods’ – from gas and wind turbines, nuclear centrifuges and EVs to batteries and building insulation.22 As global decarbonisation drives booming trade in these products, Germany retains strong comparative advantages in several sectors. Under normal trade patterns, countries specialise where they are relatively most efficient and import the rest. Instead, China’s imports of low-carbon technologies have been declining for years, suggesting import substitution driven by a policy of self-sufficiency rather than true comparative advantage (Chart 11). Meanwhile, the rest of the world, including Europe, grows more reliant on Chinese clean tech supply – a trend that will undoubtedly accelerate as firms and households further switch to renewables to manage surging oil and gas prices from the Israel-US war with Iran.

No relief from Washington

For a time, the North American market offered Germany’s car and clean tech makers an important offset from the China shock. EU car exports to North America almost doubled between 2019 and 2024, from $25 billion to just below $50 billion – a business still dominated by combustion-engines but with a rapidly growing share of EVs. Many in Europe feared that the 2022 Inflation Reduction Act (IRA) would result in an investment exodus from Europe as US green subsidies made American production more attractive. But in practice, the combination of rising clean tech demand and limits on Chinese imports pulled in European imports. Germany, as the EU’s clean tech manufacturing powerhouse, benefitted: it exports around $170 billion a year globally in clean tech kit.

The American cushion is now vanishing. The Trump administration has largely scrapped the IRA’s tax credits, restricted federal support for charging infrastructure, and above all imposed new tariffs on European car imports. Under the lopsided August 2025 US-EU trade deal, EU car exports now face a 15 per cent tariff (and President Trump has recently threatened to lift car tariffs to 25 per cent). This represents a six-fold increase over the previous level, comes with plenty of uncertainty and has already led to a sizable decline in EU car exports to the US (Chart 12).

Goldman Sachs estimates that China’s export surge could shave around 0.2-0.3 percentage points off German growth annually to 2029, with Germany and Central and Eastern Europe far more exposed than the UK or the US.23 If Goldman’s model calibration is broadly right, the losses to producers, jobs and investment will far outweigh the gains to consumers from cheaper imports. A 2026 report by the French Prime Minister’s planning office warns that Chinese competition could threaten up to 55 per cent of European manufacturing output over the medium term – 35 per cent in France and a striking 70 per cent in Germany.

There is no doubt that Europe will have to reallocate labour and capital as China shock 2.0 engulfs the world – and supply-side reforms can help. But European industrial history shows the old often gives birth to the new. Airbus grew out of national aerospace champions, while Siemens helped build Germany’s clean tech industrial base. ASML, Europe’s leading semiconductor firm, grew out of the gradual decline of Philips, whose workforce fell from around 400,000 to fewer than 100,000. What mattered was that the key parts of the underlying ecosystem, including optics, machine-building and semiconductors, remained in close proximity to each other. Those capabilities did not collapse, but had the time to recombine, sparking the emergence of a new world-leading semiconductor machinery cluster. Crucially, Dutch authorities supported this process, covering around half of ASML’s R&D budget in its early decades.24

Losing existing sectors too quickly risks pushing Germany into a low-productivity equilibrium.25 Without protection, Deutschland AG will not get Schumpeterian creative destruction, but plain deindustrialisation: factories close, capabilities disappear and the high-productivity replacement never arrives. A pivot to services is no panacea, resting on the false premise that innovation can be separated from production – an assumption that China’s stunning rise shatters. Leaving the China shock unmitigated and unchallenged would be profoundly irresponsible in a world where China has shown it will use its control over key global supply chains as leverage.

Letting diplomacy fail before Europe escalates

Germany is not alone in worrying about China’s growth model. In advanced economies up to $650 billion in economic activity – equivalent to around 12 per cent of G7 manufacturing exports – could be directly exposed to Chinese market-share gains by 2030 if they continue at the current pace.26 Beyond the G7, there has been a global reaction to increasingly one-sided trade with China. In 2025, 52 of the world’s 70 largest economies launched new trade defence measures in response to China’s ballooning exports.27 Countries fear not only lost jobs and factory closures, but also deeper dependence on Chinese supply chains and greater vulnerability to coercion from Beijing.

The best remedy for the second China shock is also the most elusive: macroeconomic adjustment in China itself.

A combination of consumption-led fiscal stimulus, stronger household income support, and reforms to strengthen social safety nets, would reduce exceptionally high precautionary savings and raise internal demand. China can afford it: a 2023 IMF working paper found that the central government had as many financial assets as financial liabilities.28 Concerns that China has lost all room for fiscal manoeuvre conflate weak local government balance sheets with Beijing’s stronger balance sheet.

The best remedy for the second China shock remains the least likely: macroeconomic adjustment inside China.

A revaluation of the renminbi would provide a more immediate fix, slowing down exports, and generating pressure for an offsetting domestic stimulus. Chinese exports respond directly to the renminbi; depreciation predictably is followed by a period when export growth exceeds global trade growth. Conversely, a stronger renminbi would also lift Chinese (international) purchasing power and make imports more attractive. Beijing would undoubtedly only agree to appreciate the renminbi if it had a flanking plan to raise domestic demand.

Unfortunately, China is unlikely to change if left to its own devices. China’s draft 15th Five-Year Plan for 2026-30 suggests Beijing is planning to double down on its state-led industrial strategy. Technological self-reliance, national security and manufacturing expansion take precedence over meaningful consumer-led reforms.

This has led to growing efforts to convince China to change. President Emmanuel Macron was right to put trade imbalances back on the international agenda, saying, “I try to explain to the Chinese that their trade surplus is not sustainable because they are killing their own customers, notably by hardly importing anything from us anymore.”29 The IMF, which initially assumed that the 2020-21 imbalances would narrow on their own as the dislocations from the pandemic waned, also has acknowledged that there is a structural problem.

One new impediment to a united G7 push is that the US currently seems missing in action, particularly on currency issues. After striking a fragile truce in its trade and tech war with China in Busan, Korea, in October 2025, Washington now appears reluctant to pick up the baton of forceful exchange-rate diplomacy.

Germany should fill the breach and back EU, French and IMF pressure to get China to rebalance. After years of falling industrial production and exports, Berlin should no longer fear that discussions about imbalances will rebound on itself. Germany still has a surplus, but size and directionality matter.

Germany’s current account surplus, which peaked at almost 9 per cent of GDP in 2016, is now down to 4.5 per cent of GDP.30 Moreover, Germany has committed to policies that will further reduce its surplus. Its debt-funded fiscal expansion will reduce savings and lift demand for both domestic goods and imports – a shift the IMF has publicly welcomed.31 After shocks from Russia, China and Trump, it was past due for Germany to start using rather than hoarding its fiscal space. German defence spending has offered a lifeline to parts of German industry, with some manufacturers transitioning from civilian products to defence components. But even if defence spending rises to 3.5 per cent of GDP, only a fraction of it will be spent on equipment, and it’s too small a sector to drive demand for all of German manufacturing, which comprises one-fifth of the economy.

Europe’s aggregate surplus is also shrinking. The scale of the post-pandemic shift has been masked by rising earnings on Europe’s holdings of foreign assets, which show up in the current account. But the goods surplus of the eurozone has been shrinking as Chinese firms displace European exports in China and third markets.32 In fact, Europe’s goods surplus essentially disappears if the distortions from Ireland’s tax-avoidance inflated surplus in pharmaceuticals are netted out – a dynamic driven by US pharmaceutical multinationals disguising their sales and profits as exports from Ireland.33

Berlin can credibly argue that Germany’s surplus is being corrected rapidly, and that Europe is no longer defending a surplus model, but its industrial base. Rather than fearing discussions about imbalances, Berlin should play offence, not defence, and support Paris in pushing the IMF and G7 to confront China’s currency undervaluation and one-sided trade model.

Should diplomacy fail, as now seems likely, the EU will have political cover to defend its sizeable home market. Trying to rebuild US and European advanced semiconductor manufacturing was fiscally painful – with Biden’s IRA projected to cost $825 billion before it was rolled back, and the EU’s CHIPS Act adding another $80 billion.34 So is Washington’s current rush to create alternatives to China’s monopoly on the refining of certain rare earths and other militarily and industrially critical minerals. The lesson is that it is far cheaper to defend industrial capacity now than to try to rebuild it from the ashes later. The EU is beginning to move in this direction, but its current approach is too slow and too piecemeal to match the scale of the shock.

Europe’s leaky trade ramparts

The EU’s current toolbox of standard trade defences is ill-suited to handle a systemic shock. The resulting tariffs come in several flavours: anti-dumping duties for unfairly cheap imports, anti-subsidy measures for state-backed rivals and the Foreign Subsidies Regulation for distorted competition inside the single market. The EU launched 33 trade investigations in 2024, followed by another 30 in 2025, and many of those were on China.35 But the investigations are product-specific, time-consuming, administratively cumbersome and can only move forward when there is proof of injury.

It is far cheaper to defend industrial capacity now than rebuild it later after industries collapse.

They are also inherently limited, because many Chinese subsidies flow through the banking system and operate at the economy- or industry-wide level, defying easy measurement and quantification within the product-specific WTO framework. Policy-makers generally lack the hard data on subsidies from local governments – such as free land and machinery – to make a case. The result is a leaky bucket of product-by-product duties – for instance on Chinese truck tyres, but not electric trucks; and on EVs, but not hybrids.

The failure of the EU’s totemic EV duties is telling. Germany opposed the EU’s targeted countervailing duties, even though it was a modest, ‘within the rules’ response – and it passed only thanks to support from more far-sighted member-states like the Netherlands, France and Ireland. The impact of these duties was also over-estimated: a study by the Kiel Institute estimated that higher levies would cut Chinese EV exports by 25 per cent.36 Instead, Chinese car exports to Europe rose by 26 per cent in 2025 to nearly 1.2 million vehicles.37 The reason is simple: Brussels designed tariffs only for battery EVs, with generally modest duties that varied by producer – 9 per cent for Chinese-made Teslas, 17 per cent for BYD, 18.8 per cent for Geely brands, and over 35 per cent for SAIC Motors. Chinese manufacturers simply changed lanes. Monthly Chinese EV sales to Europe have still grown over the past year, but imports of hybrid cars have surged by 155 per cent, quickly becoming the fastest-growing segment of China’s car exports. Meanwhile, just off the coast of the EU, the UK is wide open to Chinese imports, meaning the EU is set to lose its largest export market after the US.

Steeling the EU’s trade defences

One failed tariff line does not invalidate trade defence; it merely shows Europe is still fighting in the wrong way. If China’s overcapacity is economy-wide, Europe’s response cannot be product-by-product. That is why Germany should welcome the European Commission’s recently launched review of its trade defence instruments. But the review itself will take time. Europe needs to respond immediately – or at least by the autumn if the French push on imbalances in the G7 does not generate a material shift in Chinese policy.

One obvious step is to use the existing toolbox, such as anti-dumping and anti-subsidy cases, far more aggressively. The clearest candidate is to extend the anti-subsidy case underpinning the EU’s EV tariffs to Chinese hybrids. Since EVs and hybrids are frequently produced by the same firms, often using overlapping production structures and subsidy regimes, the evidentiary overlap is substantial. This includes Western firms producing in China for the European market, such as Volkswagen. The EU therefore need not replicate the entire subsidy investigation. But the holes in EU trade defence would persist even beyond cars within the transport sector: what about heavy-duty vehicles and electric trucks, and should action cover only electric trucks or all trucks? The same problem exists in chemicals, where duties on products like titanium dioxide or polyethylene terephthalate (PET) do little if Chinese overcapacity simply shifts into adjacent inputs where the EU market remains open. There are also institutional limits: the Commission’s trade directorate simply cannot process enough cases to cover entire sectors, let alone the wider economy, in a timely manner.

An alternative path is for the EU to develop new types of safeguards. Unlike anti-dumping or anti-subsidy cases, safeguards were designed precisely for moments when broad import surges threaten the viability of domestic industry. Under GATT Article XIX and the WTO Agreement on Safeguards, governments can temporarily raise tariffs or impose quotas when imports cause serious injury. The original logic was political as much as economic: safeguards were meant to be a pressure valve for open trade, preserving support for liberalisation by giving governments room to respond to destabilising shocks. But this instrument, too, has become too narrow and cumbersome in practice, requiring product-level investigations. The recent G7 report on global imbalances by Hélène Rey and others floated a broader use of safeguards for exactly this reason, arguing that “sectoral trade tensions, including those linked to trade surges or hard-to-measure non-market practices, should be managed pragmatically within the WTO framework.”38

The EU should push for a broader, more flexible use of safeguards, allowing action at the level of whole sectors rather than individual products. The bloc can act in the spirit of the GATT without waiting for full WTO reform. Brussels could impose 30 to 50 per cent out-of-quota tariffs (i.e. beyond a limited manageable quota of imports subject to a lower rate) on all Chinese cars or machine tools, without getting bogged down in firm-by-firm subsidy calculations. The EU has already moved in this direction on steel, agreeing to double safeguard tariffs to 50 per cent and sharply cut quota volumes. Coupled with rising defence demand, this has helped lift the valuations of leading European steel firms, from Salzgitter to SSAB, suggesting that private capital can be pulled back into European industry if the China shock is credibly countered.39 Safeguards are more vulnerable to Chinese pressure to drive fissures between member-states: unlike the Commission’s standard trade tools, which can only be overruled by a qualified majority of countries, safeguards need to be affirmed by a qualified majority vote.

Safeguards also apply in principle to all trading partners, while Europe’s problem is overwhelmingly China-specific. The easy solution here is for the Commission to exempt its 76 free trade agreement partners – a growing group as Brussels signs new trade deals – and focus safeguards primarily on China. That would be a stopgap to preserve openness to allies while defending Europe’s industrial base.

A European 301

Safeguards are meant to be strictly temporary and time-bound, thereby buying breathing space, but they do not obviate the EU’s lack of a true instrument to respond to China’s economy-wide distortions. The EU needs an instrument to penalise large countries with unbalanced domestic economies, closed domestic markets and an unhealthy reliance on a rising trade surplus for growth that they cannot generate at home. The EU’s anti-coercion instrument (ACI) is powerful but too sweeping – its use should be restricted to actual instances of coercion (for example supply restrictions aimed to force changes in European policy) rather than for sectoral self-defence. The EU needs a tool to occupy the space in between, and the Commission is mulling launching legislation to build it.40

The EU needs a European 301 to confront China’s systemic distortions beyond piecemeal trade defence.

One promising model is America’s Section 301 of the 1974 Trade Act. It allows Washington to investigate and respond to a wide set of foreign practices deemed unreasonable or discriminatory, even when they do not fit narrowly within WTO case law. That makes it a much stronger instrument than classic anti-dumping or anti-subsidy cases: it does not require the US to prove firm-level subsidies, or litigate one product at a time. Instead, the US can impose targeted tariffs on entire sectors and keep them in place for as long as the underlying distortion persists. Washington has used Section 301 across a wide range of disputes, from intellectual property theft and forced technology transfer to industrial overcapacity and forced labour. Currency practices can also fall within its scope: in 2021, the US trade representative (USTR) used Section 301 to challenge Vietnam’s excessive foreign exchange intervention and competitive devaluation.41

The EU should use the Commission’s trade defence review to build a European equivalent. A European 301-type instrument would allow Brussels to respond to systemic distortions that fall outside traditional trade defence – notably China’s persistent currency undervaluation and macroeconomic policies that generate demand externally while suppressing it at home. A 301 does not imply indiscriminate tariffs on all Chinese imports, but flexibility to apply a remedy on key sectors. A 301-style tool would let Brussels flexibly target precisely the sectors that matter most – autos, machinery, chemicals, batteries, clean tech and the semiconductors to build them.

That is likely to be an easier sell than the call of France’s national planning office for a broad 30 per cent tariff on all Chinese imports. It is far easier to keep Germany, the Nordics and business on board if Europe is defending machine tools and cars rather than raising prices on toys, consumer goods and in other sectors where it has little production and little strategic interest. A China-specific EU 301 measure is also easier to defend with trade partners than a broad de facto withdrawal of most-favoured-nation treatment, the cornerstone equal-treatment principle of the WTO. While ideally a 301 would provide the basis for a negotiated change in policy, US 301s are not time-bound and thus a European equivalent would allow Brussels to defend itself for as long as the China shock endures. One possible bargain with China would be that Beijing revalued the yuan in exchange for the EU dropping its 301.

Buy-European industrial policy: A good start, but not yet enough

Tariffs and safeguards can slow the import surge; they cannot by themselves ensure that Europe’s own demand supports European production. That is where industrial policy comes in.

Industrial subsidies in Europe are still primarily decentralised and funded through national budgets. That creates large divergences across member-states and pokes holes in the single market. France has attached de facto buy-European/buy-ally conditions to green subsidies, using battery rules and climate scores for cars that largely exclude Chinese EVs because of their more carbon-intensive production. But other member-states continue to offer consumer subsidies for EVs, heat pumps or other kit with few conditions, effectively supporting already heavily subsidised Chinese products.

A European preference is a symmetrical response to China’s long-standing de facto buy-local industrial policy.

Germany illustrates the problem. In October 2025, the governing coalition committed to equip its new €3 billion subsidy scheme for affordable EVs for low-income households – with the potential to rise to €6 billion through carbon tax revenues – with a buy-European clause. By the time the measure was announced in 2026, however, the clause had disappeared. The environment minister instead stressed that he did not fear China, arguing that Germans would buy local anyway. Undoubtedly, Volkswagen and other German car-making multinationals lobbied to keep the scheme open to their Chinese production. But for the German economy this was strategically short-sighted. German consumers may still buy German brands, but Germany will lose its European export markets to China long before it loses its own home market. Berlin aligning its EV scheme with France could have created a bandwagon effect for a European preference across the EU as a whole.

The Commission’s recently proposed Industrial Accelerator Act (IAA) gives Germany another chance. For the first time, Brussels is not merely giving member-states more room to subsidise strategic sectors; it is imposing obligations on national procurement and subsidy schemes through Union-content requirements and local production thresholds. The most concrete example is in automotive procurement. The Act introduces a three-tier definition of a European vehicle, requiring final assembly in the Union, a 70 per cent local content threshold, and a 50 per cent threshold for critical components. Importantly, this includes subsidised corporate fleet purchases from 2029 – the main channel for existing member-state subsidies, via tax deductions for company cars – and covers about 50 per cent of the market. Firms with major assembly operations in the EU should be able to qualify. China’s WTO commitments have never stood in the way of its own use of such preferences: no imported car or imported battery has ever qualified for a Chinese EV subsidy. A European preference would therefore be a symmetrical response to China’s own de facto buy-local policy.

But the proposal remains too cautious in two ways.

First, public authorities can buy non-Union content if European or eligible partner suppliers are more than 25 per cent more expensive, or 30 per cent in some schemes. But Chinese products are often at least 40 per cent cheaper, precisely because of the distortions the EU is trying to counter. If the thresholds are not tightened, the rule risks becoming a loophole.

Second, the definition of Union content is generous to trading partners, which is right in principle but risky in practice. Counting inputs from the EU’s 76 free trade agreement partners as local content helps keep Europe open to allies and avoids a crude fortress-Europe approach. But it also creates a route for embedded Chinese content to enter through partner countries but count as ‘Union content’.

Industrial policy Tinder with trade partners

Germany, often wary of giving the Commission power, should let the EU use the Industrial Accelerator Act’s envisioned reciprocity tools as needed. If partners keep their subsidy schemes closed to European firms, the Commission can stop their products from qualifying as EU content through ‘delegated acts’, a binding move by the EU executive which can be enacted swiftly and unilaterally.

This matters especially in cars. A handful of mature, like-minded markets – the US, UK, Turkey, Japan, South Korea, Norway and Switzerland – account for around 80 per cent of EU car exports. Many share Europe’s concerns about Chinese overcapacity, but their own subsidy schemes often contain hidden or explicit buy-national filters. Japan and South Korea offer large EV and battery subsidies that disadvantage European exporters through technical rules.42 With the IAA and subsequent delegated acts, the Commission can play industrial-policy Tinder: partners that open subsidy schemes to EU cars, batteries and components qualify for European local content rules and demand incentives; those that do not, or act as conduits for Chinese overcapacity, should not.

As member-states and the European Parliament wrangle over the IAA, Germany should stop watering down the very instruments it will most need. The original draft from Commissioner for Industry Stéphane Séjourné’s team envisaged stricter local content rules, a narrower set of countries qualifying as ‘Union content’ and broader sectoral coverage, including more frontier technologies. During the internal Commission negotiations, however, Germany pushed back strongly. The final proposal was diluted: the list of sectors was narrowed sharply and the definition of eligible foreign content widened substantially. At both the G7 and inside Brussels, France is often defending Germany’s industrial interests more forcefully than Berlin itself.

Chinese foreign direct investment is no free lunch

Despite the strong role of subsidies, currency manipulation and suppressed household demand in driving Chinese exports, a raft of their products, such as EVs and batteries, offer technological advantages. As a result, many in the EU hope that Chinese firms can be induced to transfer technology and production capacity to Europe, to jump-start clean technology production. But this bet suffers from too much optimism and pessimism at the same time.

First, even after rebounding to €10 billion in 2024, Chinese FDI into Europe remains modest.43 China is still a second-tier investor, overshadowed by intra-EU capital and by the US, Japan and South Korea, and ranks only fifth or sixth by FDI stock even in key recipient countries like Hungary. In part this is by design. EU member-states now routinely block takeovers of high-tech and semiconductor firms on security grounds. They have reason to be cautious about Chinese investment. Recent research on a micro-level dataset of over 160,000 firms across 159 countries shows that 41 per cent of China’s overseas investments between 2012 and 2021 were in Europe, and focused on knowledge-intensive industries.44

Tariffs create incentives for Chinese firms to produce inside Europe rather than simply export into its market.

After acquisitions, target firms saw returns on assets fall by about a quarter and patenting flatline, while their Chinese parent firms sharply increased granted patents – trebling overall and quadrupling for state-owned enterprises. That this pattern is unique to China points to firms accepting lower returns to extract technology to China. It’s a cautionary tale: Chinese firms will probably resist transferring technology to Europe in greenfield investments, even where high returns beckon.

At the same time, Europeans are too defeatist. China’s undeniably impressive engineering achievements in batteries and electric vehicles are also occasionally presented as technical accomplishments beyond the reach of European industry. But Europe is not out of the race without Chinese technology transfer: German-designed EVs supplemented by Tesla’s modest Berlin production have already made Germany the world’s 2nd largest producer of EVs, even though it is a far smaller country than the US or Japan.

Chinese firms also will not make investments just to reward European countries that adopt a pro-Chinese foreign and economic policy line. The IAA tries to tackle this problem by setting out criteria that firms from China must meet to get European public contracts or subsidies. These include transferring technology to EU partners, employing more than half of project staff inside the EU, capping foreign ownership in joint ventures at 49 per cent, including at least one EU-based partner, investing at least 1 per cent of global revenue in EU R&D, and sourcing at least 30 per cent of components from within the Union. The proposed application of these criteria is flexible; a Chinese firm would need to meet only four of the six criteria.

But joint ventures are not an alternative to tougher trade policy. China’s modest FDI numbers, compared with China selling goods worth $148 billion to the EU in the first quarter of 2026, show that the Chinese prefer to serve European demand from China as a supply hub rather than localise production. Tariffs create the incentive to produce inside Europe rather than export into the European market – complementing a more natural proclivity for firms to produce locally to be closer to consumers and bring down transportation costs. This is, in fact, the real lesson of China’s experience. Foreign car firms, including Germany’s, needed to produce in China to avoid China’s 25 per cent auto tariff – and to qualify for Chinese public procurement and later EV subsidies. The need to produce in China to sell in China – imports were never more than 5 per cent of the Chinese auto market and are now much lower – created the market conditions that gave China leverage to require foreign firms to form a joint venture with (state-owned) firms.45 And firms that entered the market through joint ventures had a cost advantage over firms that supplied the market from abroad and faced a substantial tariff.

Creating incentives for Chinese firms to produce in Europe will require a similar set of policies. The EU will need a tariff or other limitation on imports that encourages production in Europe, and additional incentives to encourage the formation of joint ventures and the localisation of component production – batteries, drivetrains, automotive semiconductors and the like. Otherwise, Chinese firms will tariff-jump by only doing final assembly in Europe. Europe starts at a disadvantage because its existing, largely national, investment regimes are relatively open. The bloc does not yet have the leverage created by China’s pre-2022 cap on foreign ownership of auto facilities at 50 per cent, which effectively required the creation of a joint venture (without a special exemption like that provided to Tesla).

Bracing for Chinese retaliation

Berlin and Brussels should harbour no illusions: toughening the EU’s trade defences against China may well provoke retaliation. China, in fact, has already threatened to strike back hard on the relatively modest, and deeply Chinese, IAA. China, for example, may block European luxury or agricultural exports – to drive wedges between EU member-states. The EU’s institutions lack the funding to compensate firms or farmers who get hit. But tariff revenues from trade defence instruments against China could be earmarked to fund a compensation mechanism for countries and sectors most exposed to retaliation. Normally, higher customs revenue would reduce contributions by member-states to the EU budget. But member-states could instead choose to earmark tariff income from China for a common compensation fund.

Industrial dependence on China is fundamentally incompatible with any realistic conception of European strategic autonomy.

A back-of-the-envelope calculation suggests the scale of a compensation mechanism could be meaningful. EU imports of machinery, vehicles and parts from China were €300 billion in 2025, implying a 30 per cent tariff could generate up to €90 billion in revenues. In practice, revenues would be lower, as importers substitute to domestic and non-Chinese foreign suppliers. Evidence from the US-China Trump 1.0 trade war suggests sizeable import responses to tariffs, consistent with short-run elasticities around −1 in the first three months, rising to -2 over time.46 Applying this range implies a substantial decrease in import volumes, in the order of 30–60 per cent once substitution occurs, leaving a residual import base of roughly €120–210 billion and tariff revenues in the range of €36–63 billion. A central estimate of €45 billion in tariff revenue annually is therefore more plausible, sufficient to capitalise a meaningful compensation fund while preserving incentives to shift production towards Europe.

More ominously, China has demonstrated that it is willing to weaponise its control over the supply chain for critical minerals, including rare earths, permanent magnets, gallium, germanium and no doubt other products vital to produce anything ranging from cars and rockets to drones, semiconductors and clean tech.47 A new and powerful system of export controls modelled on US controls over chips was part of China’s response to Trump’s 2025 tariff barrage. Europe has to be prepared for the possibility that China will deploy similar measures against European firms should Europe take steps to develop stronger trade defences. China’s ability to cut off key industrial inputs, and its willingness to weaponise its supply of rare earths and critical minerals, could be used as a tool to try to force its trade partners to accept an unbalanced economic relationship.48

Europe, obviously, cannot allow current dependence on Chinese supply in certain key sectors to become broad-based dependence across a range of advanced technologies, including the technologies needed for a clean economy and rearmament. Industrial dependence is at odds with any realistic conception of European strategic autonomy.

There is a strong case for measures to build alternative sources of supply, especially for those rare earths and critical minerals with significant military applications where China now has a de facto monopoly over refining. This argument of course extends to securing sources of supply of automotive semiconductors: more broadly, if a critical industry depends on imports for a small number of essential inputs, the suppliers of those inputs have enormous leverage over that industry. China is in some ways a model for Germany here; it actively pursues policies to develop productive capacity in sectors where it has concerns about dependency – and does not hesitate to build stockpiles in sectors where import reliance is unavoidable.

Europe and its allies should be able to fight back – and there are plenty of actionable proposals on how to do so.49 Take rare earths. In 1990 most rare earth mining still took place in the West, as did over 50 per cent of germanium and almost 90 per cent of gallium refining.50 The International Energy Agency estimates the financing gap (covering both public and private sector investment) for projects outside of China to meet non-China demand at $60 billion for a rare earth mine-to-magnet pipeline.51 The EU and Germany need to catch up: their industrial policy programmes are only a fraction of what Japan and the US are investing to wean themselves off Chinese minerals. The needs are sizeable, but achievable, especially if Germany dedicates some of the hundreds of billions of euros it is investing in defence towards securing raw materials for it.

Defensive measures to eliminate existing vulnerabilities will take time to put into place. In the event that the EU’s broadening of its trade defences is met with retaliatory supply restrictions from China, Europe should be prepared to respond with restrictions of its own, which are easily justified under the EU’s Anti-Coercion Instrument. This is a way to deter China from doing so, although such steps should not be rolled out if tariffs or other trade restrictions are met with offsetting tariffs.

In sanctions policy, countries try to develop ‘escalation ladders’ – starting with more modest steps that signal the ability to take broader and more damaging measures. The Commission needs a similar playbook for supply chain warfare.52 China’s reliance on European chipmaking tools for example, is a high card. Parts of Chinese industry almost certainly also still rely on European speciality chemicals – just as China’s chip industry depends on Japan for highly purified hydrogen fluoride.

It is an unfortunate reality that deterrence is now part of the lexicon of economic policy. At the same time, Europe cannot be afraid to act. Many of the measures now needed to preserve key industrial sectors in the face of super-charged Chinese competition were measures that China itself used to develop its current industrial ecosystem. China cannot easily take actions that would risk the complete loss of access to the European market – particularly at a time when its access to the US market is contingent on successful summitry and the whims of the American president. There is a small number of large markets that can serve as significant outlets for China’s massive industrial capacity. A Europe that is prepared to respond in kind does have significant leverage and scope for action.

Ultimately, an economic power like Europe, with Germany as its industrial heartland, cannot accept a world where current dependence is used to impose an even greater level of future dependence.

Conclusion

Germany is at the heart of China shock 2.0. As a result of the second China shock, eurozone exports are now growing more slowly than global trade, key German export sectors are contracting while industrial production continues to decline. Germany has lost 3 per cent of GDP in net exports since 2023 alone – much of it due to China, and there is more pain to come.

Waiting for the China shock to correct itself is choosing to let deindustrialisation run its course.

Berlin cannot bet that the shock will end on its own. President Xi is ensuring that Chinese production displaces imports in the few sectors where China still depends on global supply. With manufacturing investment still expanding, household demand weak, the property drag unresolved and the currency undervalued, China will continue to siphon demand from the rest of the world. Given its emerging car and machine-centric economy, that will hit Germany especially hard.

Waiting for the shock to correct itself is not prudence, but a decision to let deindustrialisation run its course. Time is running short. More Chinese firms – and foreign firms operating in China – have concluded that the only way to make money in EVs is to use China as an export base. ‘German’ firms are helping lead the shift, ploughing investment into China rather than Europe.53 The risk is that global car production – followed by machinery, clean tech, robots, aviation and semiconductors – concentrates ever more in China, withering R&D and engineering in traditional centres of advanced manufacturing like Germany.

Berlin cannot keep admiring the problem. EVs, top machine tools, industrial robots, chemicals and planes are advanced engineered goods. These sectors do not only account for a large share of German and European R&D spending; alongside information technology, they were among the fastest contributors to productivity growth between 2012 and 2022. They are worth defending.

Germany should support Brussels’ efforts to steel Europe’s trade defences, use public demand to support European production, and prepare for Beijing’s retaliation. Unlike the US, the EU has significant potential to continue to pursue openness with partners. The EU can co-ordinate trade defence measures and negotiate reciprocal access to industrial policy incentives with its growing roster of 76 FTA partners – many of whom, from Japan to Canada and Türkiye, are equally worried about China’s export juggernaut.

A China that is on course to account for 40 per cent of global manufacturing by 2030, while growing exports and compressing imports, will inevitably create more chokepoints like those it already controls in rare earths, active pharmaceutical ingredients, and chip packaging and testing. German dependence on Chinese supply chains will affect Europe’s ability to rearm, support Ukraine and reduce its own economic vulnerabilities. The longer Germany waits, the larger and more disruptive the eventual response will have to be.

2: European Commission, ‘Simplification’.

3: Sander Tordoir and Brad Setser, ‘How German industry can survive the second China shock,’ CER policy brief, January 2025.

4: Martin Ademmer and Jamie Rush, ‘Germany insight: How 5 per cent of GDP got lost, most of it forever’, Bloomberg Intelligence, December 13th 2024.

5: Brad Setser, ‘China’s massive surplus is everywhere (yet the IMF still has trouble seeing it clearly)’, Council on Foreign Relations, November 2025.

6: IMF’, 2025 China Article IV consultation’, December 2025.

7: Daniel Garcia-Macia, Siddharth Kothari and Yifan Tao, ‘Industrial policy in China: Quantification and impact on misallocation’, IMF working paper, August 2025.

8: Katie Martin, Robert Armstrong and Joe Lehay, ‘Transcript: China shock 2.0’, Financial Times, April 24th 2026.

9: Keith Bradsher, ‘Why Volkswagen is building a team of 3,000 engineers in China’, New York Times, December 12th 2023.

10: ‘Why the IMF’s newest report finds that the yuan is undervalued’, The Economist, February 19th 2026.

11: Brad Setser and Mark Sobel, ‘It’s time for China to let the renminbi appreciate sharply’, OMFIF, November 2025.

12: Daron Acemoglu, David Autor, David Dorn, Gordon Hanson and Brendan Price, ‘Import competition and the Great US employment sag of the 2000s’, Journal of labor economics, January 2026. Also see David Autor, David Dorn and Gordon Hanson, ‘On the persistence of the China shock’, NBER Working Paper, October 2021.

13: Justin Pierce and Peter Schott, ‘Trade liberalization and mortality: Evidence from US counties’, American Economic Review Insights, March 2020.

14: Jürgen Matthes, ‘Immer wenig Jobs vom China-Geschäft abhangig’, Institut der Deutschen Wirtschaft, February 2026.

15: Francois de Soyres, Ece Fisgin, Alexandre Gaillard, Ana Maria Santacreu and Henry Young, ‘The sectoral evolution of China’s trade’, Federal Reserve, February 2025.

16: Alicia García-Herrero and Robin Schindowski, ‘Unpacking China’s industrial policy and its implications for Europe’, Bruegel, May 2024.

17: See for example Alice Li, ‘China will be exporting 10 million cars per year by 2030, association forecasts’, South China Morning Post, September 23rd 2025.

18: ‘Massive overcapacity threatens to prolong China’s car price war’, Bloomberg, June 19th 2025.

19: Brad Setser, ‘Will China take over the global auto industry?’, Council on Foreign Relations, December 2024.

20: Gregor Williams, ‘Why are Chinese EVs so cheap?’, Rhodium Group, February 2026.

21: Airbus, ‘Airbus opens second A320 family final assembly line in China’, press release, October 22nd 2025.

22: ‘Trade in low carbon technology products’, IMF, last updated November 25th 2026.

23: Joseph Briggs, Megan Peters and Sarah Dong, ‘Beggar thy neighbor: Sizing global spillovers from our recent China GDP forecast upgrades’, Goldman Research, November 2025.

24: Marc Hijnk, ‘Focus: The ASML way’, Uitgeverij Balans, 2024.

25: Ambrogio Cesa-Bianchi, Andrea Ferrero, Luca Fornaro, Martin Wolf, 'Industrial policies, global imbalances, and technological hegemony', Barcelona School of Economics (BSE) working paper, January 2026.

26: Camille Boullenois, Malcolm Black and Alessia Caruso, ‘China’s next generation industrial policy’, Rhodium Group prepared for US Chamber of Commerce, May 2026.

27: MERICS, ‘Many countries launch new trade measures – but China’s exports just keep growing’, February 2026.

28: Waikei Raphael Lam and Marialuz Morena Badi, ‘Fiscal policy and the government balance sheet in China’, IMF, August 2023.

29: ‘France’s Macron threatens China with tariffs over trade surplus – Les Echos’, Reuters, December 7th 2025.

30: Bundesbank, ‘German balance of payments in 2025,’ monthly report, March 2026.

31: Kristalina Georgieva, ‘Opportunity in a time of change’, IMF, October 8th 2025.

32: Bert Colijn and Amrita Naik Nimbalkar, ‘The eurozone’s goods trade surplus is under structural threat’, ING, April 2026.

33: Ireland reports a current account surplus of around 15 per cent of its inflated GDP – a number that says little about the competitive position of German or European manufacturing and a lot about the tax strategies of Apple, Microsoft and big US pharma companies.

34: ‘US clean energy tax subsidies to cost $823 billion over ten years, CBO says’, Reuters, January 17th 2025. Also see Congressional Budget Office, ‘Estimated budgetary effects of HR 4346’, July 21st 2022.

35: Claus Zimmerman and Giovanna Ventura, ‘Annual report on EU trade defences: Activities reach record high in 2024’, Ashurst, July 2025.

36: ‘EU tariffs against China redirect trade of EVs worth almost USD 4 billion’, Kiel Institute for the World Economy, May 2024.

37: ‘How Chinese cars are beating European tariffs’, The Economist, December 18th 2025.

38: Chong-En Bai, Gita Gopinath, Hélène Rey and Axel Weber, ‘G7 economists memo on global imbalances’, March 2026.

39: Jack Ryan, ‘ArcelorMittal sees European steel tariffs restoring profits’, Bloomberg, February 5th 2025.

40: Noah Barkin, ‘Watching China in Europe – May 2026’, Substack.

41: Of course, such instruments can be misused too: there is a real argument that China’s practices and policies generate systemic overcapacity in sector after sector; there isn’t much of a case that every country in the world is a mirror image of China.

42: Japan METI, ‘Subsidies upgraded for the purchase of clean energy vehicles towards the realization of GX in the automobile sector’, July 2024.; Yong-Hee Kwak and Il-Gue Kim, ‘Korea’s new EV subsidy plan favours Hyundai over Tesla, other imports’, Korea Economic Daily, Feburary 3rd 2023.

43: James Green and Sander Tordoir, ‘Europe’s door to Chinese tech investment is still ajar’, CER insight, March 2026.

44: Jennie Bai, Luc Laeven, Yaojun Ke & Hong Ru, ‘China’s global ownership’, National Bureau of Economic Research (NBER), May 2026.

45: Jie Bai, Panle Jia Barwick, Shengmao Cao, and Shanjun Li (2025). ‘Quid pro quo, knowledge spillovers, and industrial quality upgrading: Evidence from the Chinese auto industry’, American Economic Review, October 2025.

46: Mary Amiti, Stephen Redding and David Weinstein, ‘Who’s paying for the US tariffs? A longer-term perspective’, AEA papers and proceedings, May 2020.

47: Joris Teer, ‘China’s critical minerals weapon and how to disarm it’, EUISS, May 2026.

48: Merics, ‘Merics forum: How can the EU navigate China’s rare earths export controls’, October 2025; also see Christian Shepherd and Lyric Li, ‘China’s rare-earths power move jolted Trump but was years in the making’, Washington Post, October 14th 2025.

49: See footnote 47.

50: See footnote 47.

51: IEA, ‘Rare earth elements’, April 2026.

52:Tobias Gehrke, 'Beijing hold 'em: European cards against Chinese coercion', ECFR, May 2026.

53: Rene Wagner and Christoph Steitz, ‘Exclusive: German firms’ investments in China boomed in 2025 on US worries’, Reuters, January 27th 2026.

Sander Tordoir is the chief economist at the Centre for European Reform and Brad Setser is the Whitney Shepardson senior fellow at the Council on Foreign Relations

May 2026

View press release

Download full publication

This paper was written as a CER collaboration with Brad Setser from CFR. The mission of the Council on Foreign Relations is to inform US engagement with the world. Founded in 1921, CFR is a nonpartisan, independent national membership organization, think-tank, educator, and publisher, including of Foreign Affairs. It generates policy-relevant ideas and analysis, convenes experts and policy-makers, and promotes informed public discussion – all to have impact on the most consequential issues facing the United States and the world.

The Council on Foreign Relations takes no institutional positions on policy issues and has no affiliation with the US government. All views expressed in its publications and on its website are the sole responsibility of the author or authors.

Related content

Industrie européenne : "La pression chinoise s'exerce sur trois fronts, c'est sans précédent !"

CER Podcast: Unpacking Europe: How can Europe survive Trump's tariffs and a second China shock?