How German industry can survive the second China shock

- Industrial production in the EU’s largest economy has been declining for over five years, a source of profound angst in a country where manufacturing contributes around 5.5 million jobs and 20 per cent of gross domestic product (GDP).

- Germany is starting to realise that China’s new automotive, clean technology and civil aviation industrial base directly competes with Germany’s manufacturing foundation. China’s macroeconomic imbalances now directly infringe on German industrial interests.

- Since the property bubble burst in 2021, China has doubled down on directed investment in priority manufacturing sectors, despite a lack of internal demand for much of its output. The result has been a turn back toward export-led growth, with Chinese exports (in volume terms) wildly outperforming global trade in 2024, while German exports in capital and durable goods shrank.

- Germany was relatively sheltered from the initial China shock immediately before and after the country’s accession to the World Trade Organisation (WTO) in 2001. Then, China’s exports were in consumer electronics, furniture, apparel and household appliances – not the automotive and engineering sectors at the heart of the German economy. Wage restraint and the cost-savings from expanding supply chains to Central and Eastern Europe created a German competitive export sector able to benefit from Chinese and American demand for machinery.

- That is no longer the case: China’s economy is much larger; its industry now produces the same goods as Germany and its export-biased growth is cutting into Germany’s European and global export markets.

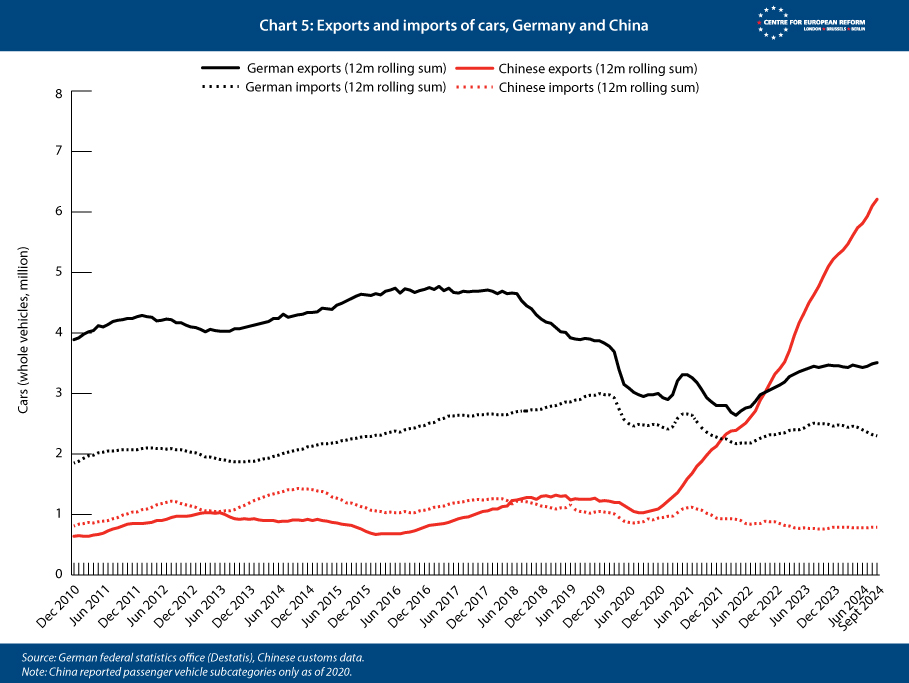

- Cars represent the tip of the spear. China was not a net exporter of vehicles in 2020, the year of the pandemic. It now exports 5 million more vehicles than it imports. The comparable number for Germany is 1.2 million, down by half from its pre-pandemic peak. Germany’s green industry, the largest in the G7, equally faces a growing competitive threat from Chinese green industrial policies.

- To weather the China shock, a new German government must rethink its policies:

- First, Germany should abandon its past opposition to scrutiny of large trade surpluses. It should join the US and the other large G7 economies in encouraging the International Monetary Fund (IMF) to prioritise policies to reduce China’s surplus – starting with a serious examination of how China’s $1 trillion goods surplus largely disappears in the reported current account data. This means supporting some historically un-German policies, notably pressing Beijing to use the central government’s fiscal space to lift domestic demand.

- Second, Germany should support EU protection of viable European industrial sectors facing an onslaught as a result of China’s active industrial policies. At the same time, it should allow cheap imports in areas where Europe has little to no manufacturing. China’s widespread use of subsidies creates ample scope for WTO-consistent duties, such as the ones the EU pursued for electric vehicles (EVs).

- Third, Germany and other EU countries should equip existing and new subsidy schemes with de facto buy-European requirements to offset China’s own local content requirements. The EU currently lacks sufficient common funding for an ambitious industrial policy, but it can tighten single market regulation to ensure EU countries align their national subsidies, for example by linking them to environmental and labour standards which China cannot meet.

- Fourth, Germany should lead on designing a unified EU industrial policy. Customs income already belongs to the EU and the growing tariff revenue from Europe’s trade defence instruments could be earmarked to fund a common policy.

- Germany, with its low debt levels and endangered industrial base, has both the policy space to act and the most to lose if it does not. But it cannot act alone against the new Exportweltmeister. As Henry Kissinger once quipped, Germany is “too big for Europe and too small for the world.”

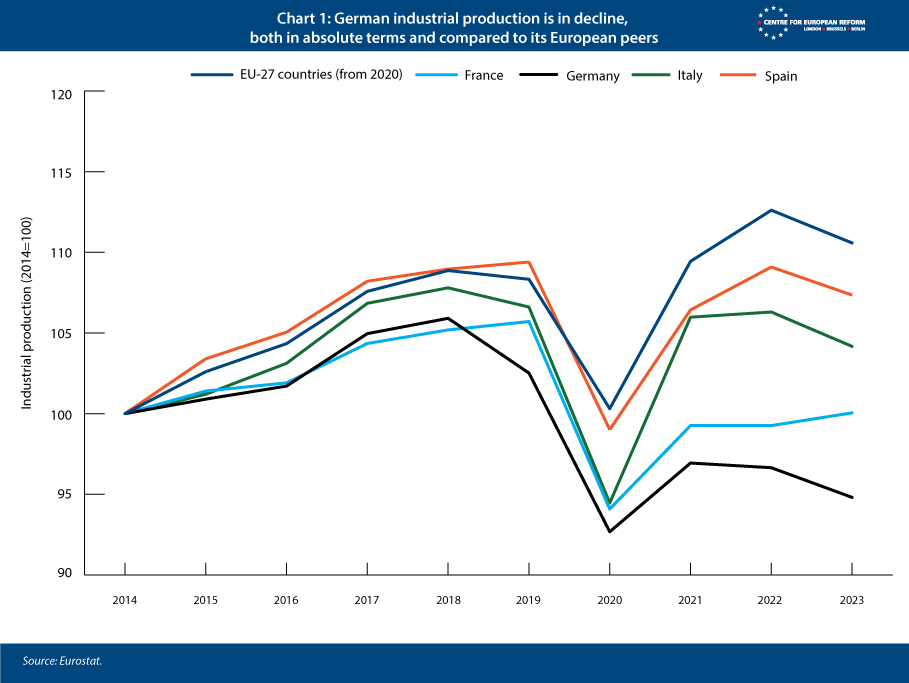

As Germany heads for federal elections in February 2025, a spectre is haunting the country – the spectre of deindustrialisation. German industrial production is way below its 2018 peak, and started declining earlier, and faster, than in other eurozone countries (see Chart 1).1 Some firms, like Volkswagen (VW), are now negotiating possible German plant closures and mass layoffs.2 This is not a function of shrinking global trade, as global trade continues to expand. China’s growing imbalances, to which Germany is uniquely exposed, are a more likely culprit.

China’s increasing technical sophistication, its political commitment to invest in, and subsidise, advanced manufacturing and its low level of demand pose a clear challenge to all advanced economies – the US as much as Germany. For all the talk about deglobalisation and the need for supply chain diversification, the global economy – including the large European countries – is becoming more, not less, reliant on Chinese supply in key sectors.3

Donald Trump’s re-election is likely to create new points of tension between the EU and the US. Trump’s concerns about China’s surplus with the US are likely to result in measures that exacerbate the threat that China’s imbalances pose to EU industry.4 If the US imposes widespread sizeable tariffs on China – as Trump says he intends to do – even more of China’s excess production will be redirected to the European market.

But Germany’s politics have still not caught up with the risks that its economic model is facing. Rather than recognising Chinese industrial policies in clean energy sectors as a clear threat to Germany’s industrial leadership, it opposed EU tariffs on Chinese electric vehicles. The EU's targeted countervailing duties – a modest, ‘within the rules’ response compared to trade practices employed by both the Trump and Biden administrations – passed thanks to support from more far-sighted members of the Union like the Netherlands, France and Ireland. Such countervailing duties are specific tariffs imposed to offset the effects of foreign government subsidies on imported goods.

Without German support, the EU may struggle the next time it tries to stand up to Beijing. Doing so in collaboration with Washington will be challenging under Trump, who is aggrieved by Germany’s bilateral trade surplus with the US. But fundamentally the US and EU share the same concern about Chinese overcapacity. If Germany wants to avoid rapid deindustrialisation, with significant, geographically concentrated losses in jobs and productivity, its new government must urgently rethink its trade, industrial and fiscal policies. This paper looks at the causes and consequences of China’s surpluses, and sets out what Germany needs to do to mitigate their effects.

Beijing’s new industrial policy – and Berlin’s response to date

Chinese manufacturing exports and the associated trade surplus surged over the last four years, rising by as much as they did, relative to world GDP, in the years immediately following WTO accession in December 2001. China is suffering from anaemic domestic demand while increasingly channelling credit to expand production in sectors where it had wanted to catch up with advanced economies. In many of these sectors, it is now also showing genuine technical innovation. As a result, the country is taking a dominant share of the global market in an ever-expanding set of industrial sectors.

China is taking a dominant share of the global market in an ever-expanding set of industrial sectors.

The EU has been slow to respond to the new ‘China shock’.5 But the Union is starting to make greater use of standard trade defences. In response to China’s subsidies, it recently imposed higher tariffs (countervailing duties) on Chinese EVs. The duties vary by manufacturer and the subsidies they have received: Tesla received the lowest duty at 7.8 per cent and SAIC Motor faces the highest at 35.3 per cent (on top of existing base duties of 10 per cent). The European Commission has also initiated investigations and measures against Chinese subsidies for a wider swathe of products including wind turbines. Several former and current EU officials, including Commission president Ursula von der Leyen and former competition commissioner Margrethe Vestager, have expressed concerns about China’s policies. They have even at times hinted that the country’s overcapacity created by state subsidies may warrant the development of new trade instruments.

The broad challenge China’s industrial policies pose to its trading partners is now clear. Beijing identifies priority sectors for its industrial policy, often sectors where China has historically relied on imports from trading partners like Germany and the US. Ambitious local governments then back local firms seeking to enter one of these industries, supported by easy access to credit from a state-dominated banking system that is expected to support national policy goals. These policies sometimes spawn innovative local, and even global, champions but result in national markets that are oversupplied as the expansion of production capacity is disconnected from domestic demand.

Overcapacity and the associated downward pressure on margins and prices also create difficulties in China itself. The number of loss-making Chinese industrial firms has been steadily rising over time.6 Only two home-grown automobile companies – BYD and Li Auto – are reportedly profitable, and 30 rivals are under pressure to stem losses even as sales rise and China’s car exports boom.7 Several Chinese EV producers have had to get new equity investments from supportive local governments to keep operating.

The consequence of this industrial policy is that other countries’ exports are squeezed out of China’s own market, and the stronger Chinese firms look to escape vicious internal competition by developing export markets (often with state support). This is what happened in China’s EV market. China developed its electric vehicle market and production capacity when the domestic market for traditional cars was already oversupplied. So the rise in domestic EV sales created pressure to use existing production capacity for internal combustion engine (ICE) carmakers to instead supply the global auto market.8

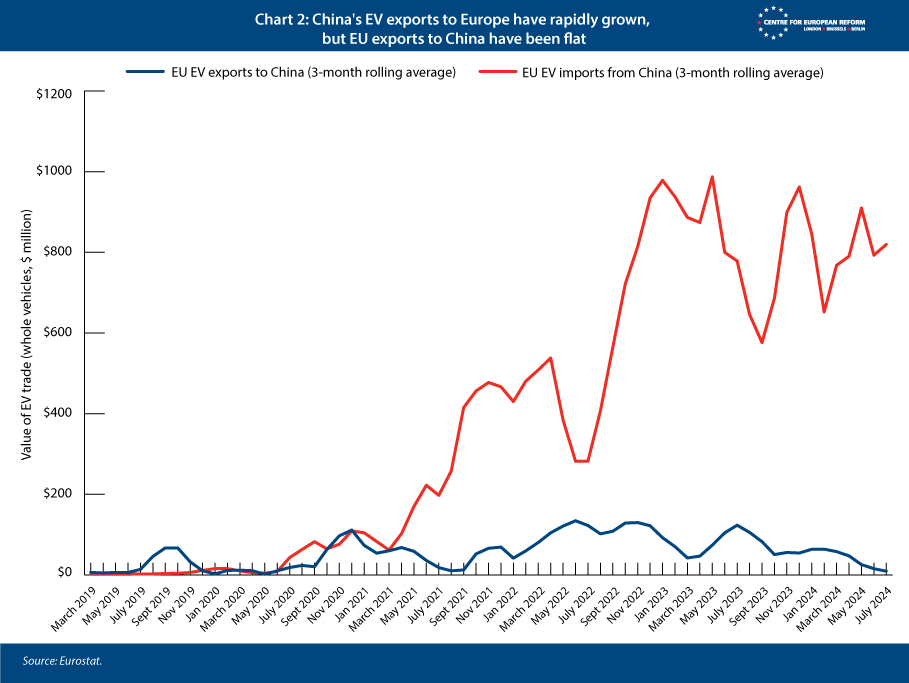

China’s industrial model has a direct impact on the EU and Germany: EU EV exports to China, for example, are negligible, while the EU’s EV imports from China have surged since the start of 2022 (Chart 2).9 Tesla, for example, has supplied the EU market exclusively from China for two years.

Germany, the most auto-centric of the large EU economies, has the most to lose if Chinese industrial policies transform China from a net importer of EU automobiles into a competitive supplier of middle- and up-market cars to the EU. Yet last year Germany was one of the few member-states to vote against the EU’s WTO-consistent countervailing duty decision on Chinese electric vehicles.10 Chancellor Olaf Scholz seems to have been intimidated by the prospect of China raising tariffs on Germany’s already falling exports of luxury ICE sedans to China, as well as Volkswagen’s concerns that China might retaliate against its “in China, for China” business – its factories that produce locally for the Chinese market. It is possible that VW was also hoping to join Tesla in using its new 75 per cent German owned EV factory in China to supply the European market. It is notable that Europe’s traditional free-trade bulwarks like the Netherlands, Ireland and Denmark all backed the tariffs, which were grounded in a detailed investigation into China’s subsidies in this sector.

Had Scholz succeeded in overturning the EU car tariffs at the 11th hour, it would have vindicated China’s efforts to lean on individual member-states. Not only would that have damaged the long-term prospects of Germany’s own car-sector and that of Europe at large; it would have also undermined the EU’s efforts to forge a coherent foreign economic policy. EVs are uniquely prominent, but they are only one of many sectors where China’s industrial policies are leading its companies to go global.

A tale of two China shocks

This is not the first ‘China shock’ to hit global markets. China’s manufacturing exports exploded in the years following its WTO entry in 2001, turbo-charged by provincial governments who rolled out the red carpet for foreign firms looking to manufacture in China. An undervalued exchange rate, sustained by record intervention in the foreign exchange market, played its part too.

This time China’s exports are in the automotive and engineering sectors at the heart of the German economy.

Particularly after China clamped down on internal credit growth in 2004, it started to export far more manufactured goods than it imported. This rapid and asymmetric expansion of trade put pressure on manufacturing in the advanced economies. David Autor and his co-authors have shown that the manufacturing-heavy regions of the US lost one million manufacturing jobs during this period, leaving an enduring imprint in states like Pennsylvania, Michigan, Ohio, North Carolina and parts of Georgia.11 Many workers responded to this shock not by moving to other parts of the country with lower unemployment, but by dropping out of the labour market – in some cases devastating entire communities. Parts of Italy, the UK and France experienced a similar dynamic.12

German industry was sheltered from the first China shock. German firms themselves were relatively cost-competitive, after reaping huge gains by expanding supply chains to Eastern European countries that joined the EU in 2004, and from the wage restraints negotiated with German unions. But more importantly, China’s initial export success came in sectors like consumer electronics, furniture, apparel and household appliances – not in the automotive and engineering sectors at the heart of the German economy.

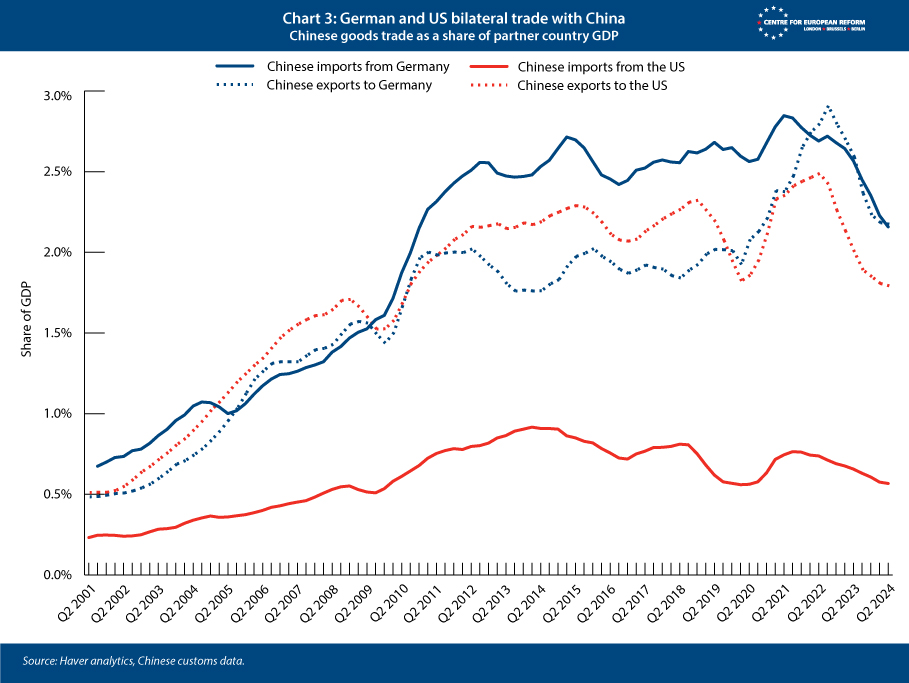

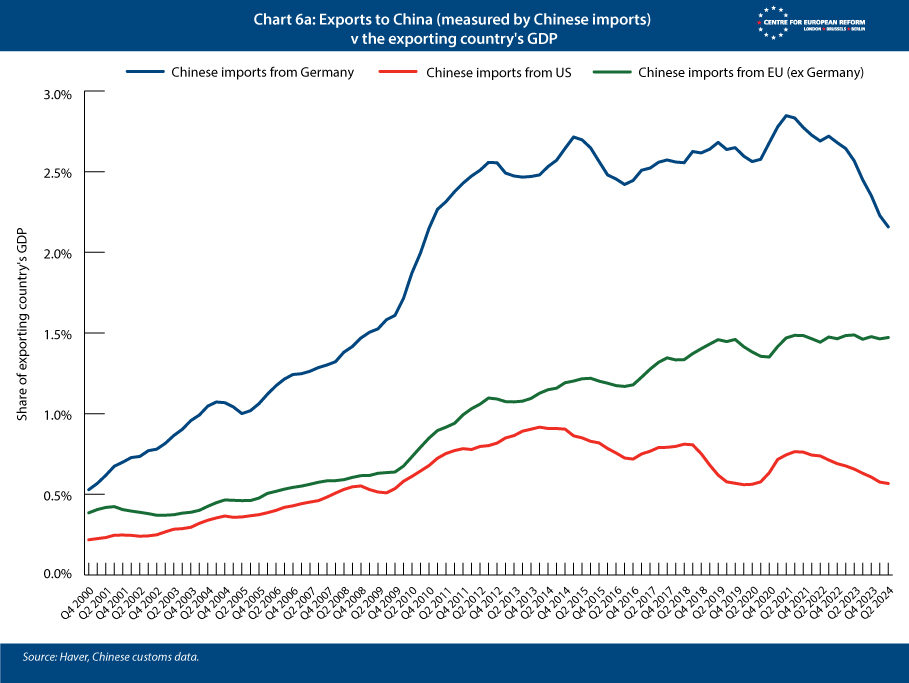

One of the ironies of this period was that Germany ended up benefitting more than the US from the pressure Washington exerted on China to scale back its intervention in the currency market and allow the yuan to appreciate. Germany left this fight to the US. But the yuan’s rise from 2007 to 2012, together with China’s own domestic stimulus, created a cohort of Chinese entrepreneurs who were able to afford German luxury cars. By 2012, German exports to China were about three times more important to the German economy than US exports to China were to the US economy (see Chart 3).

But Germany’s success at supplying cars and industrial machinery to the growing Chinese market between 2004 and 2012 left the country poorly prepared to respond to the next China shock.

The ongoing second China shock has multiple causes. As the Mercator Institute for China Studies (MERICS) and the Kiel Institute have documented, China’s long-term effort to catch up with leading producers in cutting-edge sectors started to pay dividends, benefitting from a mix of protectionism, subsidies and competition between regions to develop Chinese national champions.13 China is a competitive producer of cars, specialist chemicals, and many machine tools – and it now dominates many clean technology sectors. One famous example: in 2010, Chinese production of solar Photovoltaic (PV) panels depended on imported German equipment. Now solar PV production globally relies on equipment imported from China.

But industrial policies on their own would only generate successes in some sectors – they would not typically generate a big rise in China’s overall trade surplus. The second rise in China’s trade surpluses also reflects renewed surging internal imbalances in China’s economy, as the drag from low levels of domestic household consumption is no longer masked by a turbo-charged property sector. Private consumption expenditure accounts for 68 per cent of GDP in the US and around 52 per cent in Germany and the EU.14 But private household consumption makes up less than 40 per cent of China’s GDP, an exceptionally low level even for a high-saving Asian economy.15

High savings are the flip side of low consumption, and after the global financial crisis, China’s property sector absorbed a significant portion of the economy’s excess savings and put them into construction work at home. But now that the real estate bubble has burst, the IMF expects China’s real estate investment to be cut roughly in half.16 This prolonged structural decline in property investment is depriving China of its key growth driver, reducing household confidence and consumer spending.

If domestic consumption is flat and production capacity is rising, exports are the only means to achieve growth. It is therefore no accident that the slump in China’s property sector has coincided with a large increase in China’s customs trade surplus. Exports had been shrinking as a share of China’s economy between 2008 and 2018 – but that has reversed in a big way. Chinese exports continue to outpace global trade: in 2024, Chinese exports were up 12 per cent or more in volume terms, while global trade is growing at around 3 per cent. Chinese import volume growth, meanwhile, has declined significantly.17

China’s manufacturing surplus is now 10 per cent of its GDP – a staggering number.18 As The New York Times recently noted, US trade surpluses in manufactured goods peaked at 6 per cent of American output early in World War I, at a time when factories in Europe switched to wartime production and mostly ceased exporting.19

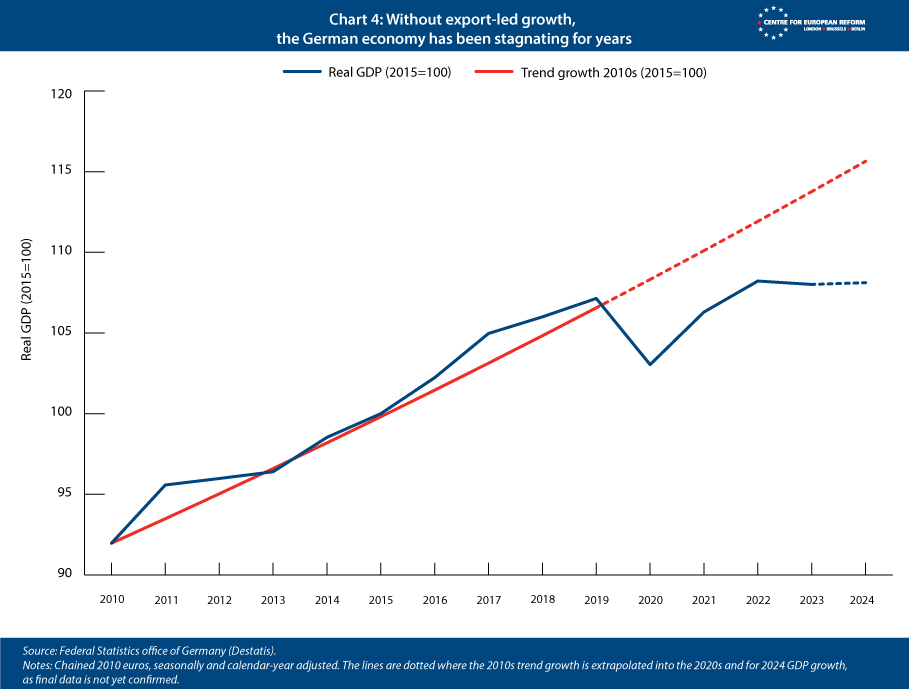

China’s return to export-led growth, with an economy that is a competitive producer of autos and most industrial machinery, and an aspiring producer of aircraft and top-end semiconductors, has put it on a collision course with Germany, the incumbent master of export-led growth. The German economy, meanwhile, has been stagnating for five years – throttled by decades of under-investment, the energy price shock imposed by Vladimir Putin’s war in Ukraine and the ongoing China shock (see Chart 4).20

China’s trade surplus in manufactured goods has jumped by about a half-point of world GDP – and is now far bigger than the combined manufacturing surpluses of Germany and Japan. But in some ways sectoral analysis tells the story more compellingly than the aggregate data.

China’s vehicle exports exceed imports by 5 million, while Germany’s net car exports are half their pre-pandemic peak.

In 2019, China was a net importer of passenger cars – importing about a million, mostly high-end ICE cars (see Chart 5). Those imports were a modest share of China’s roughly 25 million car domestic market but they dwarfed China’s exports. By 2023, only four years later, China was the world’s largest net exporter of cars, with exports in excess of Japan and Germany. As can be seen on Chart 5, it is on track to export about 5 million more passenger cars than it imports in 2024. And by some accounts, China’s production capacity – EVs as well ICEs – approaches 50 million cars.21 That is roughly half of global vehicle demand. Meanwhile, Germany exports one million vehicles a year fewer than it did during the pre-pandemic peak.

China is even more dominant in the production of solar cells (and the assembled panels), EV batteries and their precursor chemicals, and the key components for wind turbines. This capacity has created difficulties inside China – China’s authorities have acknowledged that consolidation will be required to reduce losses in the solar sector. But true capacity reduction remains a challenge, with weaker firms often rescued. For example, Zhido, a bankrupt EV producer, was rescued by equity from the Three Gorges Company (a large state-owned utilities company) and one of China’s provincial governments.22 NIO, another EV producer, also received a bailout.23

German firms are struggling to compete. Bound by the logic of capitalism to deliver returns, not just pour out products, and without profits to fuel new investment, they risk falling behind in the technological race.

The risks of European and German deindustrialisation

The EU, with Germany at its industrial core, boasts 30 million manufacturing jobs: almost twice as many as the US had before the first China shock.24 Not only does the EU have a lot at stake: the potential shock is also much larger this time. China was a $4 trillion dollar economy before the global financial crisis, accounting for less than 15 per cent of global manufacturing output; it is now a $18 trillion economy that accounts for over a third of the world’s manufacturing production.25 In many important sectors, China makes up well over 50 per cent of total global manufacturing capacity.

The EU’s EV tariffs will help to protect European automotive production from Chinese imports, but they are no panacea. Even if the fairly modest tariffs limit China’s share of the EU market, they will not offset the loss of export markets.

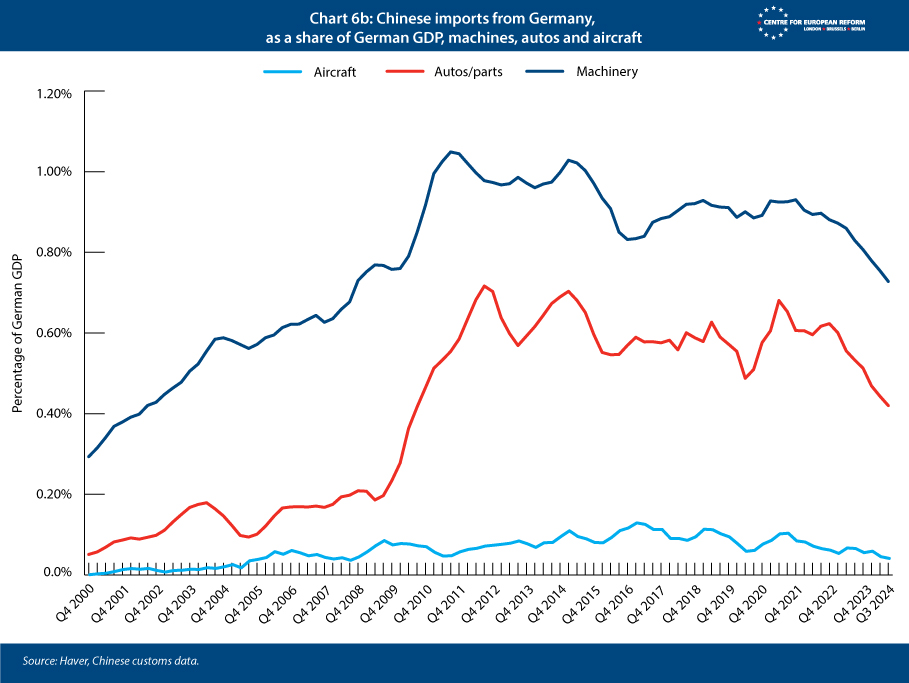

In other words, the second China shock will play out differently from the first because for many economies, including Germany, it will be associated with the loss of export markets, not just a surge in imports. This process is already well underway. As can be seen in Chart 6a, German exports to China as a share of German GDP have been falling for the last two to three years, already representing a loss of approximately 0.5 per cent for the German economy, and there is much more room for decline. The trend in vehicles and machinery is already clear (Chart 6b). Only in aviation is Germany still holding its own, but China has ambitions to expand production of its indigenous narrow-body aircraft.26

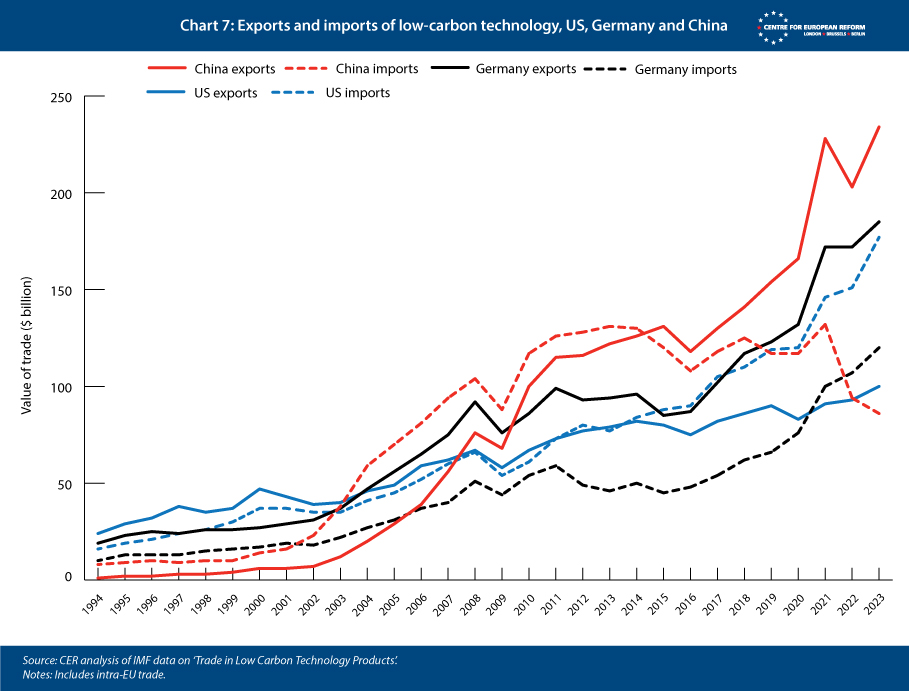

China also appears to be reducing its imports of low-carbon technologies. The IMF maintains a list of more than 200 ‘low-carbon technology’ (LCT) goods, which are defined as technologies that generate lower greenhouse gas emissions over their lifecycles compared with conventional alternatives. This list includes products such as EVs, heat pumps, electrolysers, all kinds of turbines, nuclear centrifuges, as well as everyday technologies like insulation and thermostats. The EU is behind in solar PV and EV batteries. But led by Germany, Europe retains a strong production base in this wider array of clean energy technologies – especially all kinds of machines.27 But while global trade in green tech is rapidly expanding, China is the striking exception here too – curbing imports of low-carbon technologies even as its exports soar (see Chart 7).

The long-term economic damage for Germany will be substantial. Labour and capital are less mobile in Germany than in the US, making shifts in employment across sectors and regions more difficult. Germany’s vaunted furlough schemes (Kurzarbeit) helped the country to manage the cyclical shock of the global financial crisis better than most other large economies. But they are not a solution to the structural decline of entire industries, because they retain the links between workers and employers.

Germany’s exposure here is a result of its past strength in manufacturing, which makes up 19 per cent of German GDP, compared with 11 per cent in the US. Moreover, US domestic manufacturing includes a lot of sectors in which exposure to China is limited, such as food processing. Compare that with Germany: in 2023, exports of cars, machines and chemicals combined accounted for almost 40 per cent of Germany’s total exports, worth 15 per cent of Germany’s GDP.28 And in Germany, as in the US, manufacturing is more productive than services. Letting this sector shrink more than necessary is antithetical to efforts to boost Germany’s languishing productivity growth.

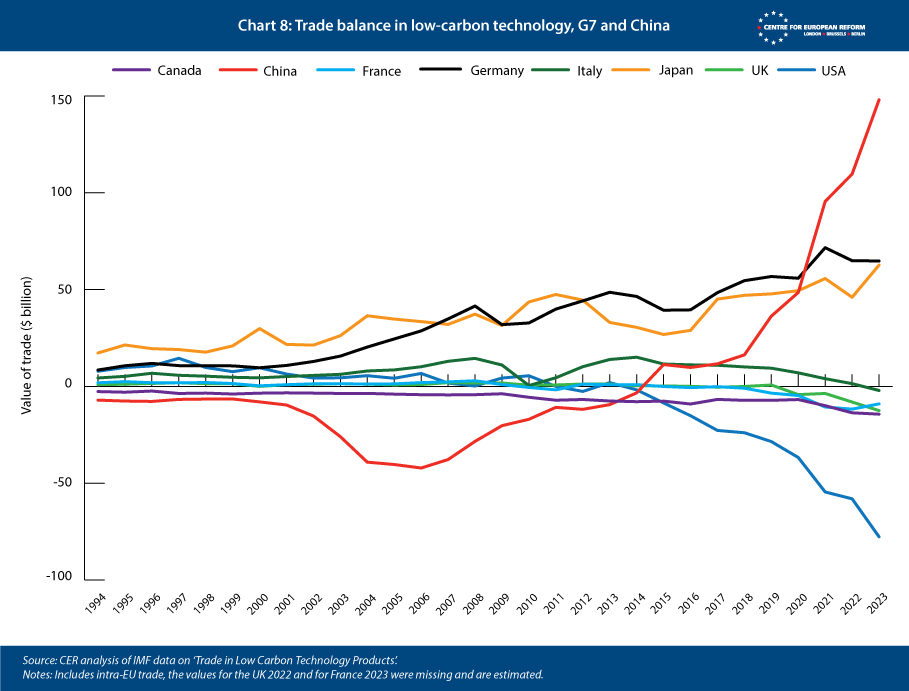

Chinese firms that do not need to show a financial return, thanks to state backing, will also deprive German firms of the profits needed to invest in the next generation of machines and production methods.29 EU cleantech firms now confront massive Chinese overproduction while facing restricted access to the Chinese market, saturated third markets, and import competition. Moreover, firms’ investments typically benefit the broader economy – through workers sharing knowledge of production processes and innovations when moving between employers. Europe now risks losing out on these learning spillovers. This is particularly true for emerging cleantech industries, which may fail to grow enough due to Chinese overproduction – as suggested by an exploding Chinese trade balance in these sectors (Chart 8). Moreover, if China’s policies stifle the contribution to greentech innovation from Germany and the wider EU – one of the leading blocs in patenting – it could also slow the global pace of cleantech development.30

It is possible that China will change course, raise domestic consumption and let its weaker firms fail. The US and EU should hope for such a transformation. But hope is not a plan. The odds are that President Xi Jinping is not going to change what he views as a successful model. The model has severe imbalances and may not be sustainable forever. But China’s state-directed markets could provide irrational levels of financing for new capacity for longer than swathes of German manufacturing can remain solvent.

A German strategy to meet the China challenge

Germany now needs to develop a strategy to counter the global distortions spreading from China’s own unbalanced economy. This strategy should start by recognising that Germany is not alone in its concerns – and that there is a potential global coalition that worries about the economic model adopted by President Xi. Obvious partners include the US and the other G7 members, but also potentially countries like Brazil and Turkey that have voiced concerns and even imposed EV tariffs on China. Germany has at times viewed itself as part of a coalition of trade surplus countries, and thus opposed IMF scrutiny of policies that give rise to large trade surpluses. That should change now. One easy place to start is to insist that the IMF work off solid numbers.

China runs a manufacturing surplus six times that of Germany and reports $1 trillion overall goods surplus in its customs data. But in 2022, China unilaterally changed the methodology that it uses to estimate the goods surplus that it reports in its broader current account – a statistic used by many institutions and analysts around the world. The new number is much smaller and no longer based on the actual customs data. China now counts the production and sales of foreign firms that happen entirely within China as trade deficit with itself. As a result, its official surplus in goods trade is far smaller than actual shipments picked up by the customs data. China also adjusts the value of the exports reported in its customs data down, arguing – without supporting evidence – that the dollar value of exports reported to customs exceeds the actual number of dollars received in payment for these goods.

Solid data is the foundation of solid analysis. There is no reason for the IMF to ignore the well-measured customs surplus simply because China is self-reporting a much smaller number. Germany should also relinquish the past instinct of its economic diplomats and encourage the IMF to push for policies that allow China to grow through domestic household demand, not exports. Germany’s history of support for multilateralism and its position as the EU’s largest economy gives the country global heft.

Deploying trade defence instruments

Second, Germany needs to support a more vigorous set of trade responses to the distortions created by China’s subsidies and wider system of protection. As advocated by former European Central Bank president Mario Draghi, there are sectors that are not strategic, where Europe has little-to-no manufacturing capability and the efficient outcome is to rely on Chinese supply.31

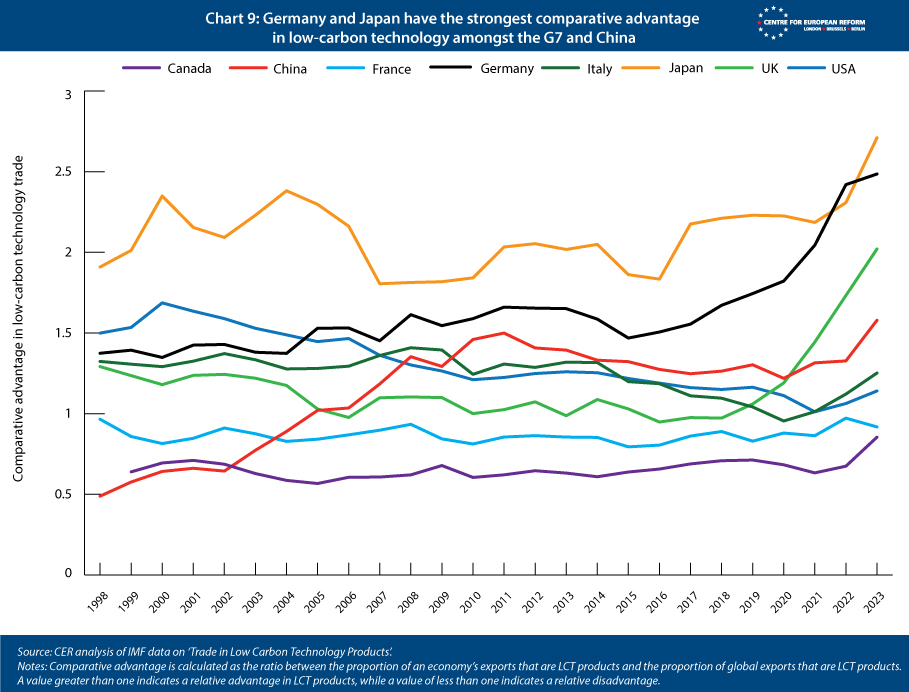

Europe, and especially Germany, is demonstrating that it still maintains a strong comparative advantages in many low-carbon technologies.

But Europe, and especially Germany, is demonstrating that it maintains a strong comparative advantage in many low-carbon technologies (see Chart 9). Europe’s traditional openness to imports needs to be matched by a willingness to deploy its trade defence toolkit to confront difficult cases. China retaliates even when countries follow the rules, but the EU will nevertheless have to offset the advantages created by China’s system of local preferences and its pervasive state subsidies. As the net importer, the EU is also in a strong position, as conflict will tend to hurt the Chinese economy more than the European one.

The European Commission can often impose trade measures, such as tariffs (countervailing duties), in a WTO-compliant way. This is thanks to its investigative work to identify Chinese sectoral subsidies more precisely, and growing understanding that China systematically seeks to promote investment in sectors that can substitute for existing imports. The case against China’s EV subsidies is a useful model.

Ensuring manufacturing demand with buy-European provisions

Third, the EU could introduce buy-European provisions into existing subsidy schemes, such as subsidies to consumers to purchase EVs. China’s WTO commitments have not got in the way of its use of such preferences – no imported car or battery has ever qualified for a Chinese EV subsidy. So, such a measure would be a symmetrical response to China’s own de facto preferences. But the EU might be able to incorporate buy-European mechanisms in a subtle and creative way that does not openly violate WTO rules.

With an EU budget of only around 1 per cent of GDP, and a lack of industrial policy instruments, the Union currently lacks the resources and tools to directly conduct industrial policy in the short run. Industrial subsidies in Europe are primarily decentralised, funded through member-state budgets. And some member-states provide consumer subsidies for EVs or heat pumps with no specific conditions, thereby supporting already heavily subsidised Chinese products. But the EU does have a single market under one regulatory roof, making it easier to co-ordinate subsidies.

The EU could leverage existing single market regulation to integrate de facto buy-European (or ally) clauses into national subsidy schemes. The Net-Zero Industry Act (NZIA), for example, requires authorities to assess how renewable energy auctions for solar or wind farms contribute to sustainability, resilience, cybersecurity, and responsible business conduct. These criteria must apply to least 30 per cent of the volume auctioned annually in each EU country or 6 gigawatts, whichever is greater. The EU could extend that logic to national subsidy schemes for greentech products.

One possible lever to enforce such criteria across the EU would be competition policy: the Commission’s enforcers could condition approval of national subsidy schemes on criteria that favour EU production, such as adherence to social standards, and exclude products associated with high emissions from long-distance transportation or coal-intensive production processes.

France’s EV subsidy scheme incorporates design features that could serve as a blueprint for the EU. The scheme restricts subsidies to low- and middle-income households and ‘green’ vehicles, with eligibility determined by criteria such as the emissions generated during transport from the manufacturing site and whether production relied on coal or cleaner energy sources like those prevalent in the EU. This framework effectively disqualified many Chinese-made EVs, while favouring European-made vehicles that met the criteria. If all EU member-states adopted a similar subsidy, it could have a comparable impact to the local content requirements implemented by Beijing. And the link to environmental, or even national security conditions, could make the European scheme WTO-compliant. While Brussels and Berlin cannot prevent the loss of demand for European goods in China or in third markets saturated by Chinese products, they can ensure that domestic European demand is directed toward EU production.

Brussels and Berlin cannot offset lost Chinese demand but can redirect European demand toward EU production.

The use of the EU’s product-specific regulations provides another lever to shield German manufacturers from competition with China’s subsidised exports, which also benefit from lower environmental and labour standards. Regulations like the European Sustainable Product Regulation (ESPR) can limit market access for non-European competitors failing to meet stringent sustainability criteria. The Commission can implement the ESPR using delegated acts. It could set product standards that combine minimum quotas for low-carbon components – such as green steel or efficient electrolysers – with emissions intensity thresholds. Such thresholds would prevent greenwashing, if they were based on standardised estimates of a product’s carbon emissions, such as the average of an industry in a specific market. Given Europe’s cleaner production processes, such an approach would give EU producers a clear competitive advantage over higher-emission imports from countries like China.

For instance, Chinese-made EV batteries, which often have higher embedded carbon emissions due to coal-heavy electricity grids, would struggle to meet EU standards, creating a competitive advantage for European manufacturers. Subsidy schemes and public procurement rules could then amplify these effects: tax breaks or grants could be tied to the use of components that comply with the EU standards, so that financial support would boost European supply chains rather than funding China’s imports.

These measures could ensure that most, if not all, EU member-states introduce subtle mechanisms in their subsidy schemes to direct European demand toward European production. Member-states have already cut back on some consumer EV subsidies, but insofar as they keep them, or re-instate them, they should tie them to buying European. There may, however, be sectors like non-greentech machine-building or energy-intensive chemical production where existing EU regulations (like the NZIA) or product standards (such as the ESPR) provide insufficient hooks to do so. The EU could then pass new directives to co-ordinate subsidies. Unlike an EU regulation, an EU directive is a legislative act that sets out a goal all member-states must achieve, but allows them to decide how to transpose it into their national laws.

Buy European policies would initially discriminate against countries like the US, which does not have a formal trade agreement with the EU. But there should be scope over time to strike new deals that allow allies and countries that do not discriminate against European products access to European subsidies in return for European access to their own subsidy schemes. In fact, such a deal could provide an elegant solution to European concerns about the discriminatory aspects of the Inflation Reduction Act (IRA), if the incoming Trump administration does not abolish it.

There are, no doubt, other opportunities for increased co-ordination among allies in ways that maintain the advantages of open trade while recognising the challenge that China’s subsidies and unbalanced economy pose to free commerce. Common approaches to carbon tariffs and carbon border adjustment, for example, hold some promise – although to advance in this direction, the EU will have to wait for a US government that recognises the reality of climate change.32

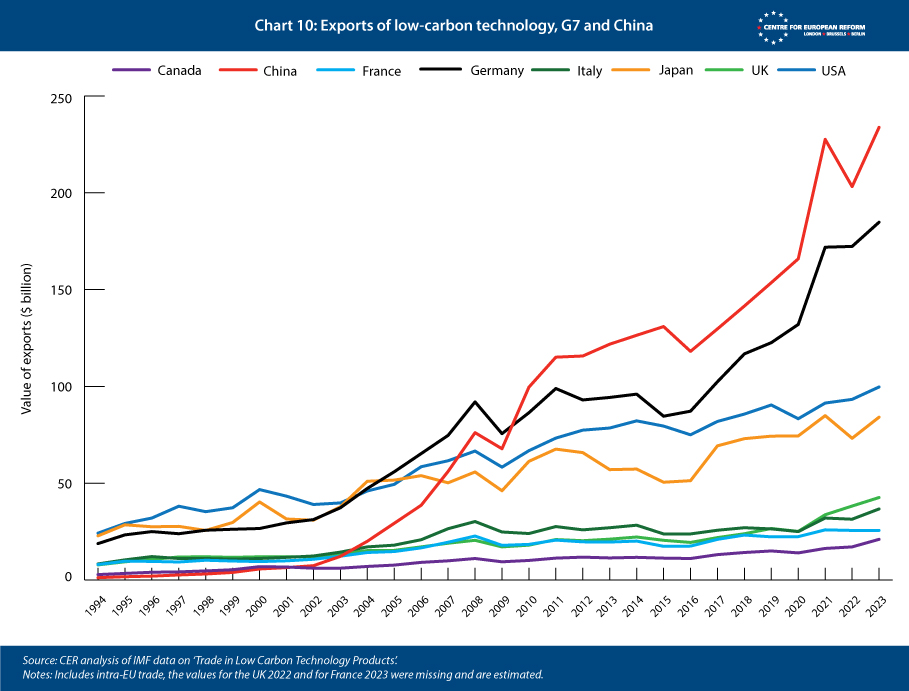

The opportunities for Germany are enormous: it is by value the second largest exporter of low-carbon technologies among the G7 and China already. As allies like the US opt to reduce their reliance on Chinese tech, there will be more demand for German products (see Chart 10). The new Trump administration may roll back US federal climate efforts and slow the expansion of US domestic greentech manufacturing. But renewable energy is increasingly cost-competitive, and US states may still push ahead with greening their economies. This should boost American demand for German cleantech products, as long as the Trump administration does not impose prohibitively high tariffs on European imports.

Funding an EU industrial policy

Fourth, a new German government should take the lead in shaping a coherent European industrial policy. For some time, Europe has had industrial policy at the national level, but member-states often act inconsistently: sometimes allowing companies to fail, at other times intervening; sometimes protecting domestic production with tariffs and standards, and at other times letting global competition – and China’s distortions – dominate. Meanwhile, the EU continues to pile on regulations that often do not align with national policies. The result is an expensive, inefficient patchwork that fails to offer policy and planning certainty. Mario Draghi has called on the EU finally to determine which sectors it wants to preserve and rebuild for strategic purposes, and which it is willing to let fail. These decisions must be followed by concrete measures, including targeted financial support. Germany, as the EU’s industrial heart, would stand to benefit more than most from Draghi’s proposals.

A common fund could facilitate the implementation of an EU-wide industrial policy, mitigating intra-EU subsidy races that distort the single market’s level playing field. It would also prevent scenarios where countries like France and Germany overpay by competing against each other, for example, when trying to attract American or Taiwanese chipmakers to build factories. However, the EU currently lacks the necessary resources: the €800 billion pandemic recovery fund has been allocated, and the EU budget is stretched. Commission President Ursula von der Leyen has repeatedly attempted to establish a fund to support strategic industries across the EU – rebranding it from a ‘sovereignty fund’ to a ‘competitiveness fund’ in its latest iteration. But her efforts have floundered because member-states are unwilling or unable to provide more money or authorise new revenue streams – known as ‘own resources’ – for the Union.

The EU budget is funded by customs revenue, a value added tax-based contribution, a levy on non-recycled plastic packaging, fines imposed after proceedings in the European Court of Justice, and member-states’ contributions based on their relative gross national income (GNI). Since customs income is already an EU own resource, the Union could start funding a common industrial policy by earmarking tariff revenues generated from its trade defence instruments against China. Typically, higher customs revenue would reduce GNI-based contributions from member-states. Because it increases the EU’s own resources, it reduces the amount national coffers need to contribute. However, member-states could choose to redirect tariff income from China – arising from shared trade concerns – towards the long sought-after EU industrial policy fund. Member-state contributions to the EU would not have to increase; they simply would not decrease.

Over time, this could create a substantial revenue stream to (co-)finance large-scale EU industrial policy initiatives. The tariffs on Chinese EVs alone are projected to generate €2-3 billion annually – an amount that will grow as China’s car exports continue to surge. Moreover, the range of products subject to tariffs is set to expand: the EU will impose tariffs on Chinese titanium oxide next year, has initiated anti-subsidy investigations into Chinese train and wind turbine imports, and has raised concerns about electrolysers.

Conclusion

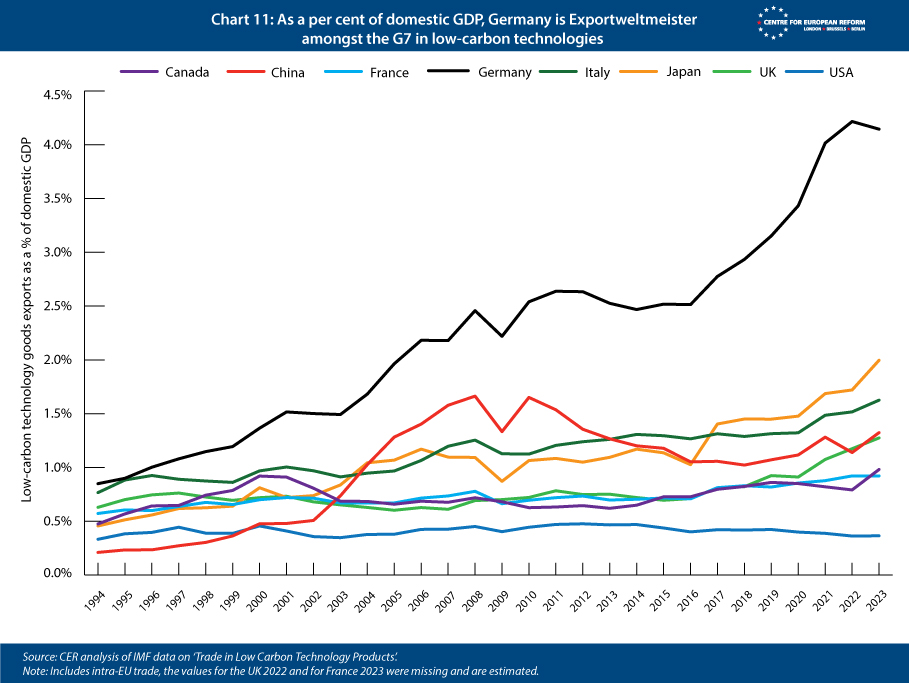

For the moment, Europe, led by Germany, retains a strong production base in cars, machinery and aviation. Germany is also the second largest exporter of greentech products behind China; in terms of exports as a share of GDP, Germany is even the leader (see Chart 11). But Europe cannot be complacent: if it does not act to counter Chinese policies, its current advantages in other sectors will go the same way as those in EV batteries and solar panels.

EU industrial policy support would undoubtedly benefit Germany, and it should. And unlike its budget transfers to poorer regions or farmers, the EU should target its scarce industrial policy funds to maximise European competitiveness. This means supporting value chains (and regions) with strong potential, many of which are centred in Germany. Germany would be a primary beneficiary of a significant European funding programme for decarbonising industry or expanding chip production, for example.

Berlin frets that a more muscular EU industrial and trade policy would lead to Chinese retaliation against German multinationals operating in China. But a new German government should not equate the interests of German businesses operating in China with the interests of the German economy. What is good for Volkswagen is no longer always what is good for Germany. It would not be in Germany’s long-term interest, for example, if German firms turned China into their hub for the design and production of all luxury EVs, eroding the technical skill set and advanced quality production of cars that has long been the mark of the German economy. For German workers the trade-offs are stark and real; German firms that succeed by moving production of cutting-edge technologies out of Germany ultimately weaken, rather than strengthen, the German economy.

Finally, Germany needs to recognize that it will also need to do a better job of identifying domestic drivers of growth, and not starve its own economy of needed investment. Even if Europe tightens trade policies, China’s massive overproduction will still make exporting to third countries more difficult. Without steps to boost domestic consumption and investment, Germany will not be able both to absorb China’s surplus production and provide demand for its own manufacturing. Cutting EV subsidies to comply with its constitutional debt brake is self-defeating, and deprives Berlin of instruments to steer demand in support of its own manufacturing.

Germany is more exposed to the current China shock than many other Western countries because of its industrial structure and China’s growing exports of advanced manufactured goods. The country also has more fiscal scope to counter the China shock than most other advanced economies. Berlin must weigh deploying some of its ample fiscal space against the looming threat of deindustrialisation. It may come down to use it or lose it. Millions of manufacturing jobs, the communities they sustain, and Germany’s future as a cleantech manufacturing powerhouse are at stake.

2: Monica Raymunt and Christoph Rauwald, ‘VW weighs first-ever Germany plant closures to cut costs’, Bloomberg, September 2nd 2024.

3: Brad Setser, ‘The surprising resilience of globalisation: An examination of claims of economic fragmentation’, Aspen Institute, October 2024.

4: Aslak Berg and Zach Meyers, ‘Surviving Trump 2.0: What does the US election mean for Europe’s economy?’, CER policy brief, October 2024.

5: David Autor, David Dorn and Gordon Hanson, ‘On the persistence of the China shock’, NBER Working Paper, October 2021.

6: ‘China’s manufacturers are going broke’, The Economist, August 8th 2024.

7: Daniel Ren, ‘China’s EV makers are selling more vehicles at bigger losses, as price war takes its toll’, South China Morning Post, August 23rd 2024.

8: Keith Bradsher, ‘It is desolate: China’s glut of unused car factories’, The New York Times, April 23rd 2024.

9: Incidentally, the reverse is true for the United States: the EU exports a lot of EVs to America (and parts to the German car plants in Mexico that now make EVs) while importing almost no US-made EVs.

10: Finbarr Bermingham, ‘EU votes for tariffs on Chinese-made EVs in blockbuster trade row’, South China Morning Post, October 4th 2024.

11: Peter Dizikes, ‘Q&A: David Autor on the long afterlife of the “China shock”’, MIT News, December 6th 2021.

12: Hedieh Aghelmaleki, Ronald Bachmann and Joel Stiebale, ‘The China shock, employment protection and European jobs’, DICE Discussion Paper, December 2019.

13: Frank Bickenbach, Dirk Dohse, Rolf Langhammer and Wan-Hsin Liu, ‘EU concerns about Chinese subsidies: What the evidence suggests’, Intereconomics – Review of European Economic Policy, August 2024; Jost Wübbeke, Mirjam Meissner, Max Zenglein, Jaqueline Ives and Björn Conrad, ‘Made in China 2025: The making of a high-tech superpower and consequences for industrial countries’, Mercator Institute for China Studies, December 2016.

14: World Bank, ‘Households and NPIHSHs final consumption expenditure (per cent of GDP) – European Union, United States’, World Bank open data.

15: Zhang Jun, ‘Why is China’s consumption rate so low?’, Project Syndicate, July 2024 and Michael Pettis, ‘China must sacrifice GDP growth to rebalance its economy’, South China Morning Post, October 3rd 2022.

16: Henry Hoyle and Sonali Jain-Chandra, ‘China’s real estate sector: Managing the medium-term slowdown’, International Monetary Fund, February 2024.

17: Brad Setser and Michael Weilandt, ‘China’s stunning 2024 export growth’, Council on Foreign Relations, December 2024.

18: Brad Setser, Michael Weilandt and Volkmar Bauer, ‘China’s Record Manufacturing Surplus’, Council on Foreign Relations, March 2024.

19: Keith Bradsher, ‘China’s trade surplus reaches record of nearly $1 trillion’, The New York Times, January 13th 2025.

20: Tom Nuttall, ‘Once dominant, Germany is now desperate’, The Economist, November 20th 2024.

21: Agnes Chang and Keith Bradsher, ‘How China became the world’s largest car exporter’, The New York Times, November 29th 2024.

22: Yoko Kubota and Clarence Leong, ‘Why China keeps making more cars than it needs’, The Wall Street Journal, April 28th 2023.

23: Craig Trudell, ‘NIO soars on China government deal; Bernstein calls it a bailout’, Bloomberg, February 25th 2020.

24: Eurostat, ‘Manufacturing statistics – NACE Rev. 2’, European Commission, 2024 and Federal Reserve Bank of St Louis, ‘All employees: Manufacturing (MANEMP)’, 2024.

25: David Autor, David Dorn and Gordon Hanson, ‘The China shock: Learning from labor-market adjustment to large changes in trade’, Annual Review of Economics, October 2016; Richard Baldwin, ‘China is the world’s sole manufacturing superpower: A line sketch of the rise’, Centre for Economic Policy Research, January 2024.

26: Alexander Brown, Jacob Gunter and Max Zenglein, ‘Course correction: China’s shifting approach to economic globalisation’, Mercator Institute for China Studies, October 2021.

27: John Springford and Sander Tordoir, ‘Europe can withstand American and Chinese subsidies for greentech’, CER policy brief, June 2023.

28: Federal Statistical Office of Germany (Destatis), ‘Trading Goods’, 2024.

29: Philippe Aghion, Reda Cherif and Fuad Hasanov, ‘Competition, innovation, and inclusive growth’, IMF Working Paper, March 2021.

30: Sander Tordoir, ‘Chinese exports threaten Europe even more than the US’, Politico, June 7th 2024.

31: Mario Draghi, ‘The future of EU competitiveness’, European Commission, September 2024.

32: Elisabetta Cornago and Aslak Berg, ‘Learning from CBAM’s transitional phase: Early impacts on trade and climate efforts’, CER policy brief, December 2024.

Sander Tordoir is the chief economist at the Centre for European Reform and Brad Setser is the Whitney Shepardson senior fellow at the Council on Foreign Relations

Related content