A reform agenda for the single market

- The EU needs faster growth. Productivity has stalled, energy prices remain high, and the bloc’s biggest economic asset – the single market – is incomplete. With the US and China both intervening in trade, protecting demand, and investing heavily in industrial capacity and innovation, the EU risks falling further behind. Europe cannot afford another decade of drift.

- This paper sets out a reform agenda that can deliver growth within today’s political constraints. It builds on the recent reports by former Italian prime minister Enrico Letta and former ECB president Mario Draghi, but focuses on reforms that member-states are more likely to agree to – and which could start delivering results within this legislative cycle. The EU should prioritise four areas:

- Smart regulation: Too much recent EU regulation has prioritised political signalling while there has been too little attention given to the potential impacts of poorly designed regulation on economic growth. The Commission should refocus regulation on deepening the single market, not pre-emptively harmonising emerging sectors or acting as the world’s first mover. That means:

- Cutting overlap and inconsistencies – especially in digital regulation – through a coherent ‘omnibus’ clean-up.

- Reasserting the subsidiarity principle to allow regulatory experimentation between member-states – to help identify the most efficient way to regulate – and avoid locking in bad rules.

- Using self- and co-regulation more often to give firms flexibility in meeting policy goals, especially when trying to reconcile prescriptive rules like the bloc’s data protection laws with the deployment of new technologies like AI.

- Taking a tougher line on member-states that fragment the single market by gold-plating or misapplying EU law.

- Energy market integration: Europe’s power market is still too fragmented. Grid bottlenecks and poor co-ordination are keeping prices higher than necessary. To fix this:

- Invest in cross-border grid connections and prioritise EU-level co-ordination of infrastructure spending.

- Shift to smaller bidding zones and more granular pricing to reflect local costs and reduce congestion.

- Mainstream time-varying power pricing and accelerate the deployment of smart meters to encourage consumption at times when prices are low.

- A Savings and Investment Union: A lot can be done to expedite capital market growth at member-state level. The EU should embrace the ‘bottom-up’ approach to capital markets by taking on a greater role in co-ordinating and incentivising successful national policies that drive financial development:

- The EU should push ahead with the 28th legal regime (which allows companies to opt in to a single European legal regime) to help companies increase scale across borders.

- Many obstacles to capital market deepening are national. The EU should play a stronger role in benchmarking member-states on the extent to which they encourage financial market growth as part of the European Semester.

- The EU should incentivise reforms by showing some flexibility on financial targets to countries that undergo meaningful capital market reform.

- Services and city-led growth: The next phase of the single market must focus on services. Intra-EU services trade is growing fast, but it is concentrated in a few large cities. Without reform, integration will widen regional divides. The EU should:

- Encourage development of trade in services through supporting a group of ‘European growth city-regions’ that have the potential to become hubs for services trade, with investment in infrastructure, energy, transport.

- Empower cities by giving them increased say in how EU funds are spent in their areas.

- Shift funding away from lower-impact spending and towards human capital and infrastructure.

- A more innovation-friendly approach to competition policy should not come at the expense of market integration and should protect the foundations of EU competition law, which have served the bloc well. The Commission should:

- Discourage political interference which would block or dissuade firms from pro-competitive intra-EU mergers. This has been a particular problem in sectors like banking where there remains a strong desire in some capitals to protect ‘national champions’.

- Revise its guidelines to reflect the importance of scale, the prospects for radical innovation in some sectors, and the nature of global competition. However, these guidelines should not ignore reality. The EU cannot be ‘assumed’ to be a single market in cases where regulatory barriers and divergences mean that firms only compete with their domestic competitors, for example.

- The Commission should consider making it easier for firms to argue that their merger will have positive effects on consumers through greater innovation. However, the Commission must still assess these claims critically. Scale matters more to innovation in high-tech digital markets, rather than in infrastructure-heavy sectors like telecoms where incumbents have been lobbying heavily for a relaxed approach. The Commission must still ensure that changes to merger policy do not allow mergers (such as many in-country telecoms mergers) that raise prices while providing questionable benefits for investment and innovation.

The European Union has a growth problem. Its share of the global economy has been on a steady decline for decades, dropping from over 20 per cent in 2000 to around 15 per cent currently. In part, this is due to catch-up growth in developing countries but the EU has also lagged behind its peer across the Atlantic, the United States. Europe’s productivity growth, rate of innovation and ability to foster new, innovative companies all compare unfavourably with the US.

At the same time, the EU is operating in an increasingly difficult external environment. Russian aggression has led to increased energy prices as well the need for increased defence spending, putting strain on public purses that were already under pressure from high debt levels, mediocre productivity growth and higher health and pension spending as populations age. Meanwhile, the US has turned increasingly protectionist and has broken with WTO rules, forcing the EU to accept higher tariffs. China, on the other hand, has been an aggressive competitor, putting increasing price pressure on European products, both in the European domestic market and export markets.

The first step towards solving a problem is acknowledging its existence. In that respect, Europe has done well, with not one, but two major reports coming out last year by former Italian prime ministers Enrico Letta and Mario Draghi. These reports do a good job laying out the productivity challenge and the various ways the EU can address them. However, many of their proposals are politically very ambitious, and face resistance from member-states that are loath to give up additional powers to the EU. For instance, the banking and capital market unions are long-standing projects that would provide obvious benefits for the EU but have made little headway against national opposition. Similarly, the issuance of EU bonds has been limited to exceptional circumstances such as the pandemic, and although European financial markets would clearly benefit from an EU-level safe asset, there is little chance of this happening in the near future.

This paper provides a reform agenda that would boost economic growth while also being politically feasible within current political constraints. By focusing on a few key issues – better regulation, energy, a savings and investment union, and the single market for services – we hope to provide a trigger for practical action that would leave Europe better able to foster the growth it needs.

Better regulation

For decades, EU leaders have promised to improve law-making processes. These promises typically aim to ensure that regulations are evidence-based, made transparently, consulted on, and are as simple and targeted as possible. These are all important ways to ensure regulations have clearly defined goals and deliver those goals effectively and efficiently.

EU regulation’s purpose – to cut internal barriers reducing productivity – has often been relegated for other priorities.

However, there is a growing gap between rhetoric and process on the one hand, and outcomes on the other. Over the years, the EU has bolstered institutions like the European Court of Auditors and the Regulatory Scrutiny Board, strengthened its commitment to consultation and impact assessment, and instituted practices like the ‘one in, one out’ (the idea that for every new burden a legislative proposal adds, the Commission should seek to remove another) to help avoid an ever-growing set of rules. While the von der Leyen Commission has reinforced many of these ‘better regulation’ initiatives, there has been a growing consensus that the quantity of EU regulation has vastly increased in recent years while its quality has significantly declined.

One of the main problems has been that the primary purpose of EU-level regulation – to strengthen the single market and cut internal barriers that reduce productivity – has often been relegated in favour of other political priorities. These include establishing the EU as the ‘first mover’ globally and mitigating the risks of new technologies. For example, law-makers loudly proclaimed as a success that the EU was the first jurisdiction to comprehensively regulate artificial intelligence (AI) before the market truly developed.

As a consequence, new EU laws are less focused on reducing existing barriers to cross-border business. Instead, they are more frequently passed to pre-empt possible future regulatory fragmentation – such as in the area of digital competition or artificial intelligence – or to enact new political priorities such as in the area of economic security. This has sometimes had the effect of extending EU laws into areas which were previously unregulated, such as providing detailed rules about online safety. This extension of the EU’s competences has coincided with the European Commission becoming more powerful and politicised – contrary to its originally conceived role as a more technocratic body which would be freer than member-state governments and MEPs and could avoid short-termism and lobbying to make disinterested, long-term decisions.

In recognition of growing government and business concerns, the Commission is currently undertaking a simplification exercise aimed at cutting reporting obligations and streamlining some regulations. However, the Commission has so far insisted that the fundamental principles of those EU regulations are not up for debate in this exercise.

Improving existing stock of European regulation will be important, but there are strongly held views about whether the EU’s approach to regulation is too risk-averse and precautionary. It seems unlikely at this stage that there will be political consensus for any significant dilution of the EU’s regulatory standards. Nor is merely cutting red tape – while potentially helpful in reducing business overheads – likely to meaningfully boost economic growth. However, the European Commission should urgently adopt a rationalisation exercise, which would seek to simplify and address inconsistencies between different laws. This will be particularly important in the digital sector where more than 100 laws have been passed in recent years, often with significant and complex overlaps. For example, the same cybersecurity incident may need to be reported under a number of different laws, such as the Network and Information Systems Directive (NIS 2), the Digital Operational Resilience Act (DORA), the Cyber Resilience Act (CRA), and the General Data Protection Regulation (GDPR), often under different timelines and with different information required. This unnecessarily ties up resources for firms which should instead be focused on mitigating the impact of an incident. The EU’s upcoming ‘omnibus’ proposals should aim to deliver a single, coherent and easy-to-follow set of EU-wide rules in areas such as this.

The EU must also address the institutional incentives that have contributed to the recent ‘tsunami’ of new laws, in order to ensure that future proposals are better designed and fulfil the ultimate goal of deepening the single market. To do this the EU should:

- Return to and rigorously insist on the importance of ‘subsidiarity’. The idea that the EU should only regulate where doing so adds value. The Commission needs to recognise that EU-level law-making is a double-edged sword. On the one hand, it can reduce barriers to entry. But it can also reduce diversity and regulatory experimentation among member-states, locking in regulation which may be suboptimal. This is a particular risk where an EU priority is to regulate quickly – in order to pre-empt possible future regulatory fragmentation – rather than carefully. Artificial intelligence may have been one area where there may have been more benefit in waiting to better identify the risks AI regulation should target, and the possible models for regulation, before locking down one model for the whole EU.

- Adopt regulatory approaches that provide opportunities for self-regulation and co-regulation. Self-regulation and co-regulation involve setting policy objectives but giving firms discretion to work out how to deliver those objectives, often by working together and setting industry standards – and with input from regulators. In many policy areas, these approaches can frequently be more effective, efficient and innovation-friendly than traditional prescriptive regulation because they provide firms with flexibility, an ability to find the most cost-effective way to comply with regulation, and more freedom to experiment with new technologies and business practices. Prescriptive rules can then be a back-up if industry does not deliver. There is significant opportunity to increase the role of self-regulation and co-regulation in areas like data protection. While the principles underpinning laws like the GDPR remain sound, a more flexible approach to implementing these principles is necessary to adapt to technologies like AI. Given how fast-moving this sector is, close industry/regulator engagement and a more adaptable approach to GDPR implementation will be essential.

- Adopt regulatory approaches which encourage and allow healthy regulatory competition between member-states. Where there is a need to lower barriers to cross-border business, applying a single set of rules for all companies operating in Europe is not the only solution – and often it will be suboptimal. For example, the concept of ‘mutual recognition’ and ‘country of origin’ can allow different member-states and their local authorities to set their own regulations, with compliance in one member-state allowing a company to operate across the whole of the EU, and the EU setting only the overall standards that national approaches must ensure. This type of approach allows regulatory experimentation: with many firms able to choose the regulatory approach which best suits their business, without compromising on minimum standards.

- Encourage the Commission to enforce single market rules. Many member-states have a poor record of faithfully transposing EU directives into national law. The Commission previously initiated proceedings against those member-states, but only 529 new cases were opened in 2023, the lowest in the last ten years.1 The Commission has become less willing to ‘pick fights’ with member-states over time – preferring a dialogue-based approach, without much evidence that this has achieved results.

- Encourage the Commission to resist legislative amendments that undermine the single market. EU law-making is often characterised by horse-trading, where individual member-states are granted ‘opt-outs’ or are free to ‘gold-plate’ laws. In recent years, the Commission has been unwilling to let legal proposals fail even when member-states insist on concessions that put the value of the law in doubt.

Energy

Through the Energy Union, the EU aims to ensure secure, sustainable, competitive, and affordable energy for all EU citizens and businesses. The EU energy market today is better integrated than twenty years ago, but many barriers are still in place, preventing it from delivering energy across the EU more efficiently and at more affordable prices.2 In the era of electrification, integrating the electricity markets of all EU member-states is a way to strengthen energy security, reduce carbon emissions and ultimately drive down energy prices. But a series of barriers – related to infrastructure, policy and market developments – are holding back market integration in the energy sphere.

Infrastructure barriers: Grids and interconnections

In the power sector, interconnecting national electricity markets through cable infrastructure (and, administratively, through trading agreements) ensures that the cheapest generation feeds demand across the EU first. This also limits the need to call upon more expensive (and generally fossil-fuelled) generation when electricity demand is high. Interconnecting power markets functions as an important safety net, as demonstrated during the 2022-2023 energy crisis, and contributes to keeping the average electricity price across the EU lower than if national power markets were walled off. Europe today does not have sufficient cross-border infrastructure to enable truly integrated energy markets.

Connecting different regional energy markets contributes to more efficiently dispatching energy supply wherever it is demanded.

Additionally, before 2022 most natural gas entered the EU via pipelines from Russia and then made its way towards western member-states. Shifting away from pipeline imports to LNG deliveries via sea has required larger gas quantities to be transported from west to east. This has caused congestion on the gas grid, driving up prices. And because it must be cooled to be transported by ship and then regasified, LNG is costlier to transport than pipeline gas, which has further contributed to increasing average natural gas prices in Europe. Higher gas prices have led to higher electricity prices too, given that gas power plants are frequently the supplier of last resort at peak time.

Policy barriers: National sovereignty on energy policy

The reason why interconnections among different EU countries are not always sufficiently large or sufficiently exploited relates to a major policy barrier to energy market integration: energy policy is a remit of national governments, which leads to very different energy mixes across the EU. It is designed to optimise for national interest as opposed to collective European interest, which causes several market distortions.

First, governments can be subject to political pressure to protect their own energy generators from lower-cost competitors in neighbouring countries by limiting trade in electricity. This could happen through insufficient investment in interconnections, or through regulatory barriers preventing the efficient exploitation of existing interconnectors, which both limit the benefits from trade. In these contexts, compensation of the ‘losing’ parties could help unlock higher cross-country trade.3

Second, if investment decisions for new infrastructure are taken with a national perspective, as opposed to co-ordinating them at EU level, they could result in inefficiencies, such as costlier undertakings. In the power sector, this leads to overinvestment in generation capacity and underinvestment in grid connections to neighbouring countries. This results in inefficient use of existing power generation capacity, which leads to higher average prices.

Market design barriers

Connecting different regional energy markets contributes to more efficiently dispatching energy supply wherever it is demanded, keeping prices lower. Efficient dispatch requires transparent electricity prices that reflect the cost of power generation as it varies across energy sources: for example, because renewables are cheaper energy sources for electricity generation than natural gas or coal, regions with high renewable power generation tend to experience lower average electricity prices compared with regions largely relying on fossil-fuelled generation.

Another factor shaping electricity prices is the design of bidding zones, which are the geographical areas in which electricity trades happen without cross-zonal agreements (because there is no need to attribute cross-zonal capacity).4 By and large, in Europe bidding zones coincide with national borders, but few countries, such as Italy and Sweden, are split into multiple bidding zones, leading to price variation across the country.

The size of bidding zones matters for power prices: smaller bidding zones deliver more granular electricity price signals that better reflect generation costs, along with the costs of managing distribution, transmission and congestion on the grid. Conversely, arbitrarily large price zones can lead to higher average prices by hiding all these factors. A review of bidding zones in Europe is ongoing to assess network congestion issues across borders and verify whether alternative configurations of bidding zones could reduce them and increase efficiency.5

How do these barriers affect the EU electricity market, and how to remove them?

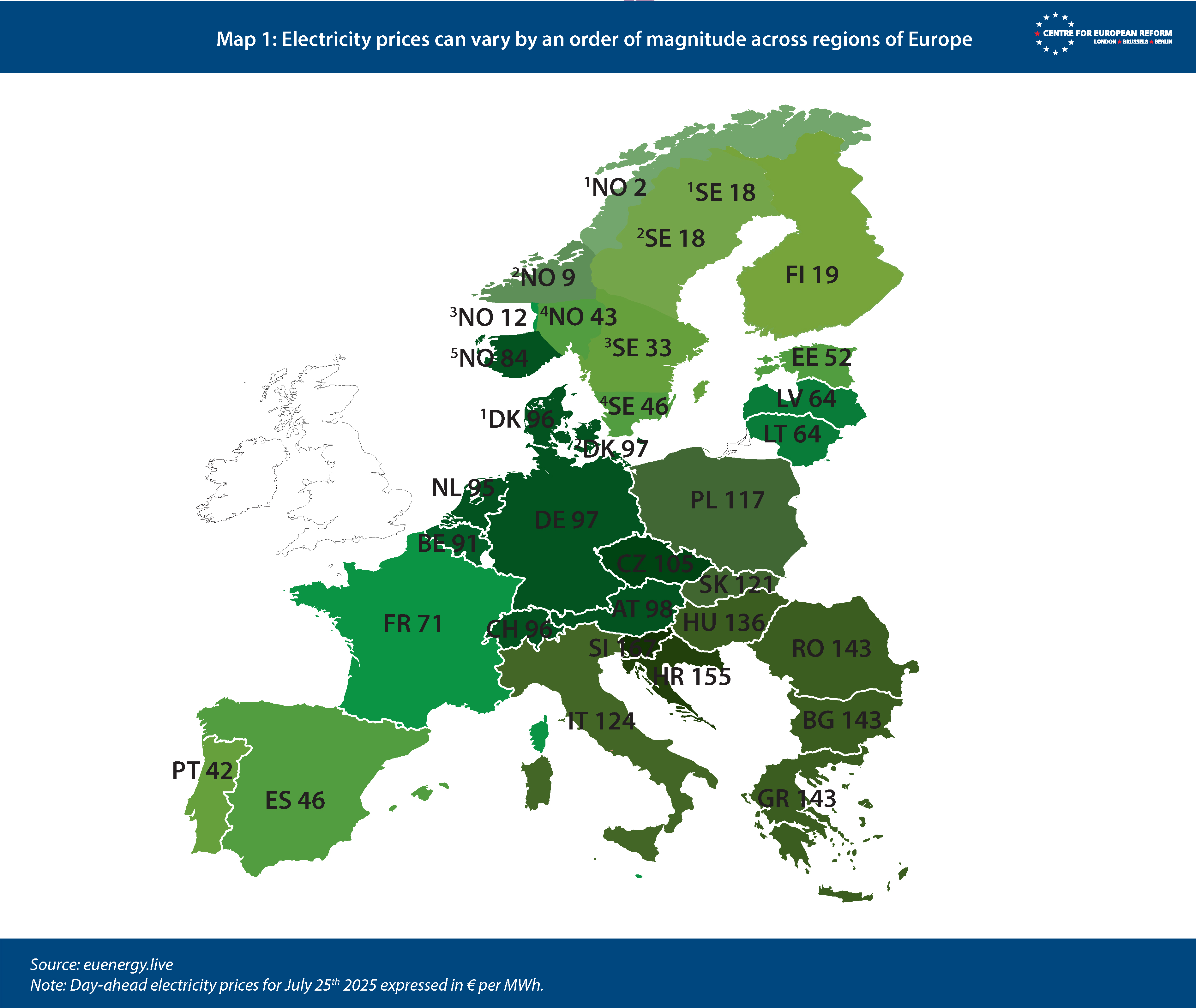

The welfare benefits for consumers of a fully interconnected EU electricity market amount to about €34 billion per year, as estimated by ACER.6 So the barriers above are leading to large welfare losses for European consumers, as a result of higher electricity prices.

Additionally, as Map 1 shows, prices are heterogeneous across the EU, with minimum levels frequently observed in areas where renewable energy penetration is high and interconnections to other markets ample (eg Northern Sweden), whereas poorly connected regions with high dependence on gas experience price spikes (eg Greece, Bulgaria). These prices reflect the mismatch between the location of power supply and demand, and scarce transmission lines, a combination of factors which leads to congestion in the power system. Abundant renewable energy capacity can also contribute to congestion, as it is not possible to modulate generation, as with thermal power plants.

Handling congestion in power systems is costly: in 2023, the cost of congestion management amounted to €4 billion in the EU, of which 60 per cent was in Germany, which notoriously has a single bidding zone, despite large energy market variations within the country.7 Concretely, to address congestion costs, transmission system operators (TSOs) require power generators to adjust their production to balance supply and demand, in a process called ‘re-dispatching’. If generation exceeds demand with limited possibilities to export it, renewable energy generators may be ‘curtailed’ or temporarily shut down to relieve pressure from the power system.8

These are short-term solutions: moving towards a power system that is largely reliant on renewables clashes with practices such as curtailing. Supporting the installation of batteries for energy storage, both at small and large scale, can absorb extra generation from renewables at times of low electricity demand, and reduce the need to fire up fossil-fuelled plants at times of high demand. Renewable energy investment should be encouraged with incentives with locational criteria, so to better reward investments closer to demand centres. More broadly, investments in new generation and in grid expansions should be better co-ordinated across member-states, in order to reduce their overall costs by better connecting supply and demand across borders. More granular pricing, conveyed through smaller bidding zones can help send more effective price signals in this sense.

But while congestion can be addressed on the supply side, electricity demand can also be adjusted to ease congestion and reduce the overall cost of power system functioning. Consumers can be rewarded for reducing their power demand at peak times, shifting some activities to off-peak moments – when renewable energy might be more abundant and electricity cheaper. Some appliances can also be used to enhance the flexibility of the electricity system, such as electric vehicles, which are ultimately power batteries on wheels. Fully exploiting the potential of flexible and responsive electricity demand requires two changes: the roll-out of smart meters, which can measure power consumption on a granular time scale, and the mainstreaming of time-varying power pricing, so that electricity retailers can incentivise consumers to shift their consumption off-peak through lower prices.

In sum, Europe’s power market is still too fragmented. Grid bottlenecks and poor co-ordination are keeping prices higher than necessary. To fix this, the EU should:

- Encourage a fuller exploitation of existing cross-border interconnections, to optimise existing power supply. It should also support investment in new cross-border grid connections: in this sense, the proposed MFF is going in the right direction. Grid planning and spending should be co-ordinated at EU level, to minimise overall system costs.

- Shift to smaller bidding zones and more granular pricing to better reflect generation, transmission and distribution costs, and reduce congestion.

- Encourage flexible power demand, to reduce fossil-fuelled power generation. To achieve this, accelerate the deployment of smart meters and battery storage, and the uptake of time-varying power pricing to incentivise consumption when prices are low.

A Savings and Investment Union for growth

Investment fuels growth. As Europe seeks to boost its flagging growth rate, the focus therefore naturally shifts to boosting investment to help increase productivity. There is certainly no lack of savings in Europe – as the Draghi report points out, the EU has a high household savings rate that could easily fund the investment needed. In the aggregate, European savings are 65 per cent higher than in the US. However, European households invest conservatively, with a large percentage locked into relatively low-yield bank deposits. As a result, household wealth is higher in the US and fewer European savings are channelled into higher yield investments. And European companies are excessively reliant on bank loans, which made up more than three-quarters of corporate borrowing in 2022. In comparison, the US corporate bond market is worth over $11 trillion, compared to $2.8 trillion commercial and industrial loans in commercial banks.9

Sweden, Denmark and the Netherlands account for over 60 per cent of European pension assets through market-based savings.

This 'bank bias' limits the development of European capital markets. The EU’s share of global capital markets activity declined from 18 to 10 per cent between 2010 and 2022. Meanwhile, venture capital funding as a share of GDP is only 0.3 per cent, compared to 1.1 per cent in the US.10 The result is that European entrepreneurs and business simply do not have the same access to risk capital as peers in the US. Without that vital lifeline of risk-seeking capital, today’s tech giants would not have been able to grow and achieve their current scale.

European capital markets are, in general, shallow, illiquid and underdeveloped compared to the US. European financial markets are on the one hand fragmented by member-state, each with its own set of regulations, tax laws and supervisory authority. On the other hand, even considering their state of fragmentation, European markets are smaller than they should be.

There is both a top-down and bottom-up approach to address this. No European market is able to achieve the size and liquidity of US markets without further integration and European regulation – a top-down approach. Pensions systems, capital taxation, financial education and the broader incentive structures that citizens face are still largely a result of national regulation. This means that there is a lot that could be done at a member-state level to encourage growth in European capital markets. As a specific example, Sweden, Denmark and the Netherlands contribute more than 60 per cent of European pension assets due to their encouragement of pension savings in capital markets. As a result of this and other finance-friendly rules these countries also have more developed financial markets. This is the so-called bottom-up approach, and the European Union could take on a greater role in co-ordinating and incentivising policy that encourages capital market growth.

The EU has long tried to create a Capital Markets Union, now rebaptised the Savings and Investment Union. So far, the results have been meagre in the face of member-state reluctance to cede national regulatory powers. There is a European personal pension product, PEPP, that has seen little uptake so far, largely because it is not guaranteed favourable tax treatment and has to compete with similar national products. There is some consolidation in the ownership of market exchanges with the rise of groups like Euronext that owns equity markets in several European countries – but from a regulatory perspective these are still run as a collection of separate markets instead of a single integrated one.

The EU should resist a purely top-down approach, since many barriers to capital-market deepening are national.

Some priorities can only be achieved with a top-down approach. The new framework for securitisation proposed by the Commission will reduce regulatory complexity and encourage securitisation by reducing the risk weight assigned to securitised assets, allowing financial institutions to own more of them. The so-called 28th regime, due to be proposed next year, would allow companies to opt into a single European corporate legal regime instead of dealing with multiple regimes. Both of these efforts would be significant steps in the right direction and should be encouraged. In particular, the 28th regime would allow companies to grow cross-border quickly while attracting investors that would no longer have to deal with a range of unfamiliar legal regimes. If successful, this would then also encourage a more unified financial ecosystem for financing start-ups and growth companies.

However, the European Union should resist only focusing on top-down approaches. Because many obstacles to capital-market deepening are national, it needs to find a way to encourage member-states to do what they can to develop their financial markets. The EU should play a stronger role in benchmarking member-states on the extent to which they encourage financial market growth as part of the European Semester – the bloc’s internal economic policy co-ordination system. A scoring system based on factors such as tax incentives, mandatory private pension savings plans, and consolidation of pension assets would help provide transparency.

The EU could incentivise reforms by showing greater leniency on fiscal targets to countries undergoing meaningful capital market reform. More ambitiously, it could copy some ideas from the Green Deal and propose binding targets for member-states while giving them flexibility in how to reach those targets. In either case, the goal should be to encourage financial activity: increasing private pension saving, the level of securitisation, the share of corporate borrowing done through markets instead of bank loans, the number of IPOs and the share of venture capital funding. Given the significant national resistance to harmonisation in some member-states, the EU should also encourage coalitions of the willing: some countries might be willing to merge national regulators to provide truly integrated equity and capital markets at a regional level.

The Savings and Investment Union project is essential to deliver on the EU’s agenda: economic growth, climate investment, defence spending all depend on it. Even an ambitious approach must recognise that much of the heavy lifting must happen at the member-state level, but within a European framework that encourages and rewards reform, while facilitating harmonisation where possible. To progress, the EU should:

- Encourage bottom-up reform at the member-state level by enabling a scoring system for reform as part of the European Semester and rewarding reform that encourages financial activity, for example through greater leniency on fiscal targets.

- Propose binding targets for financial activity whilst leaving the precise mechanism up to member-states. Possible targets include private pension savings rates, securitisation levels, and share of corporate borrowing done through markets instead of banks.

- Those member-states prepared to go deeper, for instance by merging national regulators, should be encouraged to do so.

- Prioritise swift adoption of a 28th regime to enable companies to scale quickly at the European level and enabling standardised products through a pan-European legal system.

Enhancing the single market for services

The next chapter of European growth will be written in services. There has been little progress on completing the single market for services – the EU’s largest sector and its least integrated – in the last two decades. Yet, reducing barriers to services trade and investment would boost dynamism by allowing more productive firms to scale across borders, enhancing competition within the EU and globally.

One of the EU’s main economic assets is the single market, which reduces friction in the movement of goods, services, capital and labour. In some cases, this leads capital and workers to cluster in certain places to take advantage of economies of scale: companies benefit from lower transport costs and better infrastructure, a larger pool of skilled labour, and easier access to ideas and know-how developed by other firms. These agglomeration effects can in turn foster stronger competition and accelerate innovation.

Two forces are typically unleashed when trade barriers fall. The first is clustering: firms and workers co-locate to benefit from larger markets, deep labour pools, and shared knowledge. This characterises higher-value services production, which thrives in dense urban environments. The second is unbundling: when borders open, production can be split geographically – design in knowledge hubs, routine tasks in lower-cost regions. This helped power convergence in goods markets. But services are harder to unbundle. High-value services still depend on face-to-face contact, trust, and local labour markets of sufficient size and density – so they continue to cluster.

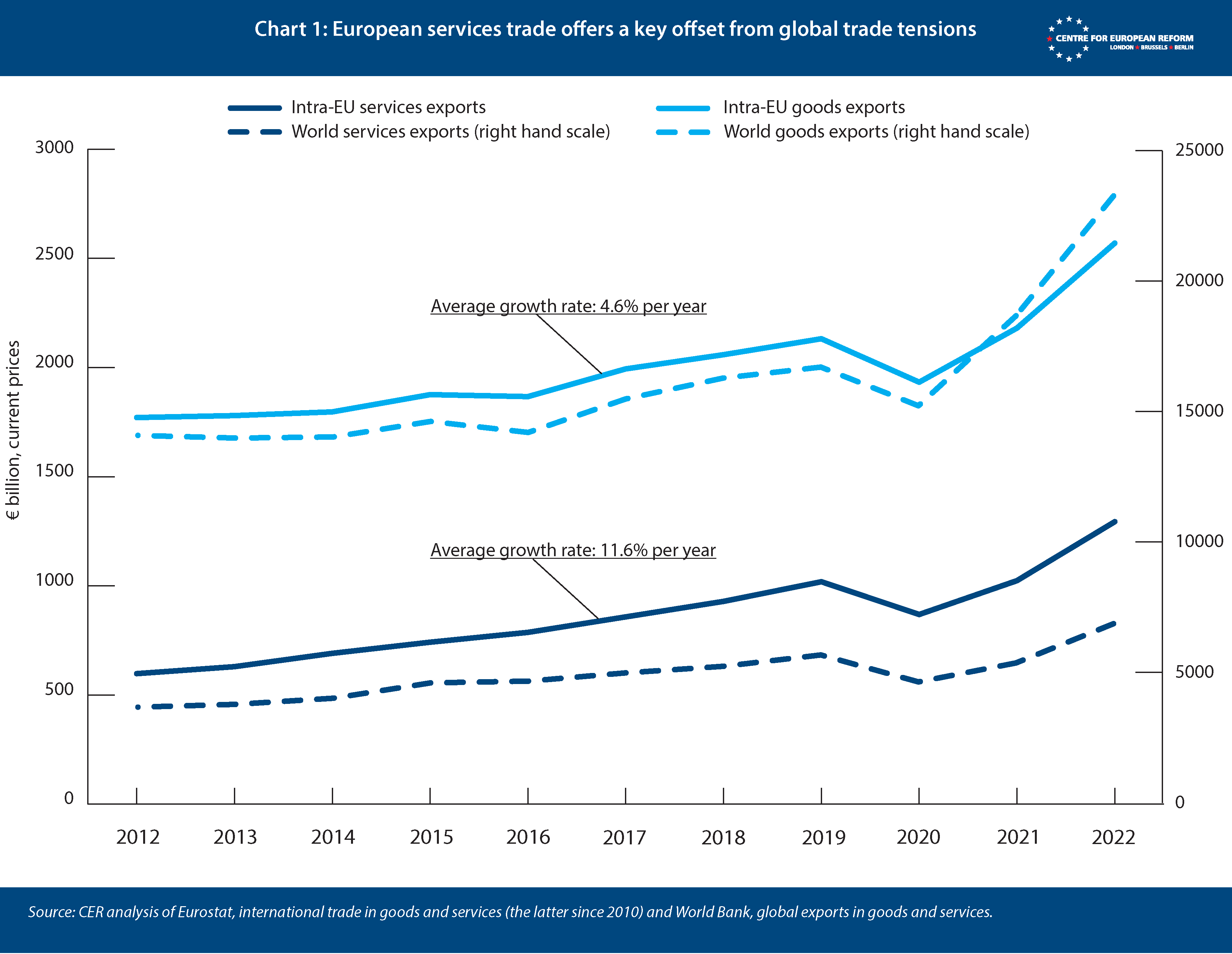

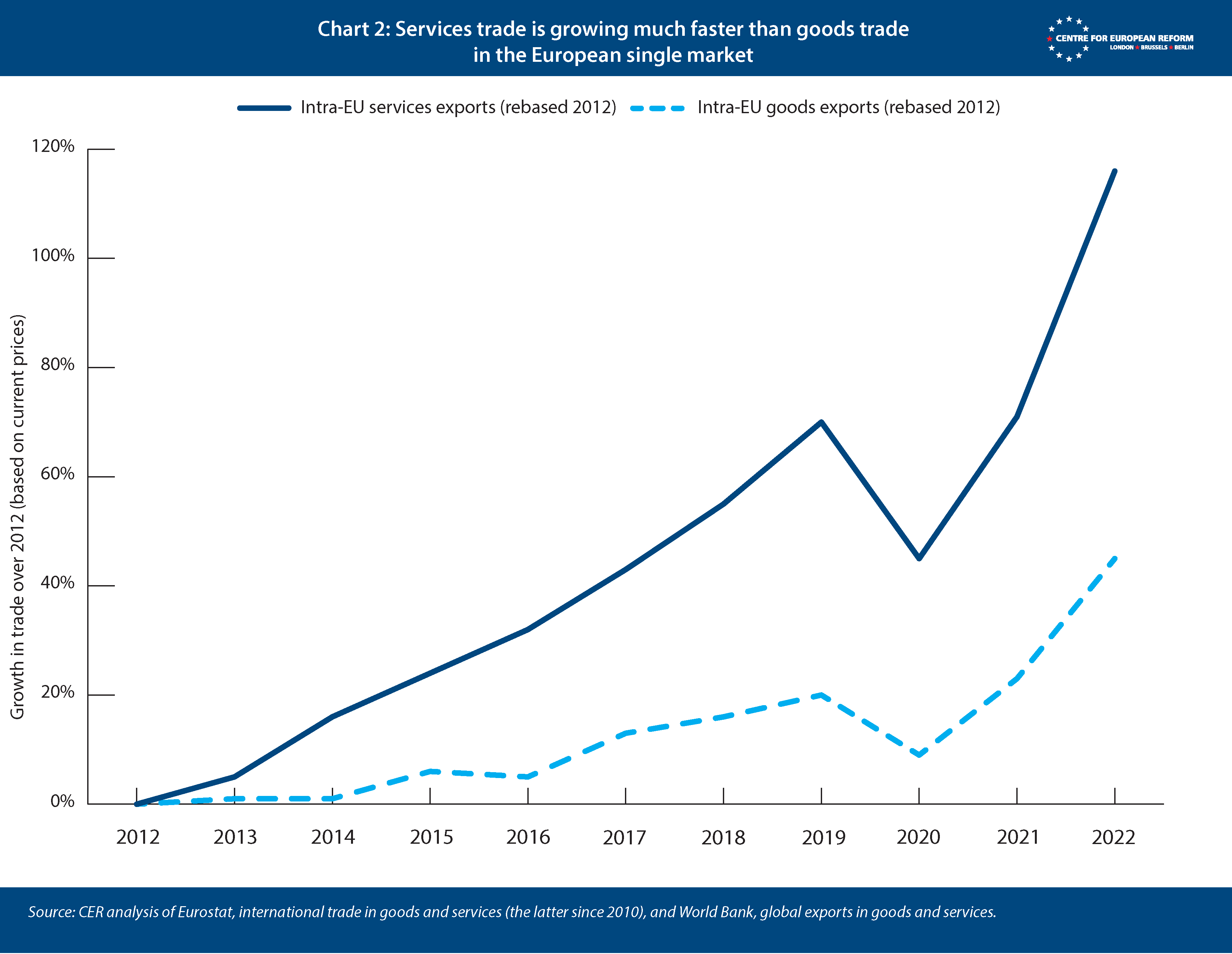

While the single market for goods drove income convergence between older member-states and those that joined after 2004, the engine of internal trade is shifting. Services now account for around 70 per cent of value added in the EU. Intra-EU services exports have grown faster than goods and far faster than global services trade. In 2012, intra-EU services exports were worth one-third the value of intra-EU goods exports; by 2022, that figure had risen to one-half. And services trade within the EU, despite doubling from 3 to 6 per cent of GDP between 1993 and 2021, still has ample room to grow. ‘Tradeability’ is almost by definition a measure of productivity: if it is possible to locate an office in one region and use it as a base to service hundreds of thousands of customers in other regions, productivity is likely to be high in terms of output per input. And higher productivity means higher income.

But services trade is not a convergence engine in the same way as goods trade. It is more ‘centripetal’ than ‘centrifugal’. Tradeable services firms cluster in places with thick labour markets, high skill concentrations, and good infrastructure. They rely on universities, research institutes, efficient public administration, and vibrant ecosystems. That is why services trade tends to concentrate in large, affluent cities.

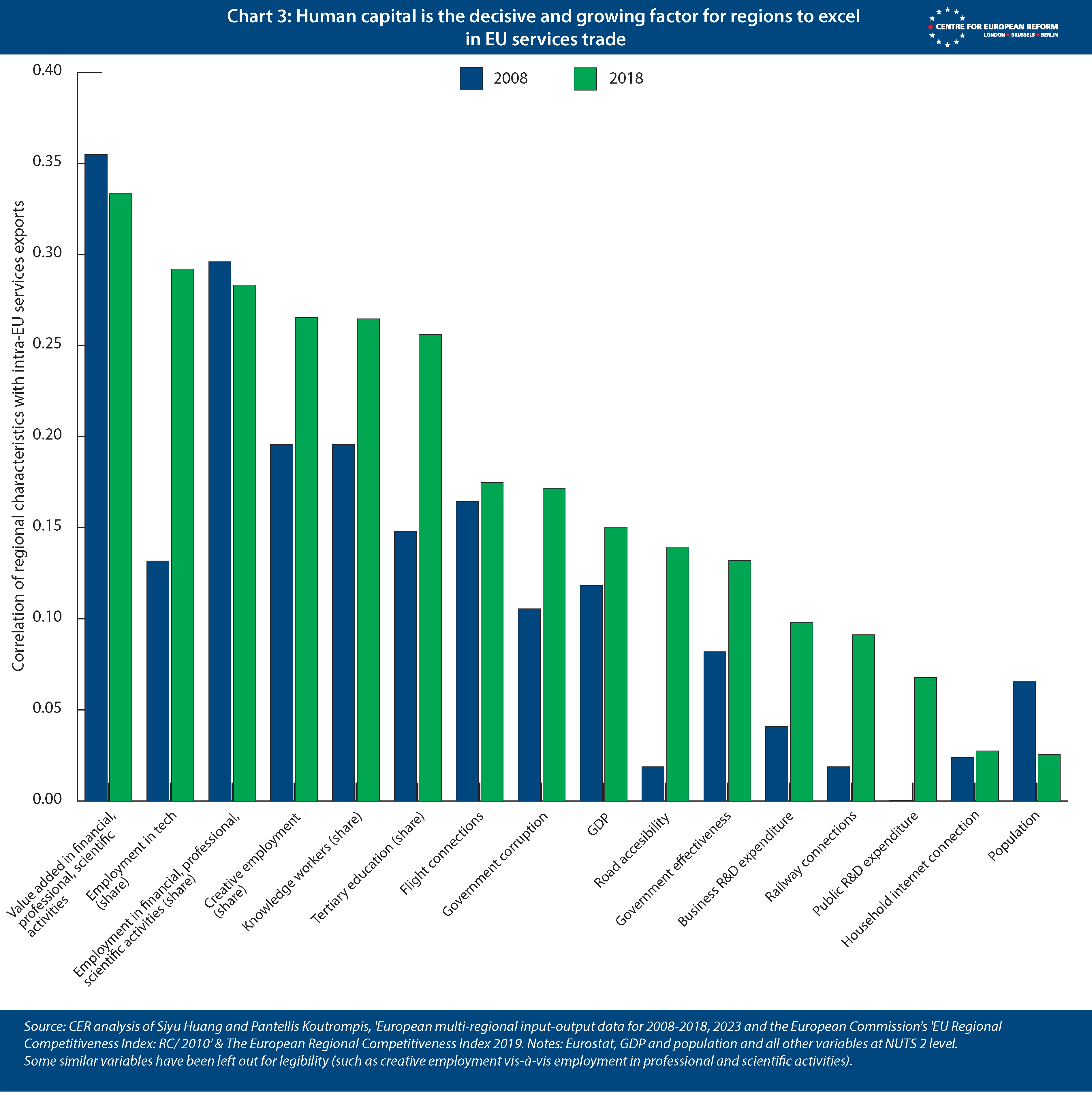

Successful service-exporting regions have high tertiary education rates, strong tech and science sectors, and effective local governance.

The most successful service-exporting regions are those with high tertiary education rates, strong tech and science sectors, and effective local governance. Cities like Amsterdam, Warsaw, Lisbon, and Prague have emerged as regional services hubs. Others – Berlin, Tallinn, Vilnius – are experiencing resurgence. And several second-tier cities are entering the fray: Krakow, Leipzig, Karlsruhe, Utrecht and Leuven stand out.

This pattern is becoming more entrenched. Between 2008 and 2018, the link between services exports and factors like GDP, population, and human capital strengthened (see Chart 3). The opposite happened in goods trade, where investment flowed to less populous, lower-cost regions in Central and Eastern Europe. Without targeted intervention, disparities between dynamic cities and their surrounding regions will widen.

These shifts present both risk and opportunity. Technological change is making more services tradeable than ever. Cloud computing, digital platforms, and AI allow firms to deliver services remotely at scale. Software engineering, legal advice, and even medical diagnostics can increasingly cross borders. Remote work has lowered barriers to collaboration. Back-office functions can be relocated to smaller cities. AI could allow services production to be modularised, just as happened in manufacturing.

But these technologies will not automatically spread economic activity more evenly. Most tradeable services remain concentrated in cities with the right mix of people, institutions and infrastructure. Even lower-skill services like logistics and warehousing cluster near metropolitan zones. Broadband access helps, but it is not decisive. What matters is the ability to attract and retain high-skilled workers.

Unfortunately, the EU’s current approach to cohesion funding is poorly aligned with this evolution. Too much is still based on static measures of income and physical infrastructure gaps. But success in the services economy is increasingly about institutions, skills, and urban scale.

Outside capitals, successful examples include Karlsruhe and Leipzig in Germany, Krakow in Poland, Valencia in Spain, and Utrecht and Almere in the Netherlands. These cities are more affordable than the capitals, but well-connected, and increasingly attractive to young professionals. They can become anchors in a more decentralised European services economy.

A city-led growth strategy can help make the most of the way in which the European economy is reshaping. Such a strategy does not imply abandoning support for poorer or rural regions. Cohesion funds will remain essential for redistributive goals. But Europe must also adopt a growth lens. Some places are simply better positioned to lead the next wave of integration. If cohesion spending ignores that reality, it risks pushing against the grain of economic change.

In fact, focusing such measures on cities outside of the capitals will help the economic diversification of surrounding rural areas by offering more opportunities for employment and retraining. If a wider variety and geographically dispersed set of cities can tap into the growing European services trade, that will cut travel times for people in surrounding manufacturing and agricultural areas to opportunities in the services sector. Workers will no longer have to locate to large or capital cities, but can work in cities closer to home, lifting incomes and productivity.

A city-led growth strategy can make the most of the way in which the European economy is reshaping.

If the EU’s budget is reformed in the next multiannual framework starting in 2027 – as it should be – resources could be shifted away from lower-impact spending and towards targeted growth-enhancing investments in human capital and infrastructure. Conditionality could help ensure funds are spent effectively, particularly where city-regions have the capacity to deliver.

Services trade is already reshaping Europe’s economic geography. The question is whether that reshaping will be accidental or intentional. A strategy that embraces the services economy, modernises cohesion policy, and empowers Europe’s cities will deliver higher wages, more investment, and more balanced growth. The EU should reorient part of its cohesion funding towards projects that unlock urban productivity in three ways:

- First, Europe should identify and support a group of ‘European growth city-regions’ – dynamic mid-sized cities outside national capitals that have the potential to become hubs for services trade. These cities should have some existing economic momentum, strong universities, and decent transport links. They do not need to be the biggest cities, but they must be capable of growing into new economic centres. Cohesion money should be redirected to these places, and investment should be focused on:

- Transport infrastructure. Fast and reliable urban transport systems – and rail links between cities and their hinterlands – expand effective labour markets. Shorter commutes reduce skill mismatches and help services firms recruit. Structural and investment funds should prioritise intra-city mobility and regional rail connections.

- Infrastructure for density. Cities need to grow vertically without suffocating congestion. That means investing in housing, water and energy systems, and public services. EU funds should help growing cities accommodate more people without displacing low-income residents or generating bottlenecks.

- Energy and digital infrastructure. The green and digital transitions are urban. Cities will need more electricity for heating, transport, and data centres. Smarter grids, battery storage, and local renewables will be essential. The EU can help cities roll out this infrastructure quickly and equitably.

- Second, the EU should place key institutions in medium-sized cities. Institutional presence matters: too often, new EU agencies are automatically placed in capitals. That is a missed opportunity. Institutions like a future AI agency, green industry hub, or cybersecurity centre could be located in smaller growth city-regions – helping to catalyse investment and attract talent.

- Third, the EU should empower cities to spend EU funds. Many cities lack meaningful control over how EU funds are spent in their territory. That is inefficient. Cities are now the key unit of economic geography – they must be empowered to plan and deliver. The EU should help member-states devolve more authority to capable city-regions. Technical assistance and performance-based funding – as in the Recovery and Resilience Facility – could help make this work.

Competition

The Draghi and Letta reports both raised concerns that the EU’s competition policy has failed to help firms scale across Europe. Draghi, in particular, links EU firms’ lack of scale with their inability to use new technologies or innovate much themselves – a leading contributor to the bloc’s low productivity growth. Letta and Draghi both argue that the EU’s competition policy should be tweaked to give more weight to considerations of innovation and growth, and to enable firms to scale. This includes potentially taking a less interventionist approach to merger policy, on the basis that in some markets the investments required to compete are so large that only very large firms with economies of scale can succeed.

In relation to mergers, the Commission president Ursula von der Leyen has asked the European Commissioner responsible for competition policy to “modernise the EU’s competition policy to ensure it supports European companies to innovate, compete and lead world-wide”. The European Commission is in the process of revising its guidelines for assessing EU mergers. A looser approach to mergers has the support of some large member-states like France and Germany, which still bristle about the Commission’s resistance to the 2019 Siemens/Alstom tie-up that the firms involved argued would have created a European champion. However, it remains to be seen whether the political direction will translate into a significantly different approach – either in the guidelines for deciding cases in general or for allowing intervention by politicians in deciding any particular case.

Too often member-states aim at protecting their ‘national champions’ rather than allowing intra-EU mergers.

The Draghi and Letta reports make some important points about the importance of scale and a true single market – and the dangers of political intervention to block cross-border mergers even if they had pro-competitive effects. Too often member-states aim at protecting their ‘national champions’ rather than allowing intra-EU mergers which could see genuine European champions emerge. This was evident in the proposed merger of Germany’s Commerzbank with Italy’s UniCredit, which was voraciously opposed by the German government. Yet, cross-border banking mergers would help banks diversify their risks; give them the scale necessary to better digitise and compete more effectively; and would help bank funding go to the best business ideas. Currently, about 75 per cent of banks’ lending portfolios are invested in their home markets.11

Nevertheless, there is a risk of reforms swinging too far the other way if they permit or encourage mergers that reduce competition. Any significant changes to the EU’s current approach to assessing mergers therefore poses serious risks of undermining competition and the single market. Given the EU’s lack of leadership in digital markets, such as cloud computing and artificial intelligence, pressure to allow a ‘European champion’ seems more likely to emerge in mature markets – where most customers are already served, competition tends to focus on price and quality, and innovations tend to be incremental. For example, much of the current policy debate revolves around mergers of mobile network operators in Europe, where EU integration appears to have gone backwards, with fewer cross-border operators now than in the past – while infrastructure-light services like internet-based instant messaging services (such as WhatsApp, iMessage, and Facebook Messenger) have grown very quickly across many European member-states. There is a general understanding that the Commission is reluctant to allow mergers which reduce the number of network operators in any EU member-state to three (or fewer). In these cases, however, scale is unlikely to produce radical new innovations or investments: telecoms technologies like 5G are highly standardised and took many years to develop, and telecoms companies largely compete over price and quality rather than innovation. The EU is already relatively well served by mobile networks and enjoys significantly lower prices for digital connectivity than the US: one of Europe’s few advantages over the US in the digital sector.

Rather, an approach which promotes in-country consolidation in mature and infrastructure-heavy markets is likely to reduce competition and raise prices for basic connectivity, weighing on the EU’s competitiveness by making it more expensive for firms to digitise. A looser competition policy would not necessarily develop the single market by promoting more cross-border business activity, since there are separate barriers to a true telecoms single market. Some of these are regulatory – for example, a single market would require politically fraught reforms in areas like radio spectrum policy, law enforcement and data retention laws, and roaming regulations, and would probably require significantly more harmonisation in how telecoms operators can access each other’s services and infrastructure. Other constraints are commercial: there are limited benefits to operating cross-border when consumer expectations, language differences, and the underlying costs of providing services remain very different from country to country. There is little evidence that the Commission – in telecoms cases or otherwise – has systemically underestimated the benefits of scale.

Competition reforms therefore risk creating a competition policy which is suitable for the unified market and high-innovation economy Europe (says it) wants – but not the fragmented markets it has. As the European Commission’s recent Competitiveness Compass states, effective competition is a key driver of economic growth. The European Commission must therefore continue to consider carefully the barriers to cross-border business when it assesses the competitive impacts of any proposed merger. It should avoid the temptation to ignore regulatory barriers which continue to exist. Instead, the Commission should pressure member-states – if they want a looser competition policy – to remove barriers to a true single market.

The Commission could, however, use its review of the merger guidelines to give more weight to innovation when it reviews mergers in markets that have greater potential for disruptive innovation. European authorities have on several occasions taken a sceptical view of a proposed merger based on how the deal might negatively impact innovation. However, the Commission has been less willing to see innovation as a potential pro-competitive justification for a merger. Currently, no firms have tried to put forward such an argument, in part because of perceptions that the evidentiary threshold that a merger would benefit innovation is too difficult to meet.

If used in high-tech industries, such as digital software, such an approach could help European tech firms scale up more quickly, boosting Europe’s innovative capacity, and ensuring today’s de facto single market for digital services is not solely dominated by foreign tech firms’ services and platforms. That is because existing barriers to entry and expansion across Europe (and elsewhere in the world) are significantly lower than in more heavily regulated sectors, meaning that mergers are less likely to significantly reduce competition.

The EU must ensure that, despite political pressure to allow European champions, the foundations of European competition are protected. To do this the EU should:

- Discourage political interference which would block or dissuade firms from pro-competitive intra-EU mergers. A true European single market demands that European firms can engage in M&A activity across the bloc. Member-state interventions which aim to discourage this behaviour – the detrimental impact on the single European market – should be strongly discouraged by the EU institutions.

- Adopt an economic-informed approach to revising the Commission’s approach to mergers. The Commission is currently revising its guidelines for assessing mergers. Inevitably, the guidelines will need to provide an updated approach which reflects the importance of scale, the prospects for radical innovation in some sectors, and the nature of global competition. However, these should not result in the Commission ignoring reality, for example by treating the EU as a single market in cases where regulatory barriers and divergences mean that firms only compete with their domestic competitors.

- Take a context-specific approach to the importance of scale and innovation. The Commission should consider how to make it easier for firms to argue that their merger will have positive effects on consumers through greater innovation. However, these impacts will be more likely to occur in fast-moving digital markets than those which are infrastructure-heavy and where technological development is standardised. The Commission must ensure any changes to merger policy do not allow in-country mergers in sectors – such as telecoms – where competition would be reduced, and where mergers could raise prices while providing only questionable benefits for investment and innovation.

Conclusion

Europe faces a number of well-known challenges: weak productivity growth, high energy prices, ageing societies and a challenging external environment.

But it also has considerable assets: world-class companies, good infrastructure, a highly educated and skilled workforce and the capacity to reform and change. By doing the latter it can boost innovation and productivity growth and provide cheaper, clean energy. There is now a broad consensus on the need for action in Europe. There is even a consensus on what problems need to be addressed. The time now is to turn words into action, and action into results that can ensure the EU will remain fit for the 21st century.

2: IMF staff background note on EU energy market integration, January 2025.

3: John Springford, ‘Power losses: What’s holding back European electricity trade?’, CER policy brief, April 2025.

4: ACER, ‘Transmission capacities for cross-zonal trade of electricity and congestion management in the EU. 2024 Market Monitoring Report’, July 2024.

5: The review is led by the EU Agency for the Co-operation of Energy Regulators (ACER) and by the European Network of Transmission System Operators for Electricity (ENTSO-E). See ACER, bidding zone review (webpage consulted in July 2025).

6: ACER, Final assessment of the EU wholesale electricity market design, 2022.

7: ACER, ‘Transmission capacities for cross-zonal trade of electricity and congestion management in the EU. 2024 Market Monitoring Report’, July 2024.

8: European Commission, Joint Research Centre, Georg Thomassen, Andreas Fuhrmanek, Rade Cadjenovic, David Pozo Camara and Silvia Vitiello, ‘Redispatch and congestion management’, 2024.

9: Maureen O’Hara and Xing Zhou, ‘US corporate bond markets: Bigger and (maybe) better?’, Journal of Economic Perspectives, Volume 39, Number 2, Spring 2025.

10: New Financial, ‘EU capital markets: A new call to action’, September 2023.

11: Francesca Lenoci and Philippe Molitor, ‘Intra-euro area cross-border bank lending: A boost to banking market integration?’, ECB, June 2024.

Aslak Berg, research fellow, CER, Elisabetta Cornago, assistant director, CER, Zach Meyers, director of research, CERRE and non-resident associate fellow, CER and Sander Tordoir, chief economist, CER.

October 2025

This publication receives funding from the European Parliament. The European Parliament and the Wilfried Martens Centre for European Studies assume no responsibility for facts or opinions expressed in this publication or their subsequent use. Sole responsibility lies with the authors of this publication.

View press release

Download full publication