How buy-European rules can help save Europe's car industry

- Europe’s car industry employs more than 10 million people and accounts for a larger share of private R&D spending than any other industry. European cars can still compete in the 21st century: the EU is already the world’s second largest electric vehicle (EV) producer.

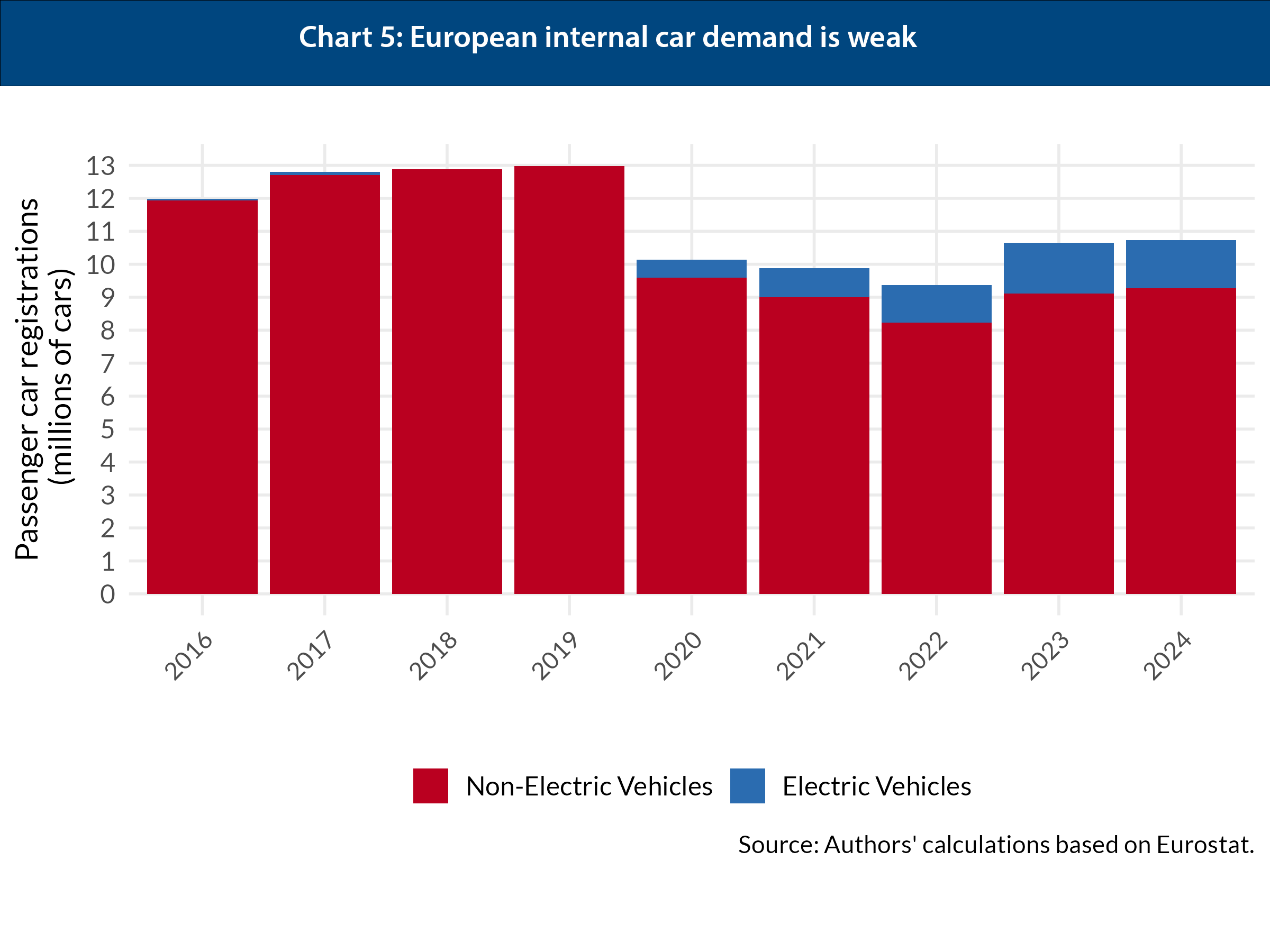

- But the sector is facing a perfect storm. Thanks to widespread subsidisation and genuine innovation, China’s global car exports are exploding, and European exports are being squeezed out of global export markets, starting with China. EU car exports to the United States (US) almost doubled between 2019 and 2024, but President Trump’s 15 per cent tariffs and his rollback of EV subsidies will deal another blow. EU domestic demand, meanwhile, is weak.

- Governments will come under massive pressure from trade unions and the public not to let car companies fail. The risk is an ineffective and costly muddle of regulatory rollbacks, firm-specific bailouts and a patchwork of national subsidies.

- The lopsided focus on prolonging the viability of internal combustion engine (ICE) cars exemplifies the EU’s poorly thought-out approach. It involves extending both the 2035 deadline for phasing out new ICE vehicles and the 2027 deadline for expanding the EU’s carbon pricing scheme to road transport.

- Future cars will be electric, not because of regulation, but because EVs will soon be substantially cheaper. If Europe’s car industry is to survive, it must pivot faster to producing EVs that are high-quality, affordable and profitable.

- Europe’s carmakers face an EV engineering lag, a battery and software gap and patchy charging infrastructure. These are hard to fix quickly. Counteracting weak demand, and offsetting lost export demand, by contrast, are issues the EU can address.

- Rather than tampering with regulations, EU policy-makers should ensure that demand from Europe’s huge single market, with 450 million consumers and a vast corporate sector, spurs European production. That primarily means supporting demand through consumer subsidies, with a buy-European clause co-ordinated across member-states.

- Most member-states already have support schemes for EVs in place, but they are completely uncoordinated. There is now a unique chance to do better, as the EU overhauls its corporate car fleet regulation and key member-states create new EV subsidies.

- To align demand-support schemes across the EU, the Union should:

- Europeanise the French eco-bonus. The French model, with its carbon-based scoring system, is the most practical template to adopt across member-states. It effectively steers demand toward European-made EVs and filters out Chinese production, because it limits subsidy to EV models produced in low-emission supply chains. It will need updating, but it is effective, WTO-proof and ready to deploy.

- Let big member-states lead. Germany, France, Spain and Italy together account for 70 per cent of EU new car registrations. To support its car sector, Germany has just committed to reintroducing EV subsidies. Equipping them with the eco-bonus would align Germany with France and support a buy-European policy. Italy and Spain, which are reviewing their subsidies next year, could then follow suit. The Commission has already approved the eco-bonus as permissible state aid, making it the ideal model to roll out across the single market, preventing fragmentation and stoking demand for all EU-built EVs.

- Cover both households and corporate fleets. Household EV purchases backed by subsidies would cover only 40 per cent of the total European car market. Over 60 per cent of EU new registrations are company cars which already benefit from sizeable subsidies. Support schemes for corporate EVs should also be conditional on European content requirements. Ensuring that buy-European subsidies apply to both markets would also allow Germany to secure demand for premium models, common in corporate car fleets, while France, Spain and Italy gain scale in the smaller cars which are more common in the household market.

- Engage export partners. Most EU car exports go to a handful of allied advanced economies similarly worried about Chinese overcapacities. A European eco-bonus could be a springboard to negotiate reciprocal access to EV subsidies with allies and free-trade partners and ensure global demand.

- Our proposal has major economic advantages:

- First, instead of rearguard fights over regulation, a demand-side push for European EVs would spur the transformation of the sector – essential to remaining competitive in adjacent technologies such as autonomous driving, batteries and software.

- Second, buy-European clauses would help avoid rapid deindustrialisation, safeguarding employment without ossifying current labour-market structures. The sector will inevitably undergo skill and geographic shifts, but higher demand would support overall employment while allowing necessary restructuring.

- Third, because buy-European clauses would be open to producers across the EU, the policy would not require policy-makers to pick ‘winners’. German tax incentives would also help French producers, and vice versa. A harmonised EU framework could avoid subsidy fragmentation, foster competition in the European market, and level the playing field with China, which excludes foreign vehicles from its own subsidy schemes.

- A European eco-bonus implies an additional fiscal cost, but many member-states already subsidise household and corporate EV purchases. Better co-ord inated and additional support would deliver a strong bang-for-the-buck: it would build scale in future technologies, and shield the car industry from geopolitical shocks more efficiently than a number of disparate national schemes.

Car manufacturing was the pinnacle of 20th century industrialisation. Even today, the industry remains one of Europe’s most important sectors, if not the most important. It employs 13.6 million people, directly and indirectly, and accounts for 32 per cent of all private R&D spending – more than any other sector.1,2 While the EU undoubtedly needs to catch up with the US in information technology and artificial intelligence, manufacturing still carries far greater weight in its economy, and cars are at the heart of it.3 Yet as it manages the arduous transition from the internal combustion engine (ICE) to electric vehicles (EVs), the European automotive sector is under pressure from Chinese overcapacity, US tariffs and sluggish domestic demand. Germany’s net car exports have fallen by 50 per cent since before the pandemic, while France and Italy have faced declining car exports for even longer.4

But the debate over how to save European cars risks driving completely off-track. Across the continent, policy-makers narrowly fixate on the EU’s 2035 phase-out of internal combustion engines and future EU carbon price hikes. This focus on regulation which only kicks in fully a decade from now overlooks the geopolitical shocks hitting European car firms today. The International Energy Agency expects one in four cars sold worldwide this year to be electric, and the global EV fleet to quadruple to 250 million vehicles by 2030.5 EVs are also set to become more affordable than ICE vehicles in the near future, as EVs entail a higher up-front cost but are cheaper to use.6 Some politicians and economists who accept the inevitability of the EV transition nonetheless oppose intervention, insisting that the market should sort out the future of the sector. That, too, ignores reality: China’s automotive industry is heavily subsidised, and Trump’s tariffs have already distorted trade. To call this a market-driven dynamic is an armchair economist’s view.

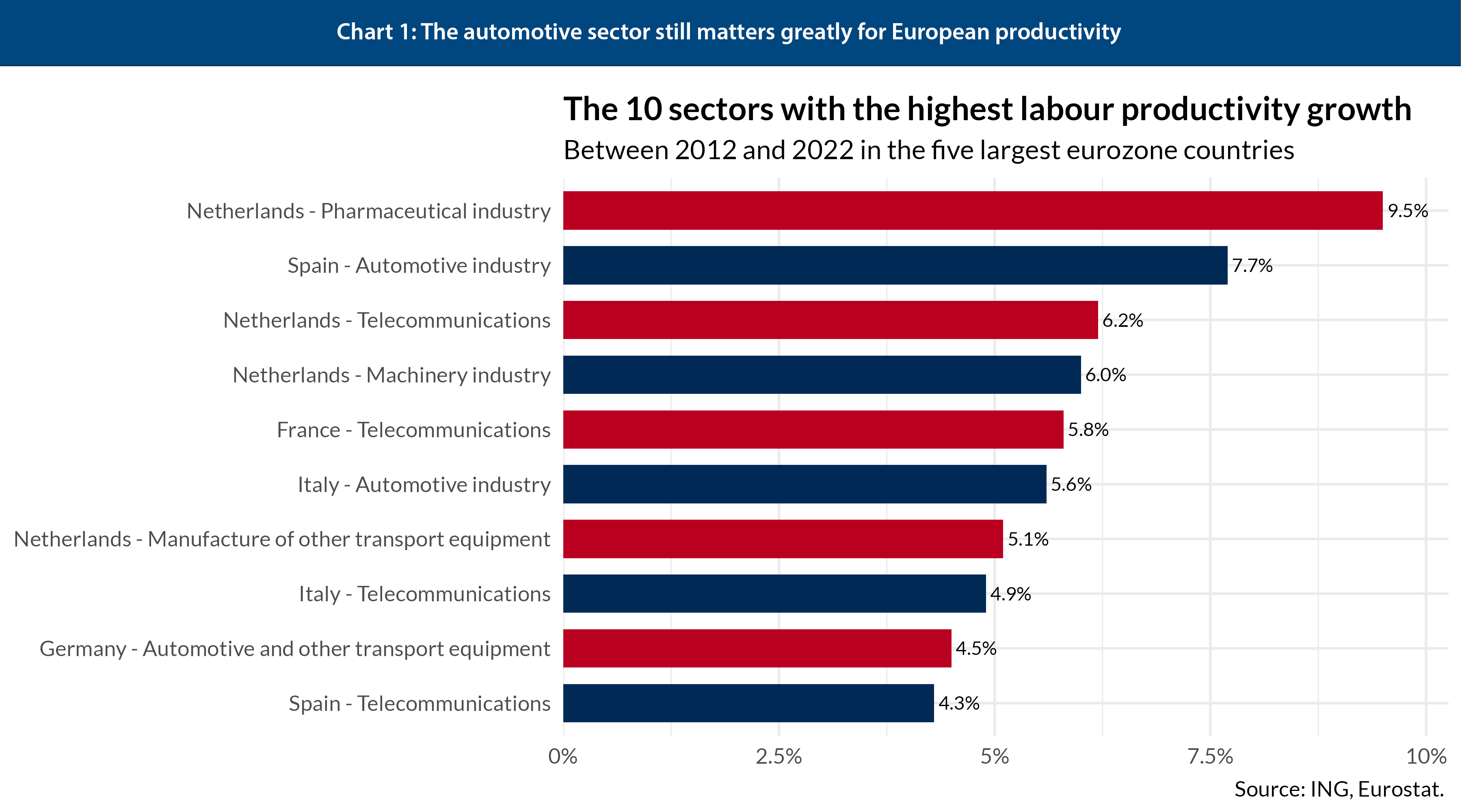

The fate of European car-making is not sealed, and policy support can help. There are encouraging signals that Europe’s automotive sector can compete in the 21st century, even if it will be smaller than in the past. Germany is already the world’s second-largest producer of EVs, ahead of the US, and more than a quarter of its car exports are now electric.7 The EU as a whole also runs a modest trade surplus in EVs, primarily thanks to exports to markets like the US, UK and Norway. Cars still matter greatly for productivity growth: four of the ten sectors with the strongest productivity growth in the five largest eurozone economies between 2012 and 2022 were in automotive and transport (see Chart 1). As long as Europe is still trying to catch up in information technology, manufacturing – with cars at the centre – will remain the locus of what little productivity growth the continent ekes out.

Moreover, the sector has immense political influence: its unions are very powerful, the companies in question are household names and the regions that stand the most to lose from the decline of the sector are mostly well-off and politically potent. There should be no doubt that governments will intervene to save the European car sector – the question is whether they will do it well, and whether they will do so with European co-ordination to leverage its massive market.

Europe’s carmakers face structural supply-side challenges. Europe was long a leader in combustion-engine design, but is struggling to catch up in EV engineering. The bloc suffers from a gap in battery manufacturing and is held back by patchy charging infrastructure and inconsistent subsidies across member-states. All these elements slow down adoption, especially in the largest member-states. Digitalisation also lags, curbing the EU’s ability to build ‘iPhones-on-wheels’, as cars become increasingly software-driven.

But the argument of this paper is more focused and immediate: today, the decisive threats to Europe’s automotive sector are not only supply-side driven but at least as much coming from the demand-side. US tariffs, the rollback of provisions from the US Inflation Reduction Act (IRA) that drew in EU-built EVs, and above all China’s surging exports amount to a massive demand shock for Europe’s car industry. And while European governments cannot fix global demand for European cars, they can do something about weak demand at home.

China is hammering European car making

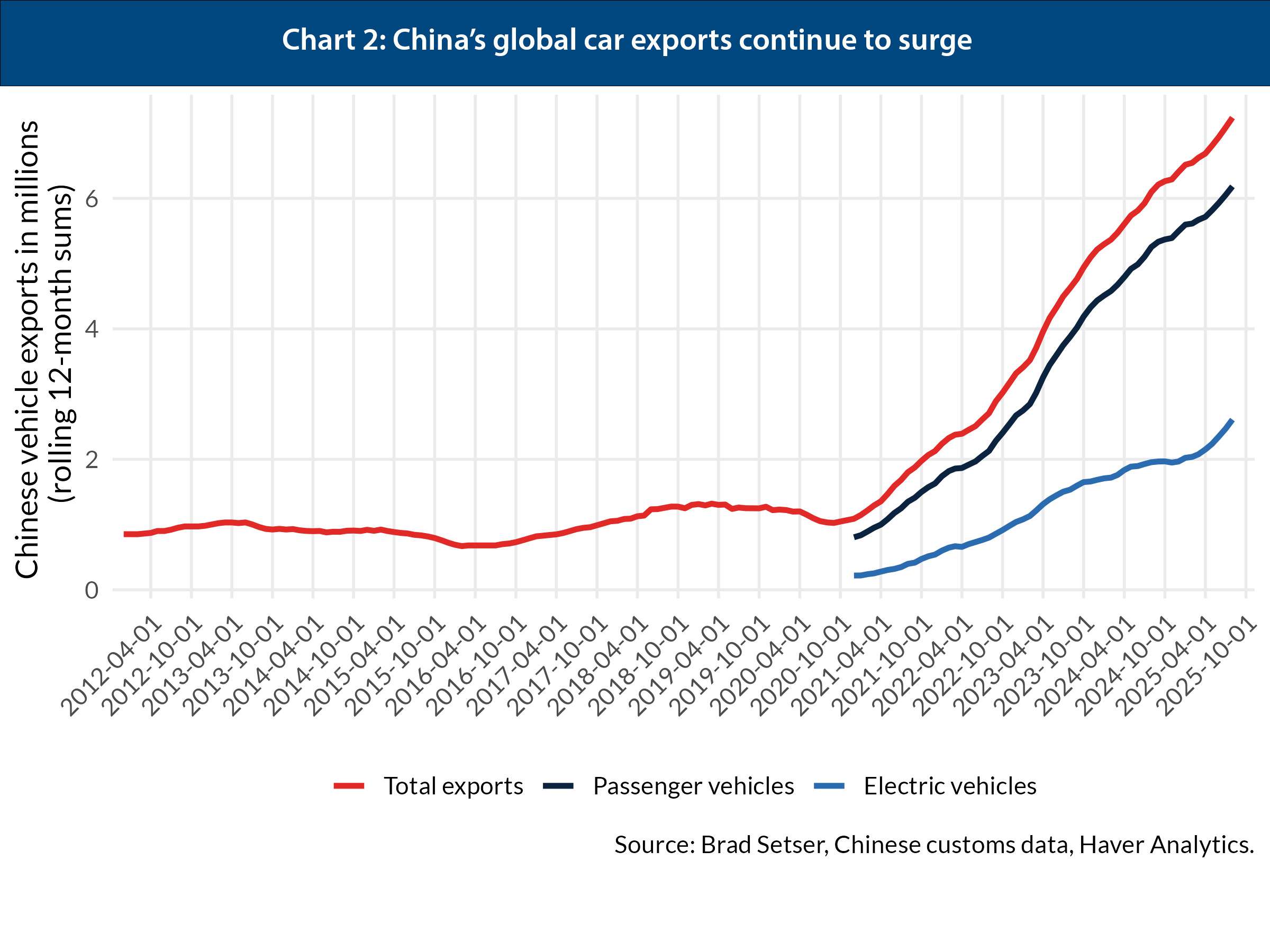

Thanks to widespread subsidisation, forced Western technology transfer and genuine innovation, China’s rise in the global car trade has been breathtaking.8 In 2020 China was not a net car exporter; now it is by far the world’s largest. China has shipped more than 7 million vehicles over the past year. As Chart 2 shows, whilst China leads in EVs, it still exports far more ICE vehicles, calling into question the idea that Europe can hide from Chinese competition by ditching climate targets and clinging to the past.

And China’s car exports keep rising, on a trajectory that is unlikely to change. That is unsurprising: with the capacity to build more than 50 million cars annually – roughly double China’s domestic demand and over 60 per cent of global demand – China’s potential to export even more vehicles is near limitless.9 The scale of China’s subsidies is staggering: the IMF recently estimated China’s industrial policy support at 4.4 per cent of GDP – multiples of the levels in advanced economies.10 Cars remain the key focus. The export surge is also driven by deeply entrenched macroeconomic imbalances. Since the late 1980s, China’s growth model has relied on chronically low consumption and the redirection of excess savings into state-led investment. When the property bubble burst in 2021, those savings were channelled into priority industries despite weak domestic demand. That is precisely when the car export surge began.

Chinese policy-makers themselves worry about the domestic implications of the continual supply expansion: this dynamic has unleashed destructive price wars in EVs and other sectors across China – a phenomenon they call ‘involution’. But it will be difficult to stop the export engine now, as provinces have built and continue to add to car-making capacity that domestic demand cannot absorb. Indeed, the growth rate for new industrial lending has roughly quintupled.11 If history is any guide, the Chinese government is unlikely to raise domestic demand to rebalance global trade, and will instead employ a tried-and-tested playbook of shutting down weaker producers and curbing production here and there. But these measures are unlikely to solve Beijing’s fundamental problem of having far too many car plants looking for demand.

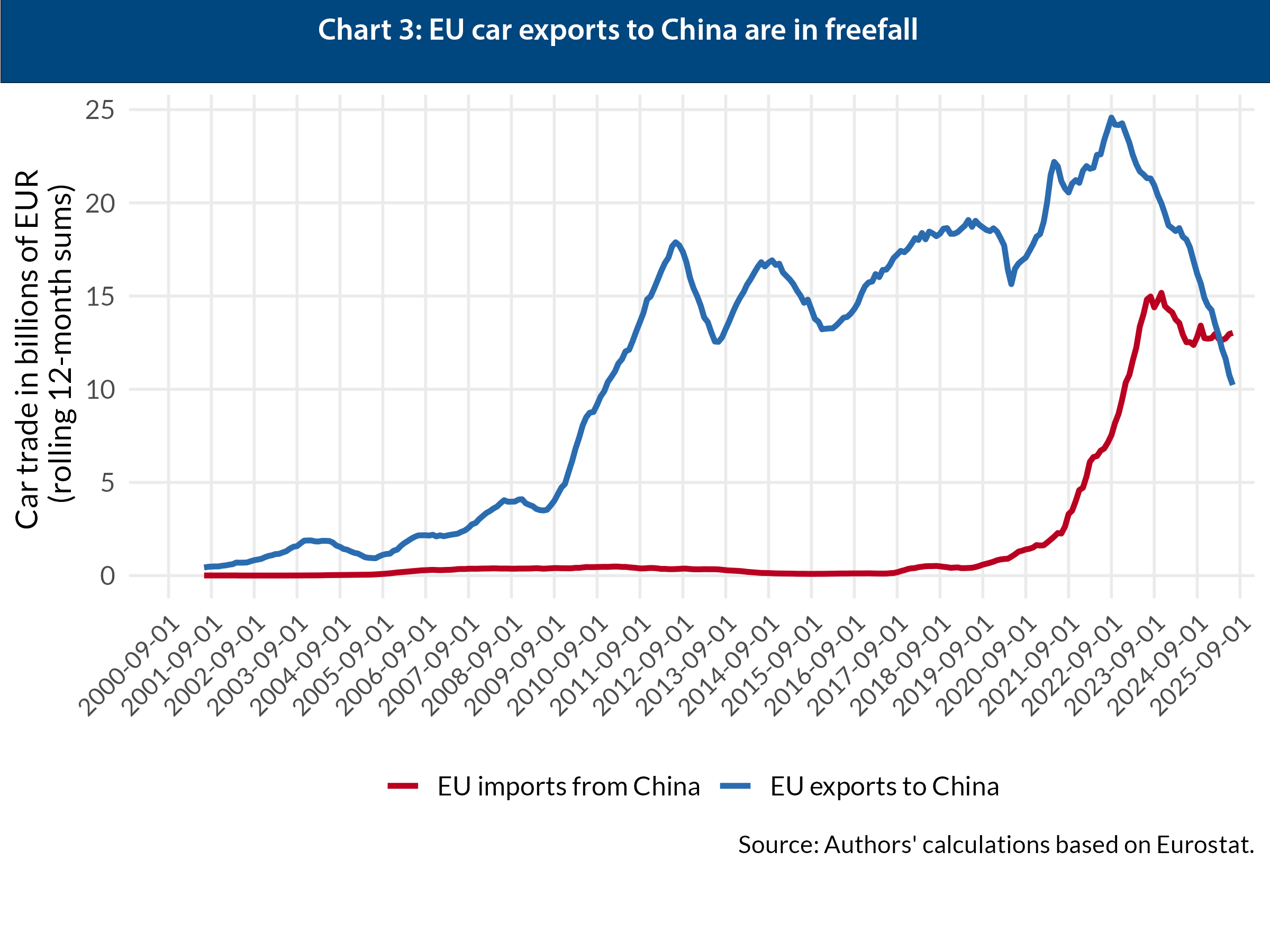

For Europe, the consequences are threefold. First, Chinese demand for European vehicles is shrinking (see Chart 3). Car exports to China are in freefall: the Rhodium Group (a research company focusing on China) recently showed that in 2024 Chinese imports of all foreign-made cars and parts fell by 28 per cent compared with 2021 and continues to drop.12 As a result, European-based carmakers see demand and the associated profits rapidly evaporating. Even for firms heavily invested in production ‘in China, for China’, prospects are deteriorating. A brutal price war and the shift of Chinese consumers to domestic brands have cut foreign carmakers’ market share from 60 to 40 per cent, with both revenues and profits still trending downward.

Second, Europe is losing demand in third markets. Chinese car exports are running at an annualised pace of around 8 million vehicles – seven times Germany’s net exports today, and four times its historic pre-pandemic peak. If China sustains this trajectory, its net car exports will exceed the combined car exports of Europe and Japan, pushing European cars out of third markets. In the first half of 2025, for example, China’s top ten export destinations included key markets for EU car exports like the UK and Mexico.13

Third, Europe faces intensifying competition at home. Chinese producers – including foreign brands that manufacture in China for export back to Europe – have already captured 20 per cent of the European EV market.14 China has rapidly overtaken Japan, South Korea and other major trading partners to become the largest source of European car imports (see Chart 4). The home market that once anchored Europe’s car industry now risks being eroded.

The EU’s tariffs on Chinese EVs, adopted in late 2024, comply with WTO rules but are insufficient to deal with the three-way demand shock. China’s car exports to Europe itself have recently slowed thanks to the EU’s duties and bottlenecks at ports and a lack of Chinese dealership networks in Europe.15 But BYD, China’s leading carmaker, is already expanding its fleet of car ships to break through shipping constraints, suggesting these obstacles are unlikely to alter the long-term trajectory.16

The EU’s countervailing duties also only offset measurable firm-level subsidies and do not cover hybrid cars. They are also blind to the edge that Chinese carmakers have built up through accumulated sectoral state support over the last decade. This has included subsidies for battery production, raw material refining and EV component suppliers, and the boon from overcapacity and rock-bottom prices in input industries like steel.

The EU’s duties similarly do not account for China’s macroeconomic policies, such as the undervalued renminbi exchange rate, which has fallen by another 10 per cent against the euro this year, making Chinese cars and other exports even cheaper abroad. But above all the duties do nothing to offset lost export demand in China or in third markets. That is especially worrying because US demand for European cars is about to take a hit, too.

The vanishing US offset

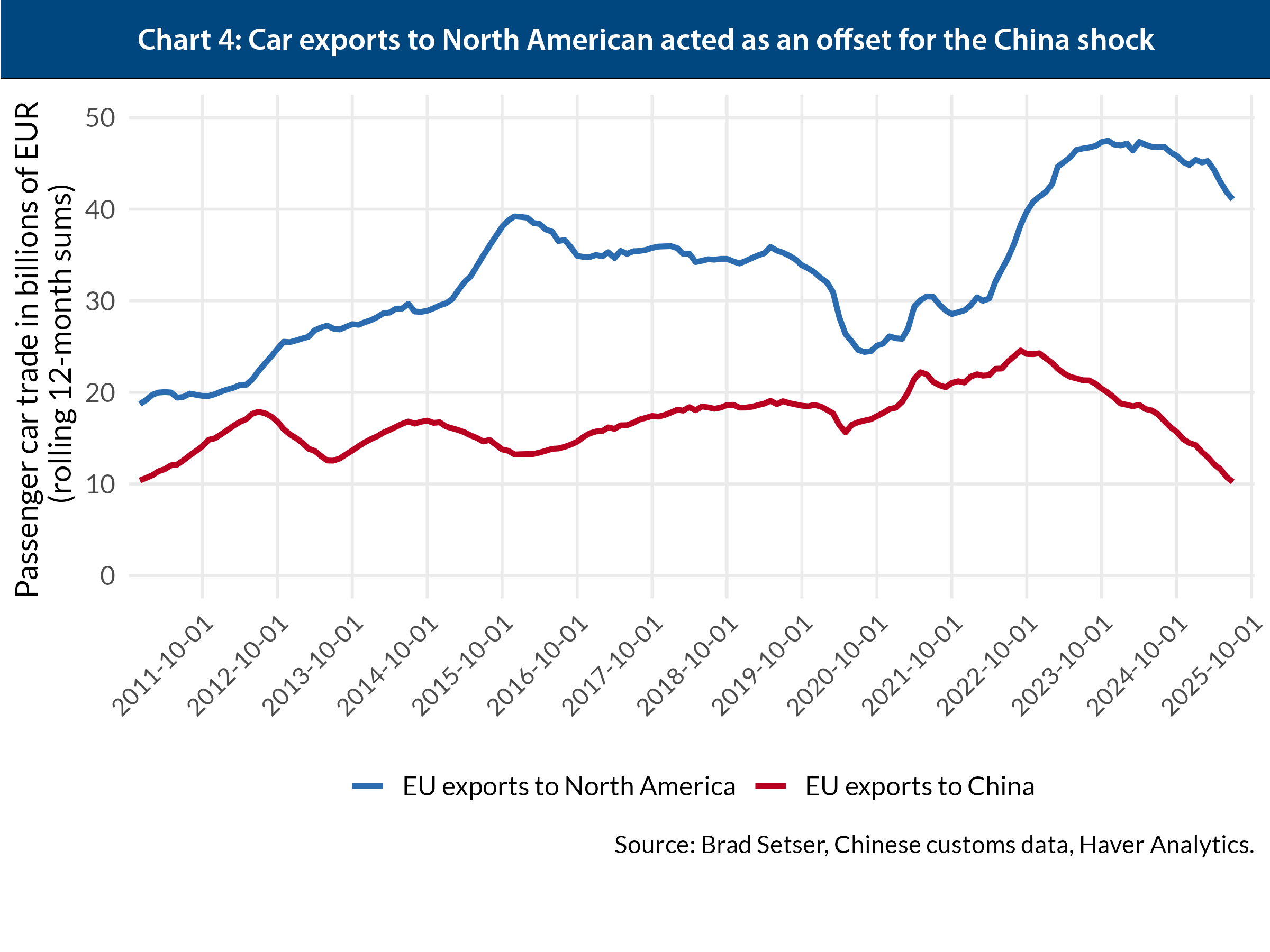

For a time, the North American market offered Europe’s carmakers an important offset from the China shock, helped by prohibitive 100 per cent US tariffs on Chinese cars. EU car exports to North America almost doubled between 2019 and 2024, from $25 billion to just below $50 billion (see Chart 4) – a business still dominated by ICEs but with a rapidly growing share of EVs. When President Joe Biden launched his Inflation Reduction Act in 2022, many in Europe feared an investment exodus as US green subsidies made domestic production more attractive. But in practice, the US stoked demand for clean tech, including EVs, which pulled in more European imports.

The Biden administration extended IRA tax credits to European-built EVs exported to the US for leasing – a loophole to accommodate the fact that the EU, like South Korea, did not have a formal free trade agreement with the US. This loophole quickly became crucial, as the leasing market makes up around a quarter of the US market, and almost half of the EV market.17 By 2024 nearly two-thirds of EU EV exports to the US were for lease, allowing European producers to tap into generous American tax credits.18

That cushion is now vanishing. The Trump administration has scrapped the IRA’s EV credits (the $7,500 credit expired at the end of September 2025), begun rolling back federal support for charging infrastructure (cutting $5 billion for charging points on highways), and above all imposed new tariffs on European car imports.

Under the August 2025 US-EU trade deal, EU car exports now face a 15 per cent tariff. This is below the prohibitive level of 30 per cent initially threatened by Trump. However, it still represents a six-fold increase over the previous level, comes with plenty of uncertainty and has already affected trade: European car exports to the US fell by 13 per cent in the first half of 2025.19 German car exports to the US rose nearly 15 per cent year-on-year in the first quarter of 2025 but plunged by 13 and 25 per cent in April and May respectively, after the tariffs took effect.20

Much about the future of EU-US trade relations remains uncertain. If inputs such as steel, aluminium or semiconductors face steep tariffs, US-manufactured cars will be less competitive than imported vehicles from the EU. Duty drawback rules let companies that build cars both inside and outside the US pay less in import taxes. They can offset the duties on cars they bring into the US with the cars they export from the US. These rules could help EU carmakers, who have sizeable plants in the US, to reduce the tariff bill but whether they legally apply to the Trump tariffs remains unsettled.21 On the other hand, if Canada and Mexico – which are key supply hubs for US-based car production – ultimately secure lower tariffs than the EU, this could draw car production investment from Europe to North America. What is clear is Washington is no longer willing to absorb more European car exports. What was once a growth market, buoyed further by IRA subsidies, is turning into another source of strain for European carmakers.

European car demand is weak

While EU producers are being squeezed out of the Chinese and US export markets, domestic demand has offered little relief. New car registrations in the EU collapsed during the pandemic and never fully recovered. In 2024, they were still about 20 per cent below pre-crisis levels, with an even steeper decline in key markets such as France and Germany (Chart 5).

The limited sectoral growth has largely been driven by rising electric vehicle sales. EV sales increased from around 250,000 cars in 2019 to about 1.45 million in 2024. While the pace of growth has slowed in recent years, there are now tentative signs of recovery. Battery electric vehicle (BEV) sales (that is, excluding hybrids) from European producers rose by 38 per cent in the first seven months of 2025, and falling battery prices, together with announcements of new affordable models from several European manufacturers, have raised hopes of a faster roll-out.22 But the pace remains far too slow to offset the slump in overall demand, let alone the loss of global markets.

Steering European demand toward European EVs

Faced with rapid, regionally concentrated de-industrialisation in the car sector, Europe’s politicians will not sit idle. Nor should they, given how central cars remain to productivity, research and development, and the wider industrial ecosystems forming around EVs. But if they wait for pressure from trade unions, firms and voters to mount, they risk creating a costly muddle of regulatory rollbacks, firm-specific bailouts and a patchwork of national subsidies to prop up the car sector – only for the industry to slow-walk into oblivion anyway. The EU, like the US, could also raise tariffs on Chinese cars to prohibitive levels, but that would violate its WTO commitments and further damage the global trade order. Domestic support schemes are also less likely to exacerbate trade tensions with China itself.

What is needed is a joint European industrial strategy, built on Europe’s greatest asset: the demand for cars in its single market, with 450 million consumers and a vast corporate sector that leases millions of vehicles. Two simple principles should guide policy. First, all public support for EVs – whether tax breaks or subsidies – should apply only to cars made in Europe or in allied countries. Second, the eligibility rules should be harmonised across the EU, so member-states are not busy outsmarting each other while losing the global race. Such a harmonised European preference for EV support would come with several major advantages.

First, relying on demand incentives rather than handouts to firms would safeguard employment without freezing current labour market structures. Because EV production differs from ICE production, employment will inevitably shift in terms of both skills and geography, although a growing body of research suggests it is not necessarily less labour intensive.23 A buy-European clause would support overall employment by boosting demand without obstructing necessary structural change.

Second, demand-side support for European EVs would accelerate the sector’s transformation, instead of slowing it down. Every year that European producers (and consumers) cling to the cars of the past, the gap between them and the technological frontier widens. Consumers miss out on certainty amidst the flip-flopping and hold back on purchasing EVs. Building an edge in EVs is also essential to remain competitive in adjacent technologies such as autonomous driving, batteries and automotive software, and for staying in the race for emerging EV markets worldwide. A targeted demand push for EVs would provide incentives to move faster, rather than trap European policy-makers in endless fights over ICE bans and phase-outs.

Third, harmonised buy-European clauses would offer a single-market-friendly form of industrial policy. They would not require policy-makers to pick national champions but would be open to all EU producers: German tax incentives would also help French and other European manufacturers, and vice versa. A harmonised EU framework could avoid subsidy fragmentation, stimulate genuine competition inside the club, and level the playing field with China, which excludes foreign vehicles from its own subsidy schemes.

Fourth, it would not require any resources at the EU level. There is no common pot for a Union-wide subsidy programme to support EV purchases. The EU budget is only around 1 per cent of GDP, and is fully dedicated to other spending programmes until the end of 2027 – it lacks the firepower for broad demand-side subsidies. Commission President Ursula von der Leyen’s attempts to create a European Sovereignty Fund to underpin industrial policy have come to nothing, and while there are plans for a more muscular successor in the next EU budget, its size and focus remain uncertain. Besides, any European money would not arrive before 2028, and Europe’s car industry cannot wait till then. That leaves harmonising member-states’ EV schemes as the only way forward.

Finally, it would put an end to a patchwork of national schemes. Most member-states already subsidise household EV purchases. Italy recently announced a new scheme worth up to €11,000 per vehicle, with annual costs of around €600 million.24 Greece and Portugal each offer roughly €9,000, with total spending of about €10 million in Portugal and €60 million in Greece.25,26 France has trimmed its EV subsidy budget but still maintains a sizeable package – around €1.5 billion in 2024 and €700 million in 2025 – and the same holds for Spain, Sweden and Denmark.27 Germany is one of the few countries without direct subsidies, after its Umweltbonus programme (€2.4 billion in its last operating year) ended in 2023 when the constitutional court struck down its fiscal underpinnings. All these subsidy schemes have different conditions embedded in them, such as eligibility, price caps and income adjustments. But above all, member-states mostly do not tie their programmes to local production. Member-states’ subsidies thus risk further subsidising Chinese cars. It is a prime example of how Berlin, Brussels, Paris, Rome and Madrid conduct industrial policy in a fragmented and unco-ordinated way to the detriment of all – something Mario Draghi criticised sharply in his 2024 landmark report.28

One immediate question is why member-states would give up the discretion to set their own criteria for national support schemes. The answer is that they have a self-interest in doing so. For one thing, the sector is already highly integrated, and the cross-border effects are obvious. Czechia, Austria and Slovakia, for example, are tightly bound into German supply chains, and their gross domestic product has stagnated along with Germany’s. Similarly, Italian parts exports to Germany fell by 20 per cent in 2024.29 Europe’s car industry depends on German strength in the sector, and the relationship runs both ways. In 2023, German exports of engine parts to France, Italy and Spain, for example, reached roughly €1.8billion, far outweighing its inputs into US and Chinese supply chains.30 In short, these are not isolated markets: member-states producers have a direct stake in each other’s success.

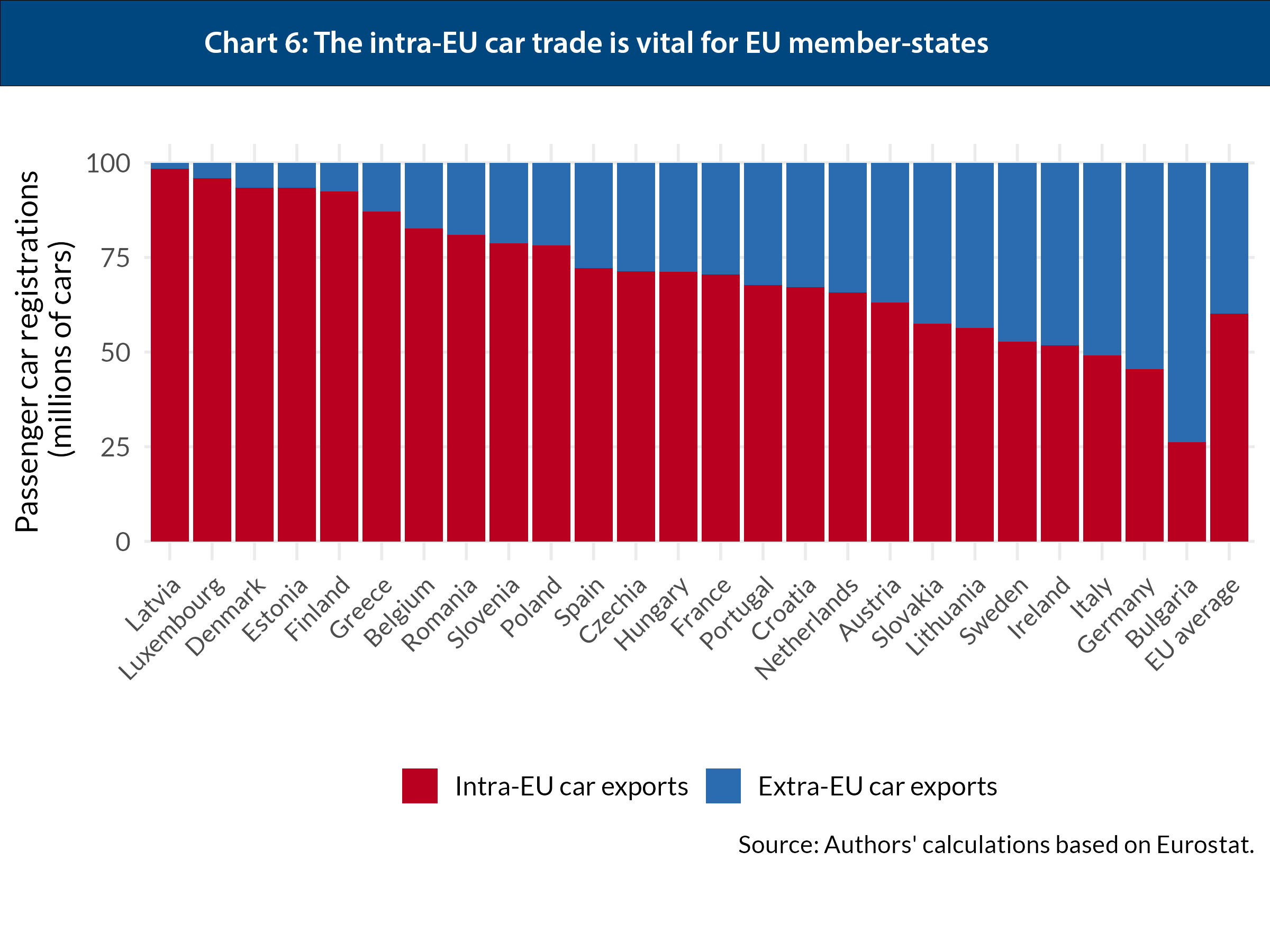

The European market is now also the most reliable buyer for almost everyone (see Chart 6). For major car-producing economies such as Spain and France, the EU market has long been the leading source of demand. The fate of their industries naturally hinges on European consumers. The same now increasingly holds for more export-oriented member-states like Germany and Italy. Given the scale of losses globally (Germany has lost half its net car exports), they cannot rely on their own demand to fill the gap, and need a co-ordinated push from their neighbours.

A common buy-European criterion for EV subsidies: the eco-bonus

There are two policy models for introducing common criteria for European preferences in EU countries’ EV support. The first is a local-content requirement that would limit subsidies to EVs produced – at least in part – within the EU. This is the approach the Biden administration took under the Inflation Reduction Act. France has recently applied a similar measure, introducing from October 2025 an additional €1,000 subsidy for EVs assembled in Europe with a European-made battery. The model is straightforward, applied across all member-states and, if desired, can be extended to trusted third countries.

But its simplicity comes at the price of legality. Local-content requirements are difficult to justify under WTO rules. The Agreement on Subsidies and Countervailing Measures (ASCM) prohibits subsidies contingent on the use of domestic over imported goods. Europe could forge ahead because even if the EU’s trade partners launched a challenge, because it would take time for the WTO in Geneva to rule. But for many member-states, co-ordinating around a measure that openly violates WTO law would be a non-starter. Pressing ahead could cost the EU credibility with trade partners at a moment when it needs allies to defend the multilateral system it relies on, including for car exports.

The wiser course for the EU would be to adopt common qualitative criteria that favour production in Europe and trusted partners – without resorting to blunt local-content rules. France’s eco-bonus system provides a ready-made blueprint for the rest of Europe. It uses a carbon-scoring method to determine which vehicles qualify for support, factoring in emissions from production, transport, raw materials and battery sourcing, as well as the recyclability of components. Eligible cars must also be priced below €47,000 and weigh less than 2.4 tonnes.31 The amount of the bonus, varying between €2,000 and €4,000, decreases as the income of applicants increases.32

France’s eco-bonus scheme covers all EVs produced in the EU, as well as UK-built models below the price threshold. It also includes several South Korean and Japanese cars made by Hyundai, Toyota and Nissan in European facilities, albeit with significant Asian components. By contrast, it effectively filters out Chinese production – reflecting, among other factors, the higher-carbon footprint of Chinese batteries – and some models manufactured in South Korea and Japan.33 NGO Transport & Environment estimated that in 2023, vehicles failing to meet the eco-score accounted for about 26 per cent of EV sales in France, largely Chinese-built cars such as the Dacia Spring, Tesla Model 3 and four SAIC MG models.34

The elegant eco-bonus system effectively steers demand towards EU-produced EVs. It has gone unchallenged at the WTO, and nudges European manufacturers toward low-carbon production. The scheme is not perfect: calculations of lifetime emissions could be made more transparent and aligned with EU regulations such as the battery passport that records the environmental footprint of EU batteries and will be mandatory in 2027; the weighting of different factors could be reconsidered instead of accounting for each components’ actual emissions imprint; emission standards and factor weightings will also need to be adjusted as Chinese production rapidly decarbonises. But such adjustments are feasible: France’s scheme offers an effective and ready-made template for scaling up to EU-wide application.

The key first mover in Europeanising the eco-bonus scheme would need to be Germany – which has the most fiscal space in Europe, and the biggest car sector. The CDU/SPD government is searching for ways to support its struggling industry, and reintroducing EV subsidies would be a vital policy lever for Europe’s most car-centric economy. Berlin should bring back the subsidies it scrapped to comply with the debt brake (in an act of self-flagellation), but update them to ensure that only European- and ally-built cars qualify, to offset China’s market distortions.

Beyond Germany, there is a broader window of opportunity to co-ordinate the introduction of updated eco-bonus conditions across key EU member-states covering most of the European car market. France itself will have to renew its private EV subsidy programme next year; Spain faces a similar deadline; and Italy’s new scheme is tied to Recovery and Resilience Facility funding that expires in 2026. Together, these four countries accounted for around 70 per cent of all new passenger car registrations in the EU in 2024.35

In a second stage, smaller member-states such as the Netherlands or Denmark could follow. The good news is that they can do so without risking a clash with the European Commission. France’s eco-bonus has been in place since 2023 and has repeatedly cleared EU state-aid checks. In the case of private EV purchases, the Commission lacks the legal basis to mandate member-states to include European preferences in their national support schemes. It would need new legislation for that. But it would not block them from applying non-price criteria such as the eco-bonus-style criteria either. So, the door for bottom-up convergence between member-states’ EV schemes with a de facto European and ally preference is wide open.

These policies are fiscally costly but can deliver strong returns by pulling in private demand for Europe’s car sector. France’s eco-bonus’ and its predecessors accounted for 40 per cent of the rise in EV market share until 2021, while US research finds that tax rebates significantly increased EV registrations.36 Research on the IRA suggests that 23-33 per cent of EV purchases were additional, thanks to tax credits, whilst the remainder of the purchases still contributed to fleet electrification.37 The lesson for Europe is clear: well-designed subsidies can unlock private car demand, offset lost exports and boost tax receipts.

In Germany, for example, ECB research suggests that a 15 per cent Chinese EV price advantage cuts German producers’ global market share by around 18 percentage points, highlighting how sensitive demand is to relative prices.38 The reverse also holds: giving EU or German EVs a comparable price edge through consumer subsidies with local production incentives would go a long way toward stabilising domestic production. Shielding even part of its output could yield substantial fiscal returns via higher VAT, corporate and income-tax receipts, given that the car industry brings in over €540 billion in revenue.39 The risk of inaction is a far higher bill later, in lost tax revenues, bailouts and unemployment schemes.

If Europe’s major economies aligned their EV subsidies to counter China’s advantages, the impact would be substantial and lower the overall bill while preserving fair intra-EU competition.

A Franco-German+ grand bargain: extend the eco-bonus to corporate fleets

One challenge for buy-European policies is that European countries specialise in different types of cars. Italian and French manufacturers, for example, have long focused on small and compact models for low- and middle-income households, where affordability is decisive. For them, the priority is defending market share against heavily subsidised, cheaper Chinese EV imports. Germany’s export model, by contrast, centres on high-end cars in the premium segment. As these are increasingly squeezed out of China and the US, the challenge is to secure new sources of European demand at the top of the market.

EV consumer subsidy schemes – including France’s eco-bonus – tend to favour smaller and mid-priced models, since most governments cap eligible prices or make subsidies income-dependent to support lower-income households. Steering producers to scale up in this segment, which accounts for 36 per cent of total EU car registrations, is crucial, as price gaps between ICEs and EVs remain widest here, especially compared with Chinese competitors. But while such schemes benefit producers in France, Italy and Spain, they do less for Germany’s premium manufacturers. An even bigger issue is that private purchases account for only about 40 per cent of new registrations in the EU, leaving much overall demand untapped.

The solution for a European grand bargain lies in the corporate car market – the dominant segment of new sales in Europe. Vehicles bought by companies, leasing firms and manufacturers make up roughly 60 per cent of new registrations.40 Corporate fleets already benefit from generous tax breaks in most member-states – worth about €26 billion per year41 – yet most of this support still goes to ICEs, and fleet electrification lags private markets. By making EV support for corporate fleets conditional on European production through the eco-bonus, member-states could support the electrification of this large swathe of the car market and boost demand.

Extending the eco-bonus to corporate fleets would round out the policy mix. Company cars are skewed toward larger and more luxurious models, for which households provide far lower demand. In European car classifications, B-segment cars are small (for example, the VW Polo), C-segment are medium/compact (such as the VW Golf), and D-segment are large/family cars (for instance the VW Passat). While half of the cars bought by households are in the B segment, they account for less than a third of company car fleets. Instead, 46 per cent of company cars are in the C segment and 22 per cent are even larger. These vehicles are also more expensive – the average non-SUV electric vehicle in the D-segment cost about €52,000 in 2023, compared with €33,000 in the B-segment for small cars.42 Boosting EV demand in the corporate market is therefore especially relevant for producers of medium and premium models such as VW, Mercedes and BMW, while still benefiting firms like Stellantis and Renault.

In sum, harmonised consumer subsidies would channel demand toward smaller, more affordable EVs, where French, Spanish and Italian producers are strongest. By contrast, a Europeanised eco-bonus for corporate fleets would disproportionately benefit higher-end EVs, including German models.

Harmonisation could proceed in two steps. First, large member-states could agree to boost tax incentives for EV uptake in corporate fleets and make them conditional on updated eco-bonus requirements. A joint push by the France, Germany Italy and Spain could then be formalised by embedding such de facto European preference requirements in the EU’s regulation of corporate fleets. The Commission is due to present its first proposal on greening corporate fleets at the end of 2025. If the major member-states align their policies, the Commission could build on that momentum to deliver an ambitious reform – such as introducing a target for the share of EVs in corporate fleets that meet the eco-bonus standard. This could then also provide the legal basis for the Commission to require member-states to link tax support for corporate EVs to eco-bonus criteria via state aid rules.

A global trade strategy using the European eco-bonus

European eco-bonus schemes are in principle open to imports, but new carbon-scoring criteria may end up excluding allied car models – for example, due to emissions from long-distance transport. There is no reason to shield EU producers from fair competition with firms such as Hyundai, Kia or Nissan. Over time, the EU should aim to strike reciprocal deals granting access to its subsidy schemes for allies that offer equivalent access to European products.

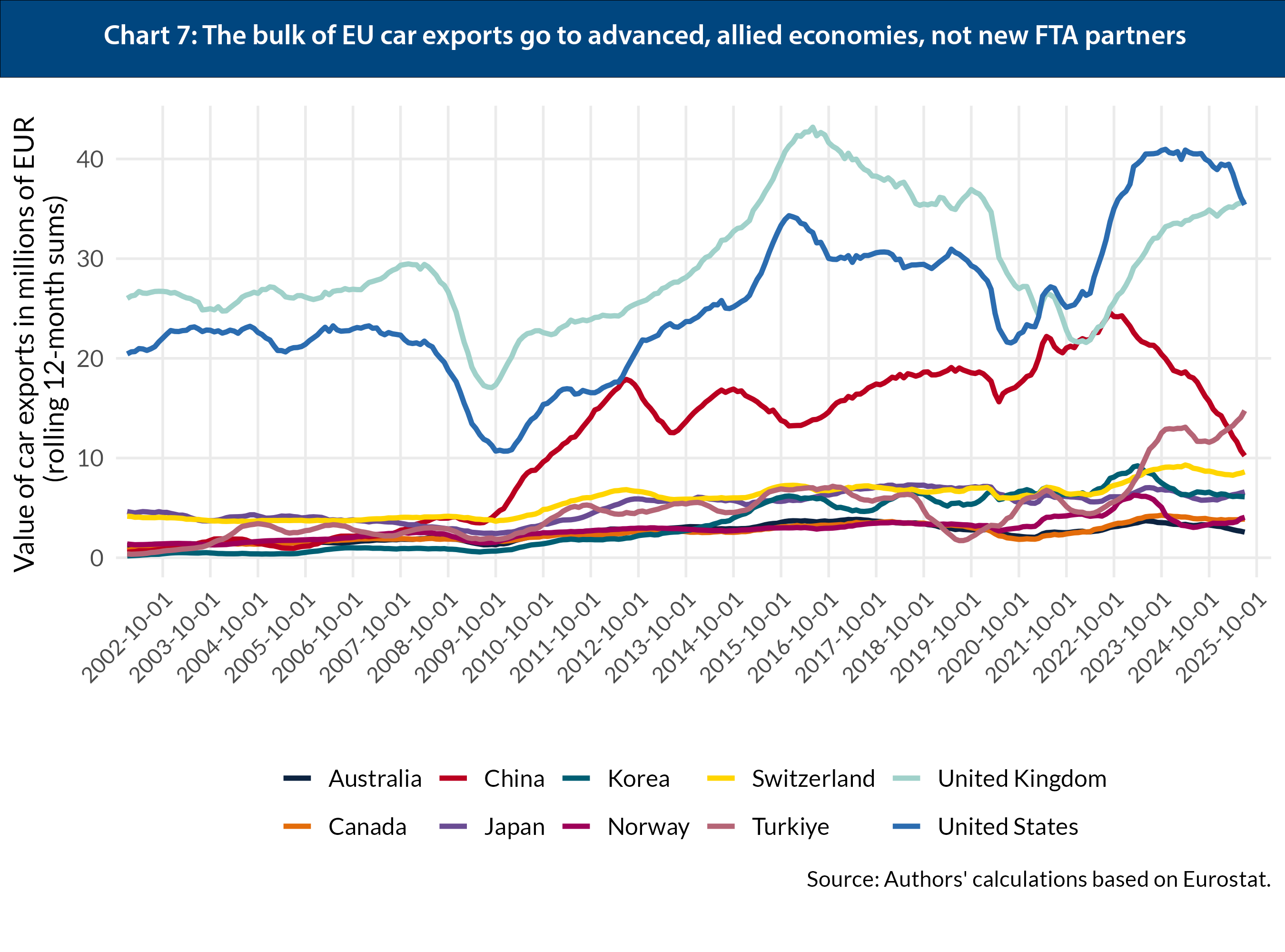

The concentration of EU car exports towards allied economies creates a major opportunity for such reciprocity. A handful of mature, like-minded markets – above all the US, UK, Turkey, Japan, South Korea, Norway and Switzerland – account for around 80 per cent of the EU’s extra-EU car exports (see Chart 7). Europeanising the eco-bonus would provide a platform for a co-ordinated trade strategy with these partners, who share Europe’s concerns about Chinese overcapacity and are similarly looking for ways to counter China’s subsidies.

Take Japan and Korea, where imports of EU built cars remain significant, even if local consumer patriotism is strong. Japan and Korea run sizeable EV and battery subsidy schemes, with hidden or explicit buy national filters that disadvantage European exporters. In Japan, rebates of up to €5,000 are conditioned on technical approvals and after sales networks that favour domestic makers.43 Korea offers consumers over €8,000 in subsidies, but foreign EVs above a set price threshold receive only half – widely seen as a discriminatory measure aimed at EU and US imports.44

Seoul and Tokyo could open their schemes equally to EU cars and batteries in return for access to European incentives, which a Europeanised eco-bonus could cater for. One option would be to grant special bonuses on top of climate scores to carmakers that meet high labour or data safety and privacy standards (benefitting European allies). Such additional bonuses could make sure, for example, that Japanese and Korean models pass the threshold to qualify for EU member-states’ subsidies while China does not. A reciprocity clause would convert subsidies into instruments of co-operative trade strategy – shielding allied markets from Chinese overcapacity while keeping demand open to partners.

A Europeanised eco-bonus could also serve as a basis for closer co-operation with the UK. This summer, Britain – Europe’s second-largest car export market – introduced an EV subsidy scheme based on climate criteria that, much like the French model, is open to cars assembled in Europe but filters out Chinese production.45 Closer alignment between the UK and EU on EV subsidy design would ease compliance for European producers, shield both markets from Chinese overcapacity and build on the renewed UK-EU partnership – without crossing London’s red line on rejoining the single market. Over time, such arrangements could also be extended to Norway and Switzerland, whose EV schemes remain import-neutral, or to Turkey, which has already introduced tariffs on Chinese EV imports.

Such an approach might also have eased EU concerns about the discriminatory dimensions of the Biden administration’s Inflation Reduction Act. But with Washington now phasing out EV credits, raising tariffs and rolling back the IRA, reciprocal subsidy access is off the table – at least for the moment.

Reciprocal EV subsidy arrangements will do far more for European car exports than new free trade agreements. The EU is right to pursue trade deals with Mercosur, Indonesia and India to prevent protectionist spirals and secure access to critical inputs such as rare earths, which China is weaponising. But car exports to these markets remain marginal and barely growing. Countries like India and Indonesia may one day become important sources of demand, but that is still years away. Europe will also struggle to compete with China’s rock-bottom prices in these lower-income markets.

Conclusion

Europe’s most important industry is faced with a perfect storm. China’s overcapacity and the erosion of global export markets, combined with the disappearance of the offset from the US market, have created a demand shock that Europe cannot ignore. Europe’s car sector is not doomed, but flip-flopping around the 2035 phase-out of ICEs is a waste of time, and not the answer to the sector’s woes.

The decisive lever for responding lies at home: Europe’s vast internal market. A coherent framework for a European preference in EV subsidies would give carmakers scale and help safeguard employment – without ossifying outdated structures. The most obvious way forward is to Europeanise the French eco-bonus scheme, which effectively steers demand to EU production, and avoids further subsidising Chinese vehicles.

France’s scheme is an off-the-shelf blueprint that Germany can improve and deploy for its new EV subsidies, to inspire other member-states, and create demand for the affordable compact EV models that households tend to buy. If large member-states extend the eco-bonus criteria to corporate fleets this will also create demand in the premium segment.

There is a fiscal cost to EV consumer subsidies, but the point is to ensure that more of this spending supports European production. Better co-ordination of existing programmes would already help, although a genuine demand push will require member-states to spend more. The alternative would be far costlier: doing nothing now will only raise the price of future bailouts, while a patchwork of national schemes drains treasuries without generating the scale needed. Stoking European demand for European EVs will not fix every structural issue, but without it, challenges from batteries to digitalisation become harder to address.

These policies echo President Biden’s signature bills, designed to reverse America’s industrial decline and curb its dependence on China. Ironically, it is now the EU, with its much larger car industry, twice as many industrial workers, and a lead in electric vehicles, that needs such an industrial awakening even more urgently. Europe has far more at stake and if it acts together, a better chance to succeed.

2 European Commission, ‘Productivity trends using key national accounts indicators’, March 2025.

3 Sander Tordoir, ‘Heavy Manufacturing is Europe’s Trump Card’, Foreign Policy, March 2025.

4 Sander Tordoir and Brad Setser, ‘How German industry can survive the second China shock’, CER policy brief, January 2025.

5 International Energy Agency, ‘Global EV outlook 2025’, March 2025.

6 Geraldine Herbert, ‘Will EVs ever reach price parity with petrol and diesel cars and if so, when?’, Euronews, October 27th 2024.

7 Sander Tordoir and Elisabetta Cornago, ‘How to build and fund a better EU green industrial policy’, CER policy brief, February 2025.

8 Frank Bickenbach, Dirk Dohse, Rolf Langhammer and Wan-Hsin Liu, ‘EU concerns about Chinese subsidies: What the evidence suggests’, Intereconomics – Review of European Economic Policy, August 2024; Jost Wübbeke, Mirjam Meissner, Max Zenglein, Jaqueline Ives and Björn Conrad, ‘Made in China 2025: The making of a high-tech superpower and consequences for industrial countries’, Mercator Institute for China Studies, December 2016.

9 Brad Setser, ‘Will China take over the global auto industry?’, Council on Foreign Relations, December 2024.

10 Daniel Garcia-Macia, Siddharth Kothari and Yifan Tao, ‘Industrial policy in China: quantification and impact on misallocation’, IMF, August 2025.

11 Sébastien Jean, Isabelle Méjean, and Moritz Schularick, ‘EU-China Economic Relations and Global Imbalances’ Joint statement of the Franco-German Council of Economic Experts, August 2025.

12 Gregor Sebastian, ‘The Hangover: Foreign Carmakers’ China Strategies’, Rhodium Group, September 2025.

13 Chinascope, ‘China’s top 10 automobile export markets in first half of 2025’, August 15th 2025.

14 Transport & environment, ‘One in four EVs sold in Europe this year will be made in China’, March 2024.

15 Vladislav Vortnikov, ‘Global supply chain adapts to booming sales of Chinese vehicles,’ Automotive Logistics, August 5th 2025.

16 Daniel Ren, ‘China’s BYD expands car-carrier fleet to bolster EV exports amid furious domestic competition’, South China Morning Post, June 24th 2025.

17 Karel Axelton, ‘The most popular cars to lease’, Experian, November 4th 2024.

18 Chad Bown, ‘How the United States solved South Korea’s problems with electric vehicle subsidies under the Inflation Reduction Act’, Peterson Institute for International Economics, July 2023.

19 Acea, ‘Economic and market report: global and EU auto industry – first half of 2025’, September 2025.

20 ‘German car exports to the U.S. slide in April, May as tariffs hit’, Reuters, July 3rd 2025.

21 Duty drawback is permitted under the legal statutes used by the Trump administration to impose the reciprocal (IEEPA) tariffs, but excluded under the sectoral (Section 232) tariffs. The legality of the former is currently under Supreme Court review.

22 Transport & Environment, ‘EV progress report’, September 2025.

23 Jannik Jansen, ‘Europe’s car industry in transition: stuck in neutral or shifting into gear?’, Jacques Delors Centre, July 2025.

24 Gazzetta Ufficiale, ‘Decreto 8 agosto 2025, criteri e modalità per la concessione di incentivi a fondo perduto’.

25 European Alternative Fuels Observatory, ‘Portugal Launches 2025 Incentive Programmes to Boost Zero-Emission Mobility,’ March 31st 2025.

26 ‘Electric car subsidy applications open until year’s end’, eKathimerini, August 2025.

27 European Alternative Fuels Observatory, ‘France: Incentives and Legislation’, April 2025.

28 Mario Draghi, ‘The future of EU competitiveness’, European Commission, September 2024.

29 Federico Fubini, ‘Cacciatori e prede’, Corriere Della Sera, February 14th 2025.

30 Observatory of Economic Complexity (OECD), ‘Engine Parts’.

31 ADEME, ‘Score environnemental du véhicule’, July 2025.

32 Service-Public.fr, ‘Bonus écologique pour une voiture’, July 1st 2025.

33 S&P Global Mobility, ‘BriefCASE: Climate politics – France’s carbon footprint incentive stirs debate on global EV supply chains’, March 2024.

34 Lucien Mathieu, ‘France’s eco-bonus shows how we can promote cleaner made-in-Europe EVs’, Transport & Environment, December 2023.

35 Authors’ calculation based on Eurostat, October 2025.

36 Haut-commissariat à la strategie et au plan, ‘Is support for the development of electric vehicles adequate?’, June 2024; and Nafisa Syed, ‘Rebate incentives boost BEV adoption and can be cost-effective when paired with a low-carbon electricity grid, new research finds’, MIT energy initiative, January 2020.

37 Hunt Allcott, Reigner Kane, Maximilian Maydanchik, Joseph Shapiro and Felix Tintelnot, ‘The Effects of “Buy American”: Electric Vehicles and the Inflation Reduction Act’, National Bureau of Economic Research, December 2024.

38 Maria-Grazia Attinasi, Lukas Boeckelmann, Bernardo de Castro Martins and Baptiste Meunier, ‘Box 2: A model-based assessment of the spillovers of Chinese subsidies to electric vehicles’, ECB Economic Bulletin, Issue 5/2024.

39 Handelsblatt, ‘Was bringt der Autogipfel beim Kanzler’, October 9th 2025.

40 Michelle Monteforte, Uwe Tietge and Sonsoles Diaz, ‘European market monitor: cars and vans 2024’, international council on clean transportation, February 2025.

41 Transport & Environment, ‘Unveiling Europe’s corporate car problem: how the EU can unlock the potential of company fleets’, June 2024.

42 Transport & environment, ‘Stuck in the fossil age: are car leasing companies in the EU green leaders or greenwashing?’, October 2023.

43 Japan METI, ‘Subsidies upgraded for the purchase of clean energy vehicles towards the realization of GX in the automobile sector’, July 2024.

44 Yong-Hee Kwak and Il-Gue Kim, ‘Korea’s new EV subsidy plan favours Hyundai over Tesla, other imports’, Korea Economic Daily, Feburary 3rd 2023.

45 Pritti Mistry, ‘Electric cars eligible for £3,750 discount announced’, BBC, August 28th 2025. Peterson Institute for International Economics, July 2023. June 24th 2025.

Sander Tordoir is chief economist at the Centre for European Reform, Dr Nils Redeker is acting co-director at the Jacques Delors Centre and Lucas Guttenberg is director of the Europe Programme at the Bertelsmann Stiftung.

Download full publication