China and Europe: Can the EU and the UK find a shared strategy?

- The EU, the UK and several European countries have strategies or policies to deal with China. But China’s rise, its support for Russia’s war effort in Ukraine and the unreliability of Trump’s US as an economic and security partner have sharpened the dilemmas in European policy towards China.

- Trade between China and the EU and UK combined amounts to more than one-third of total global trade. The balance is heavily in China’s favour, and its surplus is widening. Repeated EU and UK expressions of concern have achieved nothing. The problem for Europe is not just the size of its trade deficit, but the wide range of critical goods for which it is largely or entirely dependent on China. China’s industrial over-production is driving European producers out of their domestic markets and their export markets.

- In technology, China has moved from being an imitator to an innovator, and leads Europe in many areas seen as critical to future economic growth and achieving net zero. Through the policy of ‘military-civil fusion’, Xi Jinping is seeking to ensure that the military sector can benefit from civilian technological advances. Allowing China to acquire defence-related knowledge in Europe is worrying because China is helping Russia in its war of aggression against Ukraine, and because it threatens Europe’s democratic partners in the Indo-Pacific region. China is also using the influence it derives from its trade and investment to promote its model of techno-authoritarianism, with some success in the global south and even in Europe

- Europe has to manage its approach to China’s geopolitical challenge in the context of an erratic US administration that is sometimes tough on China but sometimes undercuts its own restrictions on technology transfer, and may intend to pull back from providing security for its European and Indo-Pacific partners.

- European ‘strategies’ for dealing with China and the Indo-Pacific region are vague about ends and even vaguer about means. Europeans want to maintain as good relations as possible with China, while mitigating the risks that it poses. They do not want to discuss what it means for China to be a systemic rival, or how to promote European models of governance against China’s alternative.

- Europeans would benefit from having co-ordinated policies towards China. The starting point should be an improved understanding of what China is doing. European governments should stop thinking that Xi Jinping will eventually level the playing field or open his markets to European competition.

- Both the EU and UK would benefit from regular and intensive dialogue and practical policy co-ordination in relation to China. There are a wide range of topics that could be included in the agenda, including economic security, the protection of sensitive technologies, Chinese cultural and information activities in Europe, and Europe’s broader geopolitical approach to China and the Indo-Pacific region.

- Engagement with China in some areas, such as combatting climate change, is desirable and necessary, but Europeans should not be naïve. The UK and EU both shy away from labelling China as a hostile state, still less an enemy. But China has built up its power with a view to pursuing ends that will in many cases not be aligned with European values or interests.

- The EU is right to say that China is a systemic rival. The UK says that “the challenge of competition from China has potentially huge consequences for the lives of British citizens” and speaks of the need for alignment with G7 and other partners. But neither the EU nor the UK have drawn the policy consequences from their analysis. Europeans must now work to ensure that the European liberal, democratic model of governance shows its superiority to the authoritarian model promoted by Xi Jinping.

In July 2023, the Centre for European Reform and the Konrad-Adenauer-Stiftung UK and Ireland Office published a policy brief, ‘Building UK-EU bridges: Convergent China policies?’, that looked at the dilemmas that China posed for both the UK and the EU. These included China’s importance as a market and as a near-monopoly supplier of some goods; its central role in combating global climate change; its support for Russia in its war of aggression against Ukraine; and its rivalry with the US, Europe’s most important security provider.

In the intervening two years Germany has adopted a ‘Strategy on China’; France has published ‘France’s Indo-Pacific Strategy’, both reflecting the EU’s 2019 ‘Strategic Outlook’ on EU-China relations and its 2021 “EU strategy for co-operation in the Indo-Pacific’; and the UK has conducted a ‘China audit’. The China audit has not been published, because of its sensitivity, and the UK has not set out publicly a unified strategy for dealing either with China or the Indo-Pacific region, although both are referenced in other documents including the UK National Security Strategy.

The EU and UK have also identified the Indo-Pacific region as one of the priority areas for foreign policy consultations between them.1

If anything, since 2023 the dilemmas around the China policies of the EU and European states have sharpened: China has become more dominant as a supplier of some critical goods and technologies; Chinese support for Russia’s military industrial sector has increased; Donald Trump’s tariff policies have had knock-on effects on trade between China and Europe; and the US has been re-evaluating its role as a provider of security both in Europe and in the Asia-Pacific region.

This policy brief looks at the state of China’s relations with the EU and the UK. It compares what the UK, the EU, France and Germany are now saying about their relations with China. And it makes recommendations for improved European co-ordination of policy towards China and its neighbours.

The state of relations between China and Europe

The then UK foreign secretary David Lammy, in summarising the results of the China audit for the House of Commons in June 2025, described the UK’s relationship with China as “our most complex bilateral relationship”, and said that China’s global role did not fit into simple stereotypes – pointing to the fact that China is both the world’s biggest emitter of greenhouse gases and its biggest producer of renewables as an example.2 The EU’s mantra for describing its relationship with Beijing is that “China is, simultaneously, in different policy areas, a cooperation partner with whom the EU has closely aligned objectives, a negotiating partner with whom the EU needs to find a balance of interests, an economic competitor in the pursuit of technological leadership, and a systemic rival promoting alternative models of governance.”3 Like most complex international relationships, EU and UK relations with China are made up of a number of simpler components. This policy brief will concentrate on three of the most important: trade, technology and geopolitics.

Trade

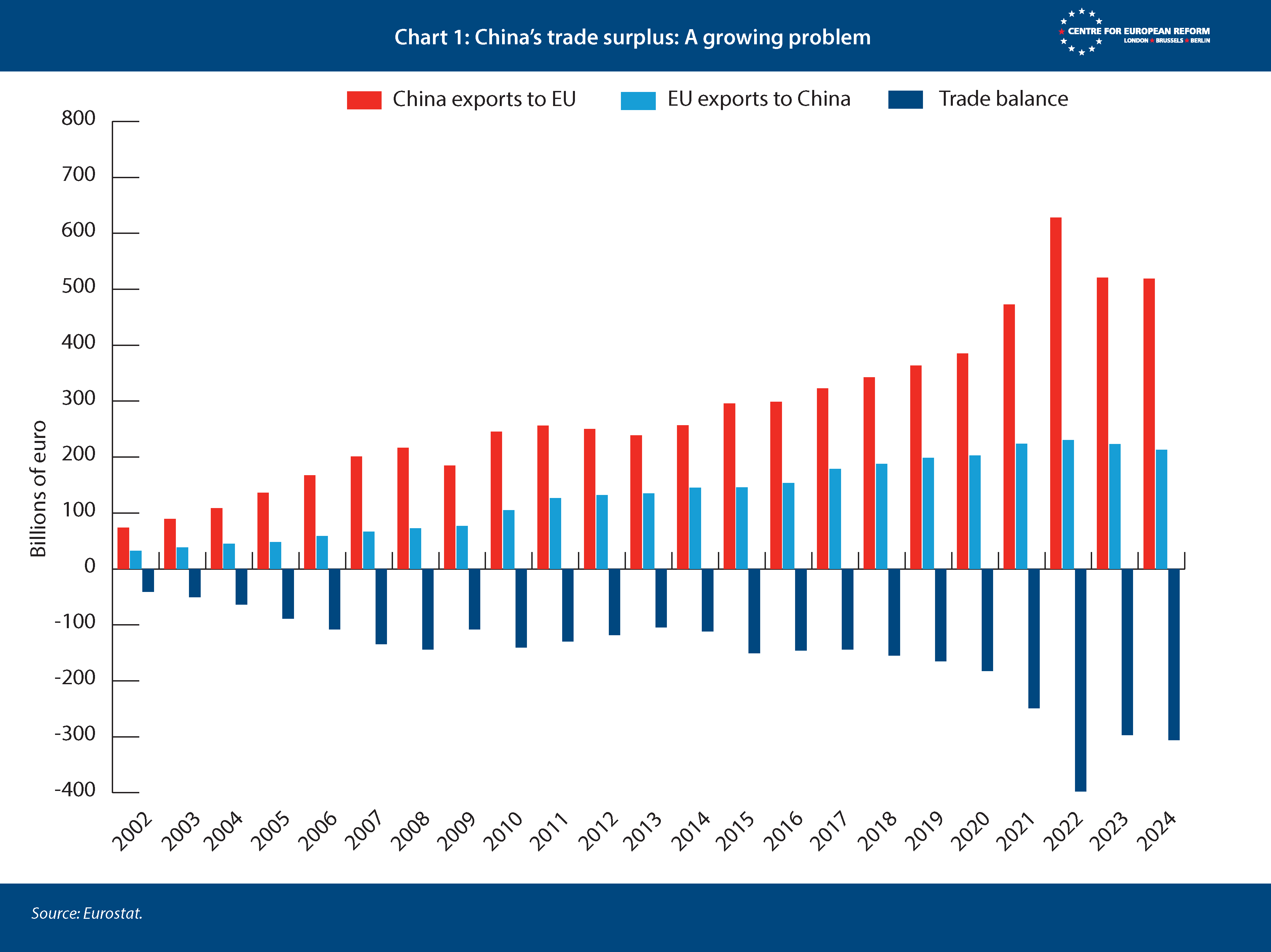

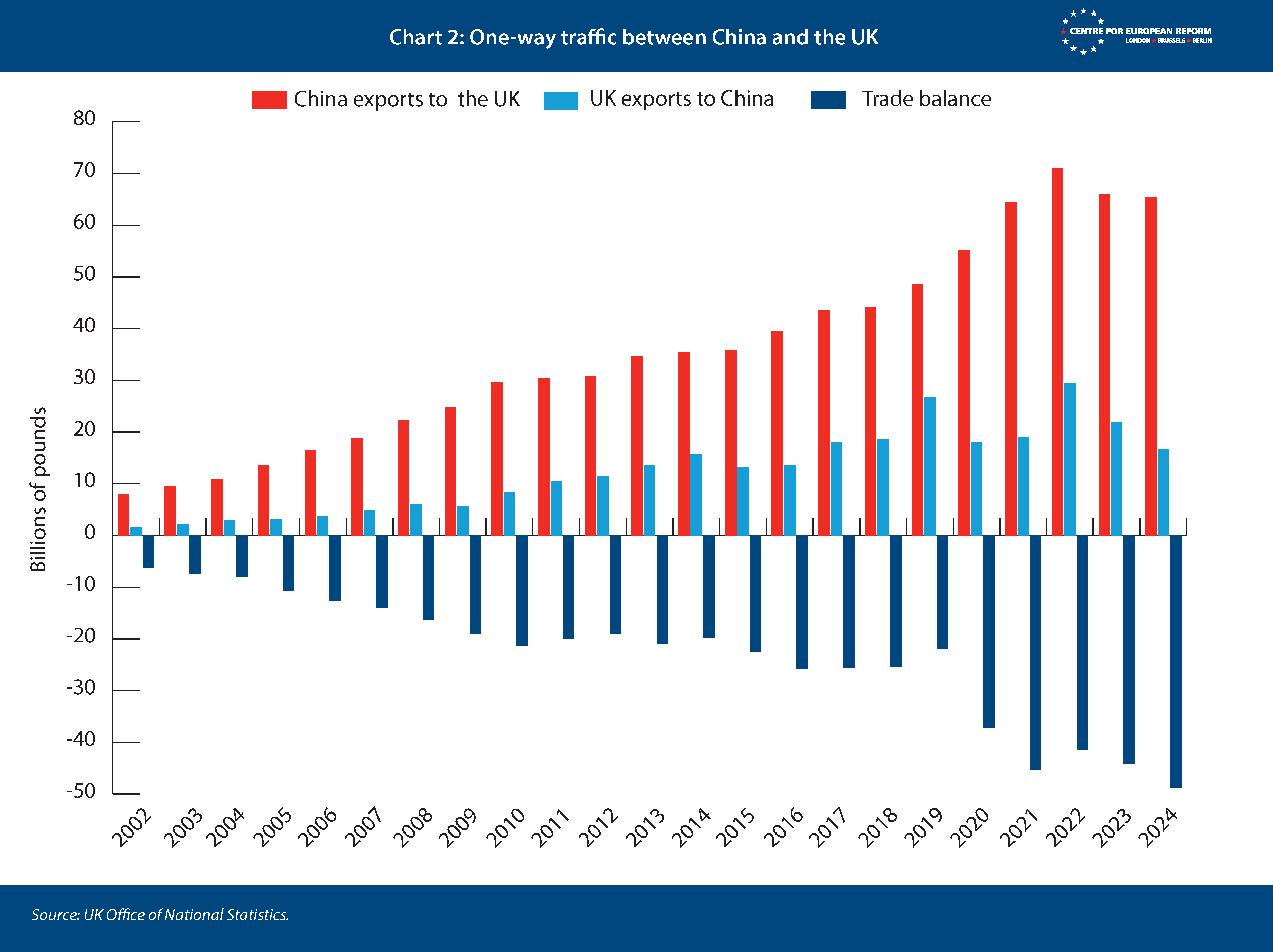

According to EU data, trade between China and the EU accounted for almost 30 per cent of total global trade in goods and services in 2024.4 Trade between China and the UK made up around another 4 per cent.5 In goods, the balance of trade is consistently and overwhelmingly in China’s favour, by €519 billion to €213.2 billion in 2024 in the case of the EU, and by £65.4 billion to £16.7 billion in the case of the UK. Both the EU and the UK run surpluses in services trade, but the figures involved are much smaller: the EU exported €67.3 billion and imported €45.5 billion, and the UK exported £13 billion and imported £3.3 billion. China is the UK’s second largest source of imports (after Germany), and the EU’s largest source of imports.

The EU has been expressing concerns about China’s trade surplus since before the global financial crisis began in 2008: José Sócrates, the Portuguese prime minister who held the rotating presidency of the EU in 2007, said after an EU-China summit that the surplus was “at unsustainable levels right now”.6 Its complaints have not achieved much. As Chart 1 shows, China’s trade surplus in 2024 was more than twice as much as it was when Sócrates made his comment. At the 2025 EU-China summit in Beijing, “the EU raised its concerns about ongoing systemic distortions and growing manufacturing overcapacity, both of which exacerbate an uneven playing field”.7

The UK’s trade with China shows a similar but more extreme pattern (see Chart 2). From 2007 to 2024, the UK’s goods trade deficit with China more than tripled, with a notable increase from 2020 onwards. Like the EU, the current UK government has also complained about the trade deficit. The UK’s business and trade secretary, Peter Kyle, visited China on September 10th-11th 2025 for the UK-China Joint Economic and Trade Commission; the Department for Business and Trade’s fact sheet after the visit said “He discussed challenges in the bilateral relationship with counterparts including level playing-field issues that undermine fair competition for UK business.”8

Trade deficits are not always a problem – the US has maintained one for more than 40 years, including with the EU. But China’s economic policy choices – essentially, to invest rather than consume, and then export surplus production – have resulted in immense industrial over-capacity. In 2024, a report by the Rhodium Group, a research company focusing on China, assessed that “Chinese companies, across a wide range of sectors, now produce far more than domestic consumption can absorb”.9 This surplus makes itself felt not only in relation to China's exports to Europe, but in the impact that it has on European exports to third countries, including China itself. Both EU and UK goods exports to China have fallen over the last three years. European manufacturers are increasingly losing out to lower-cost Chinese producers, both in Europe and in export markets. A January 2025 CER policy brief looked at the automotive sector, and found that while in 2019, China was a net importer of passenger cars, by 2023 it was the world’s largest net exporter.10

The problem the EU is facing is not just Chinese exports, but also that China’s market is not as open as its own. Tariffs are relatively low (according to the World Bank, China’s weighted mean tariff rate in 2022 was 2.2 per cent, compared with 1.3 per cent for the EU). The market is distorted, however, by the Chinese Communist Party’s objective of increasing self-sufficiency through programmes such as ‘Made in China 2025’ and the ‘dual-circulation economy’ – which seeks to satisfy domestic demand with domestic production, while increasing exports.

The market is distorted by the Chinese Communist Party’s objective of increasing self-sufficiency.

Moreover, this shift is creating new and harmful strategic dependencies. Both the EU and UK have become highly dependent on China for imports of a wide range of critical raw materials, chemicals and manufactured goods, including those needed for the energy transition. A recent report by the Bertelsmann Stiftung examining EU and UK import dependency from 2021-2023 identified 1153 goods for which the EU had no easy domestic substitute, a small number of external suppliers and one dominant supplier accounting for 50 per cent or more of imports. Of these, China was the dominant supplier for 554 or 48 per cent. In the case of the UK, there were 1068 goods meeting the criteria for dependency; China was supplier of 300, or 28 per cent (the EU was the dominant supplier of 41 per cent).11

Not all of these goods can be called ‘strategic’ (for both the EU and the UK the list includes furniture, for example). But some certainly are. The EU relies heavily on China for common and lower-cost active pharmaceutical ingredients (APIs) including painkillers like paracetamol and ibuprofen and many common antibiotics – around 45 per cent of imported APIs, by volume, came from China in 2019.12 That may underestimate the EU’s dependency on China, since India, another major source of APIs (around 10 per cent in 2019) itself depends on China for APIs and some ‘key starter materials’.13

A 2022 study highlighted the UK’s dependency on China for other basic medical supplies – 90 per cent of surgical face-masks and 69 per cent of plastic gloves were imported from China, for example.14

China also dominates global production of rare earth elements (REEs) and compounds, vital for electronic components, including smartphones, LEDs, batteries and magnets for wind turbines. The EU is 100 per cent import-dependent for its REEs; over the period 2016-2020 China supplied 80 per cent of the group of elements known as light REEs and 64 per cent of heavy REEs. The UK is equally dependent on Chinese imports. China is not only a supplier of REEs; it is also a leading and in some cases almost a monopoly supplier to the EU of components that incorporate REEs, such as rare-earth magnets – 98 per cent of which were imported from China, according to a 2021 report for the European Raw Materials Alliance (a body set up by the EU that includes all stakeholders with an interest in the issue, from mining firms and industrial consumers to non-governmental organisations).15

Dependency on China for strategic goods is harmful, not least because China has shown that it is willing and able to weaponise these dependencies. Export controls on REEs are being used to create leverage in trade negotiations with both the US and the EU. Previous controls were tightened on October 9th: China introduced rules forcing foreign companies to seek a licence to export magnets containing as little as 0.1 per cent of rare earth materials from China, or that were produced using Chinese extraction methods, refining or magnet-manufacturing technology, with a presumption that exports to military users would be banned.16

Such export restrictions affecting Europe have caused considerable disruption and risk for European EV manufacturers and other sectors over the last year, with the clear intention of putting pressure on the EU in ongoing trade disputes. They also have the potential to change the situation on the battlefield in Ukraine, if China uses the new licensing regime to prevent Ukraine buying drones or the components for them – something which it has not yet done, despite its close relationship with Russia.

Technology

The new restrictions underline the risks not just to European prosperity but to European security from China’s growing dominance in a wide range of technologies. Europe’s great fear used to be that China would steal its intellectual property. The rising danger is that Beijing will deny Europe access to Chinese technology, including in areas vital for advanced defence equipment – batteries, advanced materials, sensors, electric motors and so on.

In civilian sectors, China has already become an innovator as well as an imitator. In 2023, China was responsible for 1.68 million patent applications – almost half the global total of 3.55 million. European patent offices collectively received just over 10 per cent of the global total. China was responsible for more than half of industrial design applications (Europe – just under a quarter) and more than half of plant variety applications (Europe – just under a quarter, compared with 46 per cent in 2013).17

The rising danger is that Beijing will deny Europe access to Chinese technology.

Despite the progress it has made, China only ranks tenth in the World Intellectual Property Organisation’s (WIPO) ‘Global Innovation Index’. Six European countries – Switzerland (first overall), Sweden, the UK, Finland, the Netherlands and Denmark – are ahead of it, together with the US, South Korea and Singapore.18 But WIPO also looks at ‘innovation clusters’ – areas where universities, technology firms, inventors and venture capitalists are concentrated. Europe as a whole has 29 such clusters in the top 100, including four in the UK, though only one (London) in the top ten; China has 24, including three in the top ten – an indicator of a growing capacity to innovate.

China is ahead of Europe in many areas seen as critical to future economic growth and achieving the goal of net zero emissions, as well as to defence and security. The Australian Strategic Policy Institute’s (ASPI) Critical Technology Tracker looked at 64 technologies, and ranked countries (or groups of countries, in the case of the EU) by their share of high impact research outputs over the 2019-2023 period.19 China led in 56; the EU led in two.

In a few areas, for example quantum communication, the EU and UK combined could previously have got significantly closer to matching China. But China’s huge investments in research and development (R&D) and its output of STEM graduates is increasing the gap: as a percentage of GDP, China’s R&D spending overtook the EU’s in 2019. In PPP terms, in 2022 China spent $718 billion on R&D; the EU spent $496 billion, and the UK $103 billion. Moreover, China’s spending is increasing by 8 per cent a year or more; EU and UK spending is increasing by less than 2 per cent per year.20 China has many more students studying STEM subjects; in 2020, 41 per cent of graduates from Chinese universities – 3.57 million people – were STEM graduates. In Europe, Germany led the way with 36 per cent of all graduates in STEM subjects – 216,000. For the UK, the figures were 192,000 or 23 per cent – though up to 58,000 of those were foreign students.21

ASPI also identified 21 technologies in which there was a risk of China obtaining a monopoly, because of the concentration of expertise there. These included areas such as advanced optical communications (for instance fibre optics), advanced composite materials, electric batteries and electronic warfare.

China’s advances in civilian technologies are a challenge to European industries, but may be a boon to Europe’s efforts to achieve net zero. It is much harder to see an upside in the parallel advances China is making in military technology. Chinese leaders have talked for more than 20 years about ‘military-civil fusion’ – a policy designed to ensure that the military sector can benefit from civilian technological advances, and vice versa. Xi is keen to ensure that China’s military build-up takes full advantage of ‘new quality productive forces’ – an umbrella term for technology and innovation; their application to existing, emerging and future industries; and the development of supply chains that are outside the control of foreign powers.22 At a meeting with the armed forces and police, he said that the armed forces must “promote the efficient integration of new-quality productive forces and new-quality combat forces”.23

An important feature of China’s military development is its military-technical co-operation with Russia (which predates Russia’s full-scale attack on Ukraine). So far, most of the technology transfer seems to have been from Russia to China, in areas including air defence and submarine technology. Some of it has involved China reverse-engineering items, including fighter aircraft, purchased from Russia.24 China has so far been cautious about supplying weapons or weapons technology to Russia, perhaps because of the risk of European and US sanctions. But the combination of indigenous technological advances and imported know-how is a threat to China’s neighbours, many of whom are also important economic and diplomatic partners of the EU and the UK.

European governments should do more to try to prevent China from acquiring militarily relevant technology from Europe.

European governments may not be able to do much about China’s domestic R&D strengths or its co-operation with Russia, but they should do more to try to prevent China from acquiring militarily relevant technology from Europe. China uses ‘traditional’ commercial espionage and cyber attacks to get hold of sensitive information, but ASPI’s research also highlighted the number of Chinese researchers of key technologies with potentially military applications who study in the West and develop or acquire intellectual property there.

Many of the hundreds of thousands of Chinese students studying in Europe (98,000 in the UK alone in 2023) are merely trying to get a different or better education by coming to Europe.25 Some may even be hoping to enjoy more freedoms, political or personal, than the Chinese Communist Party offers them at home. But in some cases, their motives may be less straightforward. A 2020 study by the Henry Jackson Society identified over 500 Chinese post-graduates at British universities studying ‘high risk’ subjects (materials science, physics (including nuclear physics), mechanical engineering, aeronautical and aerospace engineering, chemical, process and energy engineering, minerals technology and materials technology) who had also graduated from one of China’s ‘Seven Sons’ defence universities or from another university or research institute classified as ‘very high risk’ because of its close ties to the Chinese military or security services.26 Analysis carried out by the Central European Institute of Asian Studies in 2025 concluded that of 1518 relationships between British universities and Chinese research institutes and other entities, almost a third were linked to the Chinese military. More than two-thirds of STEM research projects linking Chinese entities and the research-intensive Russell Group universities in the UK involved high-risk or very high-risk Chinese universities and institutes.27

A joint investigation by a consortium of European media outlets found similar reasons for concern in other European countries. In the Netherlands, for example, RTL Nieuws and Follow the Money (an investigative media group) identified more than 90 graduates of Chinese military-linked universities who had gone on to get doctorates at Dutch universities; while studying in the Netherlands, one told a Chinese newspaper that the military had sent him to study abroad so that he would be able “to take on the heavy task of strengthening and modernising the army”.28 Almost three-quarters of the 483 ties between French universities and Chinese entities have a connection to the Chinese military.29 The EU itself has even funded at least 14 projects involving European institutions partnering with researchers from the ‘Seven Sons’ – mostly in the relatively uncontroversial area of decarbonisation, but some also covering potentially more militarily relevant subjects such as advanced electronics, advanced electric motors for transport and safe maritime operations in the Arctic.30

Geopolitics

Perhaps there would be less reason to worry about China’s acquisition of military relevant technology and expertise if the international situation were not so fraught. The UK and the EU both have to keep four things in mind as they formulate their policies towards China: Beijing’s support for Russia, the impact of China’s growing military power on European partners in the Indo-Pacific region, China’s growing economic and political influence in the global south and even in Europe itself, and Washington’s hostility to China.

Relations between Beijing and Moscow have not always been good (the Soviet Union and China skirmished over their border in 1969). Their long-term aims may not coincide: China, as a major trading power, benefits from the existing international order, even if it seeks a bigger role in it, while Russia sees more to gain from disrupting the current international system and exploiting the resulting chaos. But in the short term their interests are largely aligned: each is reassured that the other poses no threat to its interests, enabling each to pursue its own objectives – in China’s case, to increase its influence in its region, globally and in multilateral forums, at the expense of the US and American allies; and in Russia’s case, to rebuild its power in Europe, starting with the subjugation of Ukraine.

China has helped to keep the Russian economy afloat, filling the gap left by Western sanctions.

China’s rhetoric on the war in Ukraine is generally cautious, and seeks to give the impression of neutrality – though the Chinese foreign minister, Wang Yi, reportedly told EU High Representative for Foreign Affairs and Security Policy Kaja Kallas in July 2025 that China did not want to see a Russian loss in Ukraine because it feared the United States would then shift its whole focus to Beijing.31 China has not recognised Russia’s annexation of Crimea, or its claims to have annexed other Ukrainian regions. Xi set out four relatively uncontroversial principles for restoring peace during a 2024 visit to China by then German Chancellor Olaf Scholz: “First, we should prioritise the upholding of peace and stability and refrain from seeking selfish gains. Second, we should cool down the situation and not add fuel to the fire. Third, we need to create conditions for the restoration of peace and refrain from further exacerbating tensions. Fourth, we should reduce the negative impact on the world economy and refrain from undermining the stability of global industrial and supply chains.”32 Yi met his Ukrainian counterpart, Andrii Sybiha, in the margins of the UN General Assembly in New York in September 2025, and talked of the two countries’ “traditional friendship” and “strategic partnership”, as well as the fact that China had provided a number of packages of humanitarian aid to Ukraine and was ready to provide more.33

Beyond the diplomatic courtesies, however, China has been significantly more helpful to Russia than to Ukraine – and much more helpful than it was after the annexation of Crimea in 2014, when Chinese exports to Russia fell sharply. From 2021-2024, despite the full-scale invasion of Ukraine in 2022, Chinese exports to Russia have increased by more than 70 per cent.34 To a large extent, China has helped to keep the Russian economy afloat, filling the gap left by Western sanctions and the withdrawal of many Western companies from the Russian market, for example by dramatically increasing its car exports to Russia.

China has helped Russia’s war effort more directly, by supplying components and machinery needed to build weapons and munitions. Estimates vary, but the EU’s sanctions envoy, David O’Sullivan, told Polish broadcaster TVP that about 80 per cent of the imported components that Russia uses in weapons production come via China.35 According to Ukrainian reports, China supplies drone components including electronics, cameras, engines, antennas and navigation modules – some Chinese, some Western items which China re-exports to Russia.36 There is considerable evidence of Chinese firms supplying Russia with equipment such as body armour, helmets and thermal sights – non-lethal, but still a significant contribution to the war effort.37 According to Politico’s research, though China continues to supply some equipment to Ukraine, such as quadcopter drones and thermal optics, quantities have barely risen since the start of the war, while deliveries to Russia have multiplied – in the case of thermal optics, from $16 million in 2021 to $105 million in 2023.

China has also contributed to Russia’s revenues during the war. It has been an important buyer of Russian oil, and the volume has increased compared with January 2022, from around 115,000 tonnes a day to around 155,000 tonnes. But there has not been the wholesale diversion of oil from Europe to China that has been seen in the case of India, which has gone from importing 4,000 tonnes a day to 192,000 tonnes a day.38 China seems to be taking a largely pragmatic approach to energy purchases from Russia, while maintaining its longstanding policy of not becoming too dependent on any one supplier: Russia accounted for around 19 per cent of China’s oil imports in 2024. Russia has also become an increasingly important gas supplier: in 2020, only 6.7 per cent of China’s total gas imports (liquefied natural gas and piped gas) came from Russia, but by 2024 the figure had risen to 17.6 per cent.39

Apart from security on its long border with Russia (which is important, not least in allowing China to focus the attention of its military on Taiwan and the South China Sea), what does China get for its help? It seems to be getting sensitive military technology in areas such as undersea warfare, for one thing.40 Russia has reportedly also agreed to supply China with equipment and training needed to mount an airborne assault on Taiwan.41

China is dramatically increasing its military capability, including the ability to project power well beyond its immediate neighbourhood. One illustration: in 2005 the Chinese navy had 221 ships; by 2030, based on current rates of ship-building, it is forecast to have 435 ships – well ahead of the US navy, with a forecast 294 ships.42 Its nuclear warhead stockpile has more than doubled since 2019. Its air force has grown and modernised. Russia’s contribution to China’s military strength may not be decisive, but it is significant.

In 2005 the Chinese navy had 221 ships; by 2030 it is forecast to have 435 ships.

The rapid growth of China’s armed forces is making European partners in the Indo-Pacific region, such as Australia and Japan, extremely nervous. Although European governments, including the UK’s, are very reluctant to label China a hostile state or a potential adversary, they are stepping up defence and security co-operation with countries like Australia, Japan and South Korea. The AUKUS agreement on the supply of nuclear-powered submarines to Australia by the UK and US was a source of bad feeling between the UK and France (which saw its contract to supply diesel-powered submarines cancelled without consultation). But it was an important example of an Indo-Pacific country seeing the need to look to Europe and North America for the capabilities required to face up to a growing Chinese challenge. In Japan’s case, it has joined the UK and Italy in the Global Combat Air Programme, with the aim of developing a stealth fighter that should enter service in 2035.43 Japan and South Korea have both signed security and defence partnerships with the EU (as has the UK), the first step towards being able to participate in projects under the EU’s SAFE (Security Action for Europe) programme.

The challenge from China is not limited to the Indo-Pacific region. The initial wave of Chinese investment in infrastructure, primarily in the global south, under the Belt and Road Initiative (BRI) has passed, and China is now lending large sums ($240 billion between 2000 and 2021) to bail out countries that cannot repay their previous debts to China.44 But the BRI and successor initiatives like the Global Development Initiative, Global Security Initiative and Global Civilisation Initiative are giving China considerable influence in Asia, Africa and Latin America.

China’s rising stock comes at the expense of Western countries that are reducing development assistance and often appear to be more focussed on keeping out migrants from countries in the global south than on helping them to progress economically.45 For commodity-exporting countries, China is now their most important market, and often a major investor. The ‘Digital Silk Road’ leads to dependency on Chinese communications technology, which in turn involves acceptance of Chinese technical standards; the EU can no longer rely on ‘the Brussels effect’ of widespread global acceptance of EU technical standards.46 Instead, China is using its power as an exporter of technology to export techno-authoritarianism and the surveillance state as well.47 One way in which it is doing this is by training thousands of officials from countries involved in Chinese initiatives.48 The attractions of the Chinese model of authoritarian control are not only felt in the global south. In Europe, Hungarian prime minister Viktor Orbán spoke approvingly of China in his 2014 speech on ‘illiberal democracy’, and his government has continued to pursue a pro-Chinese line within the EU.49

Europe’s efforts to combat Chinese influence and the promotion of China’s model of governance have to take account of the US’s current erratic approach. Trump’s inconsistent tariffs policy has seen the average US tariff rate on goods from China rise from 20.7 per cent before Trump took office to 127 per cent on May 3rd before falling to 51.8 per cent on May 14th and then climbing again gradually to the current level of 57.6 per cent (with an additional 100 per cent to be added on November 1st). In September, however, Trump lobbied European leaders (including in a bizarre post on his social media platform, Truth Social, addressed to “all NATO leaders, and the World”) to impose tariffs of 50 to 100 per cent on China to punish it for purchases of Russian oil, with the tariffs to be completely lifted when the war between Russia and Ukraine ended.

At the same time, despite the long-term concerns of US intelligence agencies about China’s development of AI, Trump lifted a ban on the export of some chips used in AI applications, in return for Nvidia and AMD, the manufacturers, giving the US government 15 per cent of the revenues from sales of the previously banned chips. He also indicated that he was open to allowing Nvidia to sell even more advanced chips to China on a similar basis – thereby undercutting previous US arguments for Europeans also to maintain export controls on high-tech items.50 After a long period in which US administrations, including the first Trump administration, have seen China as the main geopolitical threat to US primacy, a leaked draft of the new National Defense Strategy suggested that US forces should focus on defending the US and the Western hemisphere, making competition with China a lower priority.51 The dismantling of the US Agency for International Development and other soft power tools such as the Voice of America are already giving China opportunities to increase its influence in areas vacated by the US. It is not clear where it would leave the US’s allies in the Indo-Pacific region, or what impact it might have on China’s ambitions elsewhere in the global south, if the US withdrew from most foreign entanglements. Europe could certainly not replace the US as a provider of global goods, including security – least of all with a continuing war in Europe. But Europeans will not want to see China becoming completely dominant, at the expense of Europe’s democratic partners.

The China and regional strategies of the EU, UK, France and Germany

The China strategies of the EU and Germany, the Indo-Pacific strategy of France and the UK’s collection of policies touching on China and the region have many similarities. In general, even those that call themselves strategies are not: they are vague about objectives and even vaguer about the means to be allocated. Perhaps that is inevitable: China has its own objectives, and Europe’s ability to influence Beijing is generally limited. Almost all European governments are basically trying to maintain as good a relationship with China as possible, in particular in the economic sphere, while mitigating threats to the extent they can.

Europe could certainly not replace the US as a provider of global goods, including security.

Neither the EU nor any European state, however, has tried to explore in detail what it means for China to be a systemic rival, as the EU’s Strategic Outlook described it, or how, if China is promoting “alternative models of governance” European powers can counter them, and promote their own liberal democratic model. None of the European policy statements uses the sort of language about the kind of world order China wants to see that was used in past US National Security Strategies: Trump’s 2017 strategy said that China (and Russia) wanted “to shape a world antithetical to US values and interests”, while Biden’s 2022 strategy portrayed China as having “the intention and, increasingly, the capacity to reshape the international order in favour of one that tilts the global playing field to its benefit”. The EU perhaps came closest to conveying Europe’s fear of the Chinese model prevailing, and the need to do something different in order to avoid that outcome: “in order to maintain its prosperity, values and social model over the long term, there are areas where the EU itself needs to adapt to changing economic realities and strengthen its own domestic policies and industrial base”.

The strategies vary in the extent to which they reflect the geopolitical challenge posed by China’s behaviour in its region and its partnership with Russia. The German strategy describes China’s closer ties with Russia as having “direct security implications for Germany”, though without spelling them out; and warns that China’s assertiveness in striving for regional hegemony is “calling principles of international law into question.” France says that China’s role “has been essential in facilitating Russian aggression since 2022”. The UK National Security Strategy says that “Authoritarian states are putting in place multi-year plans to out-compete liberal democracies in every domain”, and claims that “the challenge of competition from China – which ranges from military modernisation to an assertion of state power that encompasses economic, industrial, science and technology policy – has potentially huge consequences for the lives of British citizens” – though without saying what the consequences might be.

The UK and all its partners are keen to stress the scope for co-operation with China, particularly in relation to combatting climate change, though not limited to that. The German strategy states “China exerts a crucial influence on all key issues relating to our world order. The Federal Government is seeking to cooperate with China, particularly as an essential actor in solving key global challenges”. France’s Indo-Pacific strategy is a little more reserved: it speaks of maintaining “a close and rigorous dialogue with the Chinese authorities at the highest level, seeking convergence on international crises and global issues wherever possible”.

China’s role as the largest emitter of greenhouse gases and the largest producer of the goods needed for the transition to net zero does indeed make China an essential partner. At the same time, the relentless growth of China’s production, helped by state subsidies, threatens to destroy European green industries. There is a significant divergence in the policy response to this threat between the EU, which has imposed tariffs of up to 35 per cent on imports of Chinese electric vehicles, in an effort to protect their European competitors, and the UK, which has imposed no tariffs and has (in effect) accepted that Chinese EVs will out-compete the alternatives.

The relentless growth of China’s production, helped by state subsidies, threatens to destroy European green industries.

Germany has traditionally tried to dissuade the Commission from using trade defence measures such as anti-dumping duties against China, for fear that Germany’s sizeable exports to China would be the main target for retaliation. But even Germany now seems to recognise that if the EU remains as open to Chinese imports as it has been, then German industries will be driven out of business.52 As a medium-sized, open economy, the UK has little leverage to use with China, and has no wish to impose (in effect) higher costs on UK consumers and provoke retaliatory tariffs and other barriers from China that would hit British exporters. But there is a considerable risk that the UK will become entirely dependent on China for the green goods it needs for its energy transition. This is less of a risk than being dependent on Russia for fossil fuels, as much of Europe was before 2022, in the sense that if China turned off the supply of equipment and technology it would take much longer for Europe to feel the pinch. But dependency on a country that is aligned with Russia, the main threat to the UK’s and Europe’s security, is still undesirable.

The UK and other European countries have tended to treat the competitive aspects of the relationship with China as just a matter of negotiating improved treatment of their businesses until eventually the playing field is levelled. The UK’s trade strategy speaks of grasping opportunities to achieve UK growth through trade with China in areas of economic strength.53 The EU’s strategic outlook says that the Union should “robustly seek more balanced and reciprocal conditions governing the economic relationship”. The French strategy includes “re-establishing a framework of fair competition and reducing excessive strategic dependence”. Germany uses similar language, but does at least recognise the problem that all Europeans have: “whereas China’s dependencies on Europe are constantly declining, Germany’s dependencies on China have taken on greater significance in recent years”. Europeans need to accept that even if China was making some moves towards opening up its economy under Xi’s predecessors, the process has now gone into reverse: Xi’s economic policies are designed to make China independent of the world, while the rest of the world becomes more dependent on China. These policies may not be sustainable in the long term, but in the meantime they can lead to European deindustrialisation, damaging European economies and social cohesion.

On the intelligence and security threats from China, there is an air of unreality about some of the European responses. The German strategy recognised the problems that military-civil fusion posed for scientific and technical co-operation with China, but seemed to think that the answer was for China’s research institutions to be as open as Germany’s, rather than that Germany might need to do more to prevent the outflow of sensitive technology and knowledge. France did not mention the issue at all. The UK’s National Security Strategy recognised that “instances of China’s espionage, interference in our democracy and the undermining of our economic security have increased in recent years”. It spoke of “bolstering our defences and responding with strong counter-measures”; but when the UK’s Foreign Influence Registration Scheme was launched in July 2025, Russia and Iran were the only countries included in the ‘enhanced tier’, requiring organisations or individuals to register in a wide range of cases where they were being contracted or given incentives to act on behalf of a foreign government. China was put in the same category as EU member-states, with registration only required in a narrow range of cases involving attempts to influence ministerial or governmental decisions, election or referendum outcomes, or the positions taken by political parties or MPs.

A European approach to China?

Europeans would benefit from having co-ordinated policies towards China – something that they struggled with even before Brexit. The starting point should be improved understanding of what China under Xi is doing. The UK’s efforts to increase China expertise in the civil service, not limited to the Foreign Office, could be emulated elsewhere; and European governments could step up information sharing with each other and with partners in the Indo-Pacific region. They could also co-ordinate their engagements with the region better, for example in relation to freedom of navigation operations in the South China Sea and the Taiwan Strait. As a recent Chatham House report said, European and Indo-Pacific partners all have limited resources, but many have shared goals.54

China is adept at framing its messages for the outside world; Europe needs more experts able to read the documents in which policies like military-civil fusion or Made in China 2025 are set out, understand what their implications are for Europe, and explain them to firms, universities and decision-makers. There are at least three European networks of experts on China, with some overlaps between them; two of them also have UK members or connections to UK institutions.55 Of the three, one received EU funding which has now ended and one received support from the US National Endowment for Democracy, which Trump has tried to defund. Their research and outreach activities deserve support from the EU and national governments.

Over his time in power, Xi has shown that his priority is regime and especially Communist Party survival.

A good research basis should help to counteract any naïve optimism about opportunities for Europe in China, and to encourage renewed effort to ‘de-risk’ – to reduce Europe’s dependencies on China. Over his time in power, Xi has shown that his priority is regime and especially Communist Party survival. That has meant increasing state influence in the economy and bringing to heel business figures who show too much independence. Xi has shown little interest in levelling the playing field or opening up the many sectors of China’s economy in which foreign involvement is banned or limited.

The EU has equipped itself with a wide variety of legislative and regulatory tools, such as the Critical Raw Materials Act and measures set out in the Economic Security Strategy, to try to ensure that China cannot gain too much influence through its economic leverage and that Europe can remain economically competitive. In practical terms, however, the strategy remains a patchwork of tools largely applied at the national rather than the EU level, which results in varying degrees of effectiveness in its application.56 The UK, with its much smaller economy, is more exposed, and there is not much that closer co-operation with the EU can do to reduce its vulnerability to Chinese pressure; though it may be able to work in parallel with the EU in diversifying supply chains away from China. There are some areas of technology (see above) in which the EU and UK could work together to compete with China. Both could also reduce their dependency on China for rare earth elements if they could co-operate to recycle more batteries, magnets and other electronic components – currently the EU and UK both recycle less than 1 per cent of these materials.57

Both the EU and UK are already taking steps to strengthen their controls over who studies what in higher education. The EU adopted recommendations on improving research security in May 2024; the Commission is also working to align measures that the EU takes to prevent sensitive research being exported with the steps taken by key international partners – which should include the UK. The UK itself has the Academic Technology Approval Scheme, which obliges foreign students and researchers wanting to work in the UK on particularly sensitive issues to apply for permission to do so. The scheme has some weaknesses, however, since it has not been able to stop Chinese students linked to military universities studying high-risk subjects. More information exchanges between the UK and the EU and its member-states could help to identify patterns in the research topics of Chinese students and researchers from military-linked institutions, and any gaps in coverage caused by the emergence of new technologies or subjects of study. Exchanges could also ensure that any researchers turned away from one institution on security grounds would find it harder to get into another in a different country.

The EU and the UK are also stepping up scrutiny of inward and outward investments – not only targeting China, but clearly motivated by concern both about China acquiring sensitive knowledge from the acquisition of European firms, and about European firms wittingly or unwittingly transferring knowledge to China through investment there. Again, exchanges of information could highlight patterns of suspicious or risky investment. Where the available information allows it, EU and UK law enforcement co-operation could help to ensure that illicit activity is not only disrupted but prosecuted – a much greater deterrent.

The UK and EU (and member-states) should step up intelligence exchanges on China’s political and economic activities in Europe, as they have done on sanctions circumvention – enabling measures to be taken against a number of Chinese firms involved in supporting Russian military industry. They should co-operate in identifying firms or individuals who seem to be acting on behalf of the Chinese authorities, including (for example) purportedly independent venture capital firms investing in sensitive sectors. They should also take a more consistent approach to organisations like Confucius Institutes attached to universities, which in addition to teaching Chinese language and culture also keep Chinese students under surveillance and may be involved in propaganda and influence operations in universities and with local companies.

Conclusion

In his statement to the House of Commons on the China audit, Lammy said “Not engaging with China is… no choice at all. Chinese power is an inescapable fact”. Engagement with China is indeed inevitable and necessary. To the extent that there may still be areas in which European and Chinese objectives are aligned, such as combatting climate change, the EU and UK should pursue dialogue. But they should not be naïve. ‘My enemy’s enemy is my friend’ is an old Russian saying; by the same token, ‘my enemy’s friend is not my friend’ – even if the UK and EU both shy away from labelling China as a hostile state, still less an enemy.58 China has built up its power with a view to pursuing ends that will in many cases not be aligned with European values or interests.

Saying that Chinese power is an inescapable fact carries the implication that the UK and other Europeans have no choice but to accommodate themselves to it – to take whatever crumbs China offers by way of trade concessions, to refrain from making too much fuss about Chinese influence operations and to watch as China replaces the US as the 21st century’s hegemonic power. Europe should have learned from the events of the last few years that dependency, whether on Russia for gas or the US for defence, creates vulnerability. De-risking, even at the expense of some loss of economic efficiency, needs to become a long-term goal. Europe, including the UK, needs to defend its own interests and carve out its own space in the emerging international architecture.

In its relations with Europe, China will seek to divide and rule where it can. Its efforts to cultivate all the countries of Central and Eastern Europe at once through the 16+1 process seem to have foundered, in part because of its attempt to bully Lithuania over its relationship with Taiwan; but it still has close ties with countries like Hungary and (among candidate countries) Serbia. Even if complete consensus remained out of reach, a common approach among Europe’s major economic and military powers, including the UK, would be of value.

The EU was right to say in 2019 that China was a systemic rival. In the interim, the threat posed by China to the liberal international order has only grown. The UK’s National Security Strategy says that “the challenge of competition from China – which ranges from military modernisation to an assertion of state power that encompasses economic, industrial, science and technology policy – has potentially huge consequences for the lives of British citizens”, and speaks of the need for alignment with G7 and other partners. But neither the EU nor the UK have drawn the policy consequences from their own analysis. Knowing that China’s promotion of its own system of authoritarian governance is a problem is not enough. The UK, as much as its European partners, should embrace the idea of systemic rivalry and work to ensure that European liberal, democracy – battered though it looks at present – shows its superiority to the authoritarian model promoted by Xi.

2: ‘China audit: Volume 769: Debated on Tuesday 24 June 2025’, Hansard.

3: ‘Joint communication to the European Parliament, the European Council and the Council: EU-China – A strategic outlook’, European Commission and High Representative of the Union for foreign affairs and security policy, March 12th 2019.

4: ‘EU-China trade: Facts and figures’, website of the Council of the European Union, updated August 8th 2025.

5: UK figures from ‘Trade and investment factsheet: China’, UK Department for Business and Trade, updated September 19th 2025.

6: Mure Dickie and Tony Barber, ‘Move to tackle EU-China trade imbalance’, Financial Times, November 28th 2007.

7: ‘25th EU-China summit - EU press release’, July 24th 2025.

8: ‘Secretary of State for Business and Trade visit to China factsheet’, Department for Business and Trade, September 12th 2025.

9: Camille Boullenois, Agatha Kratz and Daniel Rosen, ‘Overcapacity at the gate’, Rhodium Group, March 26th 2024.

10: Sander Tordoir and Brad Setser, ‘How German industry can survive the second China shock’, Centre for European Reform policy brief, January 16th 2025.

11: Jake Benford and Anton Spisak, ‘A missing pillar: Economic security co-operation in the EU-UK partnership’, and the technical annex to the report, Anton Spisak, ‘Mapping EU-UK import dependencies and shared vulnerabilities’, Bertelsmann Foundation policy brief, September 2025.

12: Fredrik Erixon and Oscar Guinea (project leads), ‘Key Trade Data Points on the EU-27 Pharmaceutical Supply Chain’, European Centre for International Political Economy, July 2020.

13: Sujay Shetty, Hardik Dave and Nisha Bhatia, ‘Reducing dependency: Making India’s API industry self-reliant’, PWC India, September 2020.

14: Robert Clark and Richard Norrie, ‘China’s presence in NHS supply chains: Why we need to protect our health service from future threat’, Civitas, May 2022.

15: Roland Gauß and others, ‘Rare earth magnets and motors: A European call for action’, report by the Rare Earth Magnets and Motors Cluster of the European Raw Materials Alliance, 2021.

16: Ryan McMorrow, ‘China unveils sweeping rare-earth export controls to protect ‘national security’’, Financial Times, October 9th 2025.

17: ‘World intellectual property indicators 2024’, World Intellectual Property Organisation, 2024.

18: ‘Global innovation index: Innovation at a crossroads’, World Intellectual Property Organisation, 2025.

19: Jennifer Wong Leung, Stephan Robin and Danielle Cave, ‘ASPI’s two-decade Critical Technology Tracker: The rewards of long-term research investment’, Australian Strategic Policy Institute, August 2024.

20: ‘R&D spending growth slows in OECD, surges in China; government support for energy and defence R&D rises sharply’, OECD statistical release, March 31st 2025.

21: Brendan Oliss, Cole McFaul and Jaret Riddick, ‘The global distribution of STEM graduates: Which countries lead the way?’, Center for Security and Emerging Technology, Georgetown University, November 27th 2023.

22: Zongshuai Fan, ‘China’s emerging industrial vision: The significance and impact of ‘New Quality Productive Forces’, Cambridge Industrial Innovation Policy, University of Cambridge, April 17th 2024.

23: ‘Strengthen mission responsibility, deepen reform and innovation, and comprehensively enhance strategic capabilities in emerging fields’, Xi Jinping’s important speeches database, People’s Daily online, March 8th 2024.

24: András Rácz and Alina Hrytsenko, ‘Partnership short of alliance: Military co-operation between Russia and China’, Center for European Policy Analysis, June 16th 2025.

25: Paul Bolton, Joe Lewis and Melanie Gower, ‘International students in UK higher education’, House of Commons Library research briefing, June 27th 2025.

26: Sam Armstrong, ‘Brain drain: The UK, China and the question of intellectual property theft’, Henry Jackson Society, September 2020.

27: Tau Yang, ‘United Kingdom: Opaque research ties, hidden CCP influence at the expense of a large Chinese student diaspora’, Central European Institute of Asian Studies, September 29th 2025.

28: Annebelle de Bruijn and others, ‘China sends selected military researchers to the Netherlands to gather sensitive knowledge’, Follow the Money, May 21st 2022.

29: Camille Brugier, ‘France: An uneven awakening to the risks posed by China in academic cooperation’, Central European Institute of Asian Studies, June 17th 2025.

30: Peter Haeck, ‘China’s military is tapping into EU-funded research’, Politico, June 27th 2024.

31: Finbarr Bermingham, ‘China tells EU it does not want to see Russia lose its war in Ukraine: sources’, South China Morning Post, July 4th 2025.

32: ‘Xi puts forth four principles to resolve Ukraine crisis’, The State Council of the People’s Republic of China, April 16th 2024.

33: ‘Wang Yi Meets with Ukrainian Foreign Minister Andrii Sybiha’, Ministry of Foreign Affairs of the People’s Republic of China, September 26th 2025.

34: Alessia Caruso and Tim Rühlig, ‘The dependence gap in Russia-China relations’, European Union Institute for Security Studies, October 2nd 2025.

35: ‘80% of military components for Russia come through China, says EU’s special envoy’, TVP World, June 30th 2025.

36: Demian Shevko, ‘Ukraine says 92% of foreign drone parts in Russia’s arsenal come from China’, NV – The New Voice of Ukraine, July 8th 2025.

37: Sarah Anne Aarup, Sergey Panov and Douglas Busvine, ‘China secretly sends enough gear to Russia to equip an army’, Politico, July 24th 2023.

38: ‘Tracking the impacts of G7 & EU’s sanctions on Russian oil’, Centre for Research on Energy and Clean Air, data accessed on October 4th 2025.

39: Author’s calculations, based on data from the World Bank’s World Integrated Trade Solution.

40: Stuart Lau, ‘US accuses China of giving ‘very substantial’ help to Russia’s war machine’, Politico, September 10th 2024.

41: Oleksandr Danylyuk and Jack Watling, ‘How Russia is helping China prepare to seize Taiwan’, Royal United Services Institute, September 26th 2025.

42: Matthew P. Funaiole and Brian Hart, ‘China’s military in 10 charts’, Center for Strategic and International Studies, September 2nd 2025.

43: ‘Joint Statement from Prime Ministers of UK, Italy and Japan: 9 December 2022’, UK government website, December 9th 2022.

44: Sebastian Horn, Bradley Parks, Carmen Reinhart and Christoph Trebesch, ‘China as an international lender of last resort’, National Bureau of Economic Research Working Paper, April 2023.

45: Katherine Pye, ‘Access denied: The EU’s discriminatory visa regime is undermining its reputation in Africa’, Centre for European Reform insight, April 2nd 2025.

46: John Seaman, ‘Technical standards, soft connectivity and China’s Belt and Road: Towards greater convergence or fragmentation?’, Reconnect China policy brief, Ghent University, February 2025.

47: See, for example, Anu Bradford, ‘Digital empires: The global battle to regulate technology’, Chapter 8 ‘Exporting China’s digital authoritarianism through infrastructure’, Oxford University Press, August 2023.

48: Niva Yau, ‘A global south with Chinese characteristics’, Atlantic Council, June 13th 2024.

49: ‘Prime Minister Viktor Orbán’s speech at the 25th Bálványos summer free university and student camp’, Hungarian government website, July 30th 2014; Ilona Gizińska and Paulina Uznańska, ‘China’s European bridgehead. Hungary’s dangerous relationship with Beijing’, OSW (Polish Centre for Eastern Studies), January 12th 2024.

50: Helen Davidson and agencies, ‘Trump sparks concern after suggesting he might allow sales of Nvidia’s advanced AI chips in China’, The Guardian, August 12th 2025.

51: Paul McLeary and Daniel Lippman, ‘Pentagon plan prioritizes homeland over China threat’, Politico, September 5th 2025.

52: Sander Tordoir and Brad Setser, ‘How German industry can survive the second China shock’, Centre for European Reform policy brief, January 16th 2025.

53: ‘The UK’s trade strategy’, June 2025.54: Ben Bland, Olivia O’Sullivan and Chietigj Bajpaee, ‘Why the Indo-Pacific should be a higher priority for the UK’, Chatham House, July 2025.

54: Ben Bland, Olivia O’Sullivan and Chietigj Bajpaee, ‘Why the Indo-Pacific should be a higher priority for the UK’, Chatham House, July 2025.

55: They are the European Think-Tank Network on China, co-ordinated by Spain’s Elcano Royal Institute, the French Institute of International Relations and the Berlin-based Mercator Institute for China Studies (MERICS); the China in Europe Research Network (CHERN), which involves a range of universities, including several in the UK, as well as the EU Institute for Security Studies; and China Observers in Central and Eastern Europe, a network run by the Association for International Affairs (AMO) in Prague.

56: Francesca Ghiretti, ‘The return of economic statecraft’, RAND Corporation, October 1st 2025.

57: ‘Critical raw materials’, British Geological Survey Minerals UK website, accessed on October 4th 2025.

58: Helen Warrell, Suzi Ring, David Sheppard and Joe Leahy, ‘Collapse of China spy case shows ‘UK can be bullied’, says trial witness’, Financial Times, October 8th 2025.

Ian Bond is deputy director of the Centre for European Reform.

October 2025

View press release

Download full publication

This policy brief is the second of a three-paper CER/KAS project, ‘Navigating stormy waters: UK-EU co-operation in a shifting global landscape.’ The first brief was ‘Will EU enlargement create new models for the EU-UK relationship?’. The final paper will look at progress in the EU-UK reset.

The author is grateful to Hannah Merrick for her assistance with the research for this paper.

Related content