Competition policy must reflect Europe's reality, not its aspirations

The European Commission is under pressure to tweak competition laws to promote European innovation. These efforts risk delivering all the downsides of America’s traditional approach to competition policy – such as higher prices – without any commensurate benefits.

In recent months, two major reports on the EU by former Italian prime ministers, Enrico Letta and Mario Draghi, have painted a dire picture of the bloc’s economic prospects. It is hard to argue with their diagnosis: Europe has doggedly low productivity growth, meaning it is struggling to become more efficient and produce more value for each hour worked. One reason is that established European firms are not using new technologies or innovating much themselves, while small and innovative firms are often unable to grow. Letta and Draghi conclude that one way to partly solve the problem would be for the European Commission to think more about innovation and growth in enforcing competition policy – a position that British prime minister Keir Starmer recently echoed in criticising the UK’s competition authority.

But competition policy is not the main cause of Europe’s innovation woes. If she is confirmed as the next Commission’s competition czar, Teresa Ribera should avoid sharp changes to the bloc’s antitrust policies until the EU tackles more important reforms. Adjusting competition policy now risks making Europe’s poor record on innovation even worse.

Adjusting competition policy now risks making Europe’s poor record on innovation even worse.

In his report, Draghi correctly identifies the main problem behind Europe’s low productivity growth: its stagnant business environment. Europe’s largest firms are far older than America’s giants. They have focused too much on incremental innovation and have faced too little pressure to embrace radical change. Europe’s competition policy was supposed to prevent this outcome. Over recent decades, it has mostly been tougher than that of the US: more willing to block mergers and to punish dominant firms for abusing their positions. Competition was supposed to not only force firms to keep their prices low, but also to pressure them to innovate. It has performed the first task well: businesses in Europe tend to have more direct competitors and to be less profitable than US equivalents, which suggests European consumers get a good deal. But European businesses are making fewer productive investments than US ones and are investing far less in research and development.

Many economists see the relationship between competition and investment as U-shaped. If one firm becomes too dominant, it will not innovate since its position will be secure, and challengers will not innovate because they have little hope of overtaking the incumbent. However, if many small firms are competing neck-and-neck, they may focus on cutting costs, rather than making largely risky bets, and they may lack the scale needed to pull off large investments. This latter scenario describes Europe’s situation today. Europe’s competition policy has often in practice fixated on ensuring a certain number of firms in a particular market.

That seemed justifiable until recently. Tough competition enforcement made sense in the industries where Europe was strongest, such as production of vehicles and mechanical equipment – which are mostly mature markets where radical innovation seemed unlikely. In sectors where disruption had seemed more likely, such as ICT, European firms have little presence. That did not tend to matter much, however: the EU could piggyback off America’s innovation efforts because tech firms tended to roll out their innovations globally.

But the EU is now starting to question this approach. In the long run, innovation benefits consumers much more than lower prices do. Embracing the computing revolution, for example, was clearly more beneficial than keeping mechanical typewriters affordable. Yet the EU is now falling behind the US and China in almost all the technologies important for future growth – which is a problem not only for economic growth but also for Europe’s economic security and autonomy. Even supposedly safe, mature industries in Europe like energy and car manufacturing are suddenly becoming vulnerable to radical disruption from technological advances like batteries and electric vehicles – giving China, in particular, a chance to leapfrog Europe in global markets. And US tech firms now seem more willing to hold back their innovations from Europe.

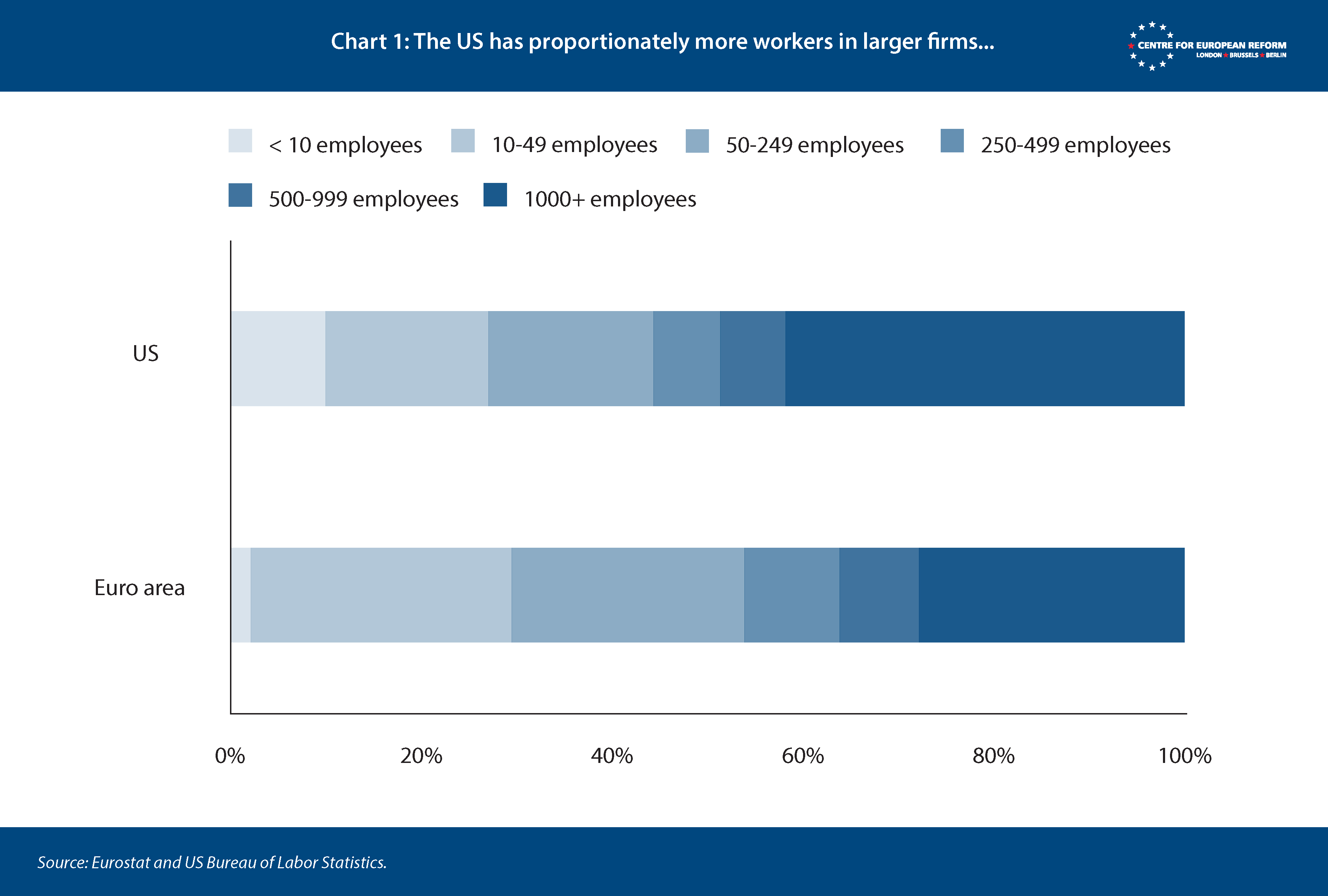

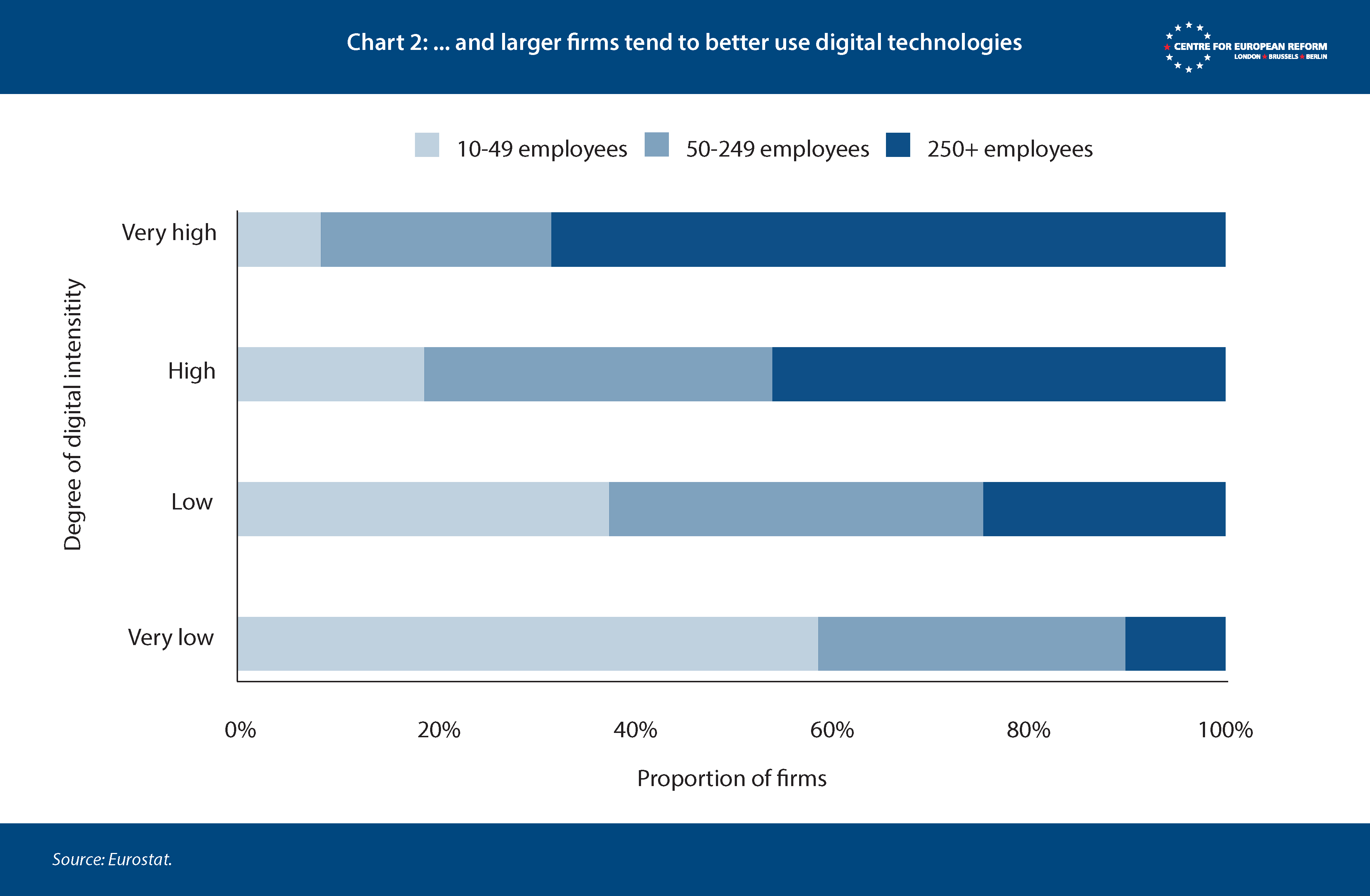

Both Draghi and Letta therefore suggest the bloc’s competition policy should be tweaked. They suggest a mix of proposals, some of which would loosen competition and others which would strengthen it. But their overall vision is for some of Europe’s markets to look more like those in America: with larger firms (see chart 1), which because of their scale should be better at innovating and deploying technology (see chart 2). For example, Draghi proposes that firms should be allowed to merge even if this would lead to higher prices for Europeans, in order to help those firms compete in foreign markets or if they promise to invest more within Europe.

Yet there is not much evidence that competition law is the key culprit for Europe’s lack of investment or innovation. The reason US firms have a greater ability to make high-potential investments is not merely because they are larger. US investors are also more risk-tolerant and take a long-term perspective. EU firms rely far more on bank lending which requires short-term return on investment. As a result, size is not everything: small European firms invest far less in adopting technology than equivalently sized American firms.

Furthermore, Europe’s lack of a properly functioning single market matters far more than its competition policy. American firms can easily grow across the US with few regulatory barriers, which means innovative firms can quickly increase their customers and earn large rewards for taking risks. In comparison, many successful European firms fail to rapidly expand across the entire EU. The US population is roughly four times that of Germany, the EU’s largest consumer market. That means even a complete monopoly in one member-state would not enjoy the scale that a firm with just a 25 per cent market share market in the US would enjoy. Furthermore, the US’s largest firms largely succeeded in ICT-based services where they could rapidly access consumers from anywhere in the world. If European firms are to succeed in sectors where huge economies of scale are essential, then completing the single market and ensuring open trade with the rest of the world is essential. Allowing firms to build up market share within a single EU member-state will make little difference.

Letta and Draghi acknowledge that competition policy should not be reformed in isolation – both emphasise the importance of developing European capital markets, deepening the EU single market, and using EU trade policy to open up access to global markets. Yet reforming competition policy will happen long before these more complex projects come to fruition.

Draghi claims that his changes to competition policy would only require the European Commission to change its practices, rather than any underlying EU law. Competition reforms also have the political support of Paris and Berlin, which still bristle at the Commission having blocked the Franco-German merger of Siemens and Alstom in 2019. Reforms of capital markets and further development of the single market, in comparison, have been bogged down for years by political resistance within member-states.

Competition reforms therefore risk creating a competition policy which is suitable for the high-innovation economy Europe wants – but not the fragmented and capital-constrained economy it will remain stuck with. The result would be all the downsides of America’s competition policy – in the form of higher prices and less choice – without proportionate benefits to innovation and investment.

A further difficulty is that Draghi and Letta see the new approach to competition policy targeting markets which are already working well, rather than those that have the most innovative potential. For example, they propose a new approach to telecoms mergers – echoing policy-makers’ concerns that Europe’s telecoms companies are too small and under-invest – despite telecoms being neither a disruptive nor a high-innovation sector.

The telecoms market is relatively mature, infrastructure-intensive and reliant on highly standardised technologies like 5G – which means investments take many years, disruptive innovation is unlikely, and the services are commoditised. That means operators compete on price and quality rather than offering fundamentally different types of services. The EU enjoys much lower prices for connectivity than the US. This is a huge advantage for European businesses which need to digitise.

The problem in the telecoms sector is European businesses’ failure to take up new technology. European businesses are not using cloud computing and AI to the same extent US firms are. Boosting take-up of these technologies is the solution – allowing telecoms prices to increase would only make take-up harder to achieve.

In contrast, in high-tech sectors like digital services, where a more innovation-focused competition policy seems more justifiable, Draghi wants competition policy to be tougher. He backs the EU’s Digital Markets Act (DMA), for example. While the DMA tries to solve real competition problems, it imposes rigid rules on tech giants, and some of these rules will constrain innovation. Loosening competition policy in telecoms (a sector dominated by European companies) while championing tough competition policy in tech (a sector dominated by US firms) would also make the EU’s competition policy incoherent and inconsistent.

Finally, changes to competition policy would likely create more problems than they would solve. When regulators emphasise innovation, competition policy inevitably becomes less predictable. For decades, EU competition policy has been shifting towards a more ‘economics-based approach’, which aimed to rely primarily on quantitative evidence to help make outcomes in competition cases more objective, accurate and predictable. Assessing the impacts of a merger on innovation, however, requires more use of qualitative evidence – such as technologists’ subjective views about which technologies could prove pivotal in the future, or how different firms could combine their technical capabilities. Judgements on these issues will inevitably prove controversial. Authorities are already grappling with how to think more systematically about innovation without undermining predictability; Letta and Draghi do not offer any solutions to this conundrum.

Competition authorities are grappling with how to take innovation into account without undermining predictability; Letta and Draghi do not offer any solutions to this conundrum.

A more innovation-focused competition policy would not necessarily result in more mergers either, as Draghi and Letta sometimes seem to assume. Concerns about innovation were the reason why the UK competition authority forced Microsoft to restructure its acquisition of Activision, and forced Meta to unwind its purchase of Giphy – both decisions which businesses criticised as unpredictable.

Draghi’s proposal that merging firms could commit to make new investments in order to get their merger approved would also create uncertainty. Such mergers would have to be unwound if the merged firm reneged on its promises. Otherwise, firms could pay a one-off penalty in order to benefit indefinitely from an uncompetitive market structure resulting from their merger. But firms may be unwilling to merge in the first place if they fear regulators could force them to undertake the expensive and complex process of unwinding a deal years later.

Europe must make radical changes to its economic model – and that may, eventually, require regulators to take a different attitude to assessing mergers and acquisitions. But competition policy’s job is to reflect Europe’s reality, not its aspirations. Draghi and Letta recognise this and recommend boosting capital markets and completing the single market as essential steps to help Europe enjoy comparable levels of innovation to the US. Reforms to competition law should follow the completion of those projects. Letta and Draghi understand that competition policy alone cannot reshape Europe’s economy – but their reports are ammunition to the EU’s political leaders who may believe otherwise.

Zach Meyers is assistant director of the Centre for European Reform.

Add new comment