In defence of borrowing for climate action

Even though interest rates are rising globally, European governments should still borrow large sums to finance green projects. In some cases, the EU should help.

The European Commission is mulling exemptions from the EU’s fiscal rules for green investment (when rules are reapplied – they are currently suspended). Germany has signalled its reticence about loosening the rules, even though it is itself borrowing significant sums to fund its €200 billion energy package. In the UK, the Treasury has argued against using debt to finance steps to achieve net zero because it considers it unfair to make future generations pay. And now that global interest rates are rising, everyone is more cautious about issuing debt. But Europe has to wean itself off fossil fuels as quickly as possible, not only to cut emissions, but also to reduce its energy dependence on Russia as well as other autocratic governments.

We need more subtle thinking about when and for what purposes governments should take on more debt. At the moment, European governments are borrowing huge sums to bail out households and businesses by reducing the cost of energy. Intervention is vital to prevent poverty and destitution, and to protect spending across the economy, which will reduce the scale of the coming recession. But this is borrowing to consume – and with natural gas prices likely to remain high at least until 2024, debt will mount up, and government bond markets will fret about debt sustainability.

Markets are more sanguine about borrowing to invest. Governments have to accelerate the pace of investment in energy efficiency and alternatives to fossil fuels. The European Commission’s ‘RepowerEU’ plan, which sets out how the EU should cut energy imports from Russia, advocates rapid investment in energy efficiency measures, especially in buildings, and the substitution of cheaper renewables for expensive gas. Governments can help to achieve this more quickly by tapping bond markets and passing on cheap finance to green investment projects.

Debt is often the cheapest way to fund green energy investments – as opposed to equity, where investors take a share of the project’s profits. Wind and solar farms are usually financed by private sector debt, because they involve a lot of upfront capital expenditure, and equity investors are put off by the long and risky period of planning and construction before revenues start flowing. Once they are built, their operating expenditure is very low – wind is free, while natural gas is not. The revenues from selling electricity cover the debt repayments (especially when government also guarantees prices).

Debt is often the cheapest way to fund green energy investments – as opposed to equity, where investors take a share of the project’s profits.

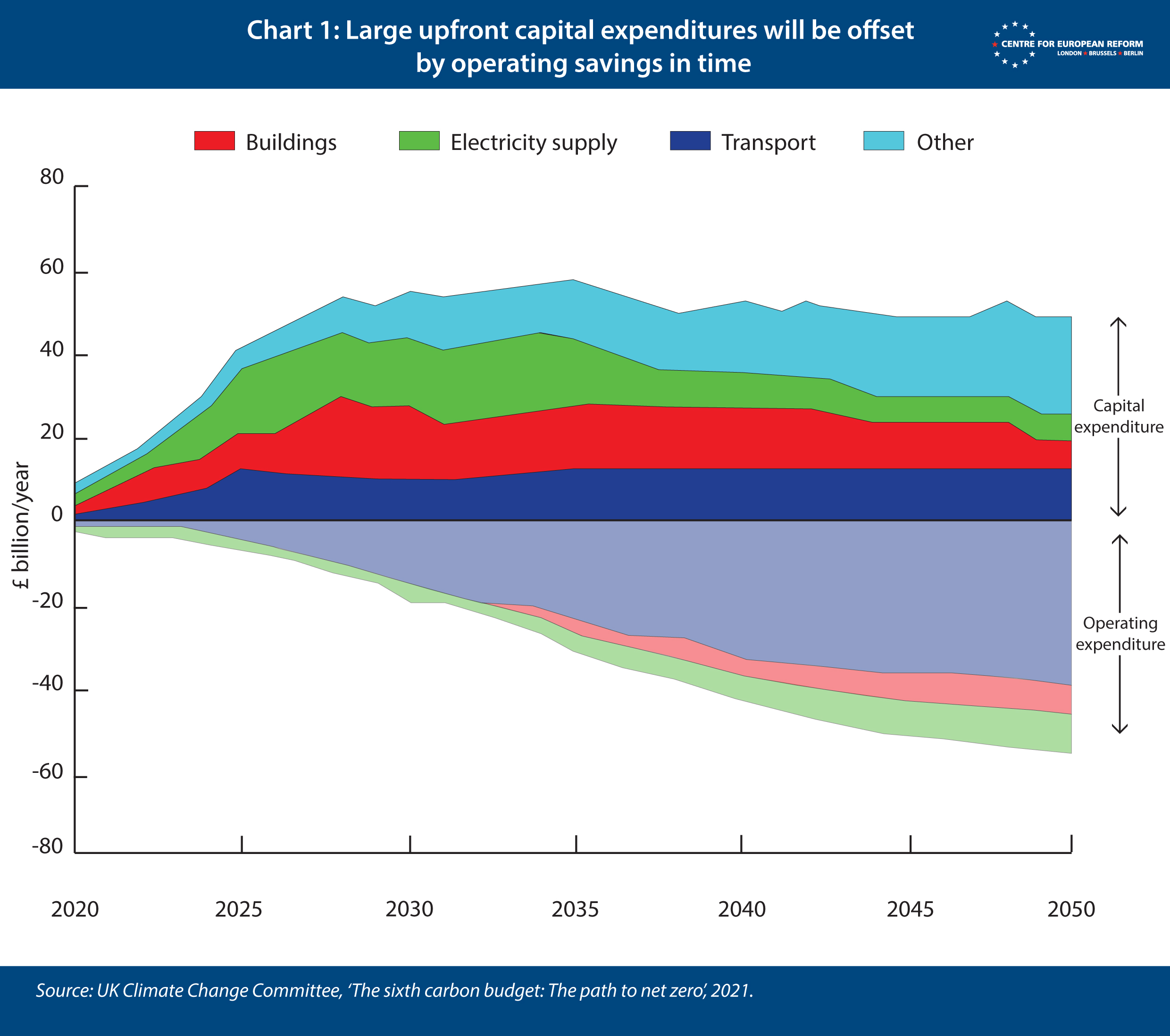

This funding structure is needed for many mature green technologies, or ones that are nearly there. Renewables, the insulation of buildings, and the installation of heat pumps to heat them all are now mature technologies that can be rolled out at scale. Chart 1 shows that, in order to meet net zero targets, capital expenditure on renewables and buildings will have to be very large this decade, with offsetting operating savings that stretch beyond 2050.

If governments can bring some of this capital investment forward, by reducing the cost of capital for investors (as well as speeding up the granting of permits, providing advice to households on retrofitting, and so forth), the operating savings will arrive sooner too. Governments can borrow at cheap rates in markets because they have more control over their tax revenues than corporations have over their income. That means they can pass on these cheap rates to projects, which will lead to more investment, more rapidly.

By borrowing to fund green projects, governments are creating assets. And if they can demonstrate to debt markets that the government will earn back at least their cost of capital, either through direct revenues from assets or from higher tax revenues arising from higher economic growth, their borrowing costs will not rise much. A borrowing government’s debt to GDP ratio may have risen – and that ratio is an important figure, and one which is closely watched by the markets – but that does not measure the riskiness of the debt.

Private sector funding is preferable for many green projects. Markets will more rapidly invest in more efficient, faster-charging batteries than government agencies will, because markets process information more efficiently than a bureaucracy can, and funnel money more rapidly to investments that offer better returns. And when governments make investments, they are exposing taxpayers to the risk that the construction is more expensive than planned, or that revenues are lower than initial estimates.

Private sector funding is preferable for many green projects. Markets will more rapidly invest in more efficient, faster-charging batteries than government agencies will.

And yet. We are in an emergency situation, in which governments are borrowing huge sums to pay for energy consumption, with money still flowing to Europe’s enemy, Vladimir Putin. The risk to taxpayers that governments bet badly must be set against a speedier cut to gas, coal and oil consumption. And if governments invest in projects using mature technology, which have high up-front capital costs followed by operating cost savings, where revenues are easily secured, government borrowing is a good tool to use.

The two best investments with all of those characteristics are renewables and other forms of low-carbon energy generation, and the insulation of buildings and the installation of new heating systems, be they heat pumps or large-scale district heating. As Chart 1 above shows, even before Putin’s invasion, investment in these two sectors needed to rise hugely in the 2020s, because they are mature technologies.

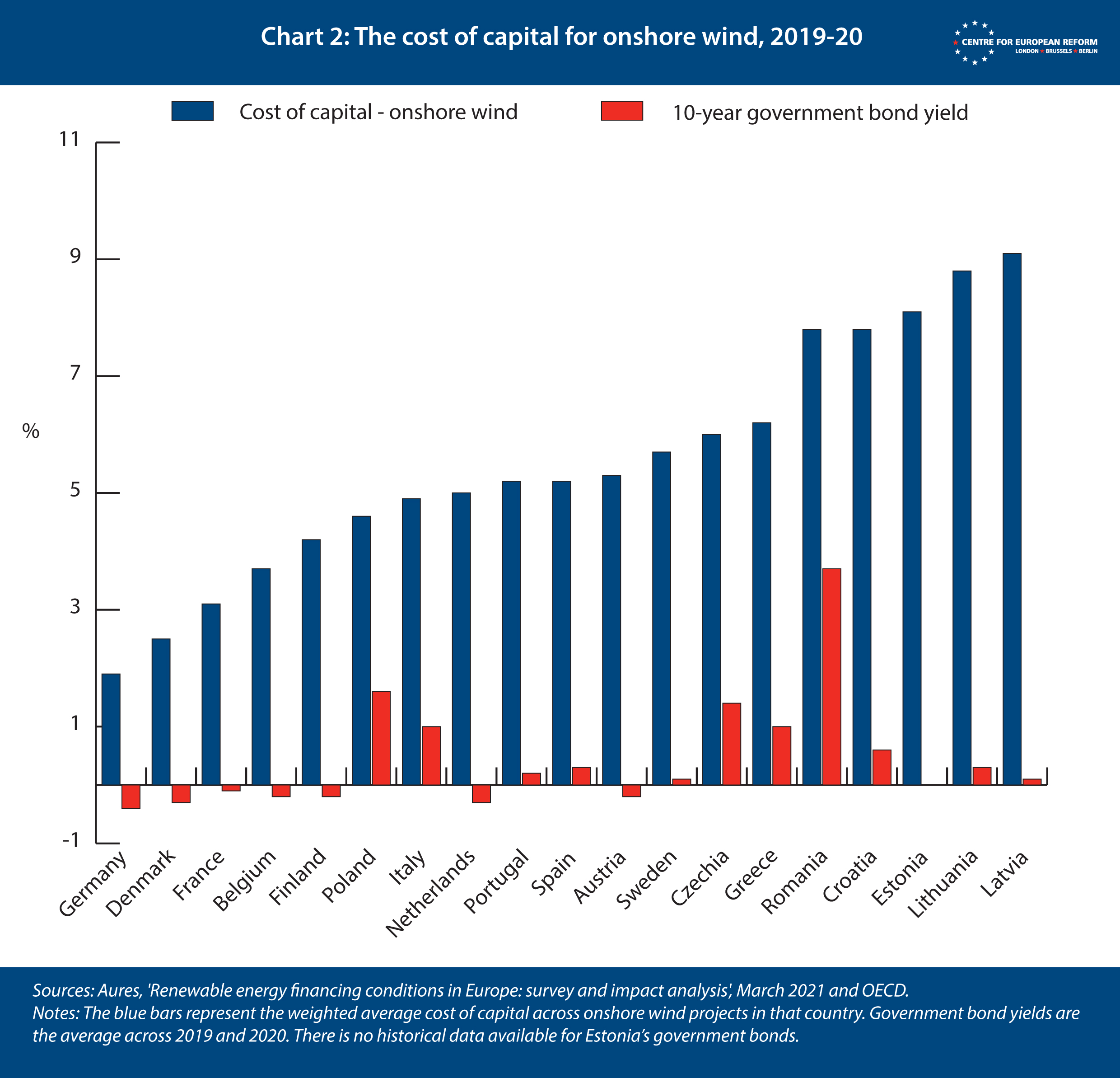

Renewables and bioenergy plants can be built fairly quickly – it’s planning and development that takes time. And once they are built, they have low operating costs. Across Europe, the cost of capital for onshore wind is 5 percentage points, on average, greater than the cost of government borrowing – even though in many cases government seeks to reduce risk for investors by guaranteeing prices for green electricity (see Chart 2). Governments could help reduce the cost of capital by providing lending to cover some of the upfront construction cost, while private investors provide the rest. This would make use of private investors’ information about which projects will generate the best returns. The government would then be paid back by the energy plant.

Most of these revenues could be used to pay back the government’s creditors, but some could provide incentives to regional and local governments to allow plants to be built in their jurisdictions. It has proved difficult to reduce lengthy planning procedures for new projects, which have to take into account the views of people who live nearby. Governments could offer to pay local authorities revenues from energy assets if they quickly provide permits for new plants to be built. Broader reforms of permitting processes would also help to allow renewable plants to be built more quickly – but these have tended to be stymied by local opposition.

Buildings are the other potential target for government loans. Over a third of Europe’s greenhouse gases are emitted from buildings. Materials for insulating buildings, energy efficient windows and district combined heat and power plants are mature technologies. Heat pumps are fairly mature – there will be improvements to the pumps as demand grows and more companies manufacture them, but much of the cost is in installing them. The typical costs of retrofitting a house are over €30,000 in Western Europe, with sizeable savings on fuel bills thereafter. If governments provided cheap loans, many more people would invest.

Better energy efficiency in buildings can generate a revenue stream, too. Households, landlords and businesses cut costly fossil fuel usage through insulation, and switch from gas to electricity through a heat pump. That generates a saving that can be used to pay the government loan back (and then the owner of the government bond). Many governments already work with private energy service companies, which give customers advice about what insulation and energy system to install, arrange finance, and update performance certificates. They or retail energy companies could administer the loans and repayment, and offer free consultations as part of the retrofit package – the surveyors would ensure that the proposed works were best for the property, and inspect the work when it was finished, thereby ensuring that the government’s asset would provide returns.

Just as renewables need work to speed up permitting, a surge in retrofitting buildings will require a lot of labour and training. Governments would have to do more to train their own citizens and loosen immigration rules to bring in more construction workers.

There is a strong case for the EU to get involved, especially to help governments that have less fiscal space. The current ten-year cost of borrowing across the Union ranges from 1.9 per cent for German Bunds, to 8.6 per cent in Romania and 9.7 per cent in Hungary (see Chart 2 above). The EU only borrowed at slightly higher rates than Germany after it started issuing its own debt under the NextGenEU plan. The EU could use its collective borrowing power to provide cheap loans to member-state governments, which could then be passed on to households, with careful monitoring by the Commission to ensure the money is invested wisely.

The EU could use its collective borrowing power to provide cheap loans to member-state governments, which could then be passed on to households.

Member-states have not taken up almost over €200 billion in cheap loans under the Recovery and Resilience Facility (RRF, a funding instrument that makes up most of NextGenEU). Under the RepowerEU plan, these funds will be repurposed for energy investment. One reason that member-states have not taken them up is that they would be added to their debt-GDP ratios. But if the money created assets with sufficient revenue streams, government bond markets would be sanguine about it. The other reason is that borrowing costs have been low for European governments until recently; they have not needed to turn to the EU for cheaper loans. With the Federal Reserve tightening global monetary conditions, yields are rising for countries that are fiscally weaker, and EU loans are becoming more attractive.

Once the principle that climate investment creates assets has been established, and once EU loans have started to be repaid, it might even be possible to persuade more hawkish governments of the merits of a permanent climate fund at the EU level.

Cutting emissions is a collective European interest, and the more cheaply and quickly, the better. So is being less dependent on autocratic governments for fossil fuels. Debt is a helpful instrument to achieve both objectives.

John Springford is deputy director of the Centre for European Reform.

Related content

The EU's energy plan for a difficult winter: What are the options?

Add new comment