Europe needs both fiscal and energy solidarity

- Putin’s invasion of Ukraine has raised energy prices and, in response, European governments are subsidising electricity and gas consumption. The European Commission has developed the REPowerEU plan to cut Russian gas out of the EU market. That plan involves energy saving targets, more imports of pipeline gas and liquefied natural gas (LNG) from countries other than Russia, and more renewable energy.

- European governments have cut energy taxes and frozen retail prices to protect consumers and businesses. So far, EU governments have allocated over €600 billion to such emergency measures (although outlays will probably turn out to be lower, given the fall in energy prices). In our analysis, we evaluate the emergency energy measures of a few countries: France, Germany, Italy, Poland, Spain, Greece, Bulgaria, and the UK.

- Some countries are targeting the subsidies better than others by making them more generous for poorer households and for small and medium enterprises. For example, Germany has provided some heating subsidies only to recipients of housing benefits, and Italy has provided more generous discounts on energy bills to households under a certain income threshold.

- In the member-states we focus on, governments have spent over four times more on price control measures like tax cuts and price freezes than on cash transfers. The latter are preferable because they preserve incentives to save energy.

- Compared to consumption subsidies, EU governments have been doing much less to reduce dependence on gas by cutting demand. In the past year, new incentives for energy efficiency investments have remained substantially below energy subsidies.

- While natural gas prices have come down from their highs, they are currently twice as high as they were before Russia’s invasion. The European economy needs to adjust to a prolonged period of higher gas prices. Smoothing the shock for household and firms in the short term is a good idea, but governments should not continue to subsidise energy consumption forever. Instead, they should reduce subsidies over time and support investment to reduce dependence on gas.

- Governments should devote more and better targeted resources to the retrofitting of buildings and to encourage businesses to invest more in energy efficiency. They should also invest in modernising the electricity grid and increasing renewable energy capacity, which will help to replace imported gas with domestic sources of energy supply. Reforming planning rules to accelerate investment in renewables is a good example of how removing administrative barriers can also boost investment.

- To finance the REPowerEU plan and help governments in these efforts, the EU is repurposing some unused funds to make about €300 billion in lending available to member-states. These are loans, not grants, which benefit governments whose borrowing costs are higher than those of the EU as a whole. According to our calculations, using these loans would provide an investment subsidy of only €6 billion a year to 2026 for the entire EU-27. This would provide some helpful support for countries whose national borrowing costs are far higher than the EU’s, such as Hungary, Romania and Bulgaria.

- However, to meet its 2030 emissions reduction targets, the EU needs to invest an additional €250-300 billion a year, so in aggregate terms REPowerEU constitutes a small subsidy for the energy transition. Without more EU investment support, poorer and more indebted countries might struggle to speed the transition away from fossil fuels. And as government borrowing costs rise, Europe might repeat the mistake of the 2010s, when investment was severely curtailed by austerity programmes.

- The response to the energy crunch has showed that richer and less-indebted countries can afford more generous energy subsidies to households and businesses. The divisions between member-states with low and high public debt are now affecting the debate on the EU’s state aid rules. In a world where China and the US are using massive public subsidies to support their green tech industries, not all EU member-states agree on how to respond. France and Germany would like EU state aid rules to be relaxed to allow governments to provide US-style subsidies to green industries. The European Commission plans to loosen these rules to make room for a more ambitious industrial policy in the clean tech sector, but is meeting the opposition of laissez-faire member-states such as the Netherlands and high-debt countries like Italy, which would not be able to subsidise their industries as generously.

- European manufacturers’ competitiveness will be undermined without a rapid shift to cheaper and cleaner fuel sources. The best way to achieve that shift is unlikely to be US-style production subsidies for green tech producers. The US Inflation Reduction Act is prompting the EU to consider its own subsidies for green tech producers. Instead, cheap finance for zero-carbon energy infrastructure is needed, since many of the key technologies needed to curb gas consumption are nearing maturity. The EU should establish a climate fund to speed the energy transition, and finance it with joint borrowing, building upon the success of the NextGenerationEU fund.

The worst of the energy crisis is over: European energy costs have come down from their September 2022 peak. But prices remain much higher than before Putin’s February invasion of Ukraine, and markets expect them to remain high for many years to come. So far, the EU’s collective answer to the crisis has largely focused on setting energy savings targets and recommendations to help member-states curb energy demand while protecting consumers. The ‘REPowerEU’ plan, put forward by the European Commission in May 2022, provided a framework for curbing Russian gas imports while maintaining security of supply, and set targets for gas and electricity savings to be achieved by March 2023.

However, energy solidarity has been little more than a buzzword so far: most member-states have embarked on their own bilateral negotiations with gas suppliers, instead of making use of the EU energy platform for common gas procurement, aside from a November agreement to buy 15 per cent of gas for storage via the platform in 2023. Similarly, member-states have chosen to water down EU-wide gas saving targets with a range of exemptions and caveats. If energy solidarity appears weak, fiscal solidarity, in the form of EU borrowing to help weaker member-states deal with the costs of the crisis, is unlikely to happen in the coming months, due to opposition in Germany and other countries opposing intra-EU transfers.

Compared to the response to the Covid crisis, the EU-level fiscal response to the energy crisis seems meagre. Yet, the energy shock may have bigger long-term consequences for the European economy than the pandemic, which resulted in a very deep (if short-lived) recession but is less likely to impose large long-term structural changes to the economy. If high gas and electricity costs persist for several years, the economy will have to adjust by switching more rapidly to alternative energy sources and raising energy efficiency. If these adjustments do not take place, more energy-intensive businesses might move production outside the EU. Cutting Russian gas imports and transitioning to a low-carbon energy system will be costly: it will entail the closure of some energy-intensive businesses, and will require capital investment and training.

So far, all European governments have tried to limit the hit to household budgets from higher energy costs. They have mainly done so by regulating household energy prices, and by paying energy suppliers the difference between retail and wholesale energy prices. Many governments are subsidising businesses in a similar way. But if energy prices remain high in the medium term, there is a limit to how long governments can – and should – maintain this level of support. Emergency measures have so far required sizeable government borrowing, shifting the cost of subsidies onto future taxpayers. Furthermore, if gas prices remain high because Russian gas is permanently removed from the European market, as seems likely, Europe will need to double down on energy savings and alternative energy sources. That makes the signal from higher gas prices important for incentivising households and businesses to invest in energy efficiency, and for energy firms to invest in alternative energy sources.

This policy brief assesses the policies European governments have enacted to protect households and businesses against growing energy costs, and to provide incentives to accelerate investment in low-carbon alternatives. It also assesses the risks of persistently higher gas prices. Not all countries have the fiscal space for continued subsidies for energy consumption if high prices endure, and all governments must ultimately rein in such subsidies and switch to providing support for clean energy investment in order to meet emissions reduction goals. More financial solidarity between member-states, in the form of common borrowing and lending, transfers from richer countries to poorer, and joint green investments would help to make the energy transition possible. Energy ‘solidarity’ has become a buzzword in the past few months, as EU countries contemplated the possibility of facing gas shortages and thus being forced to share existing stocks. The mild winter meant emergency gas sharing was not needed, but the shift away from Russian energy imports and fossil fuel dependence more broadly continues to be urgent. It is time to discuss the role of financial and fiscal solidarity in advancing the decarbonisation of the EU energy sector and in ensuring energy security in Europe for the years to come.

How to handle energy shocks

Russia’s invasion of Ukraine has led to a negative terms of trade shock for EU countries. In economics jargon, the terms of trade reflect the ratio between the prices a country pays for imports and the prices that country receives for its exports. When import prices rise, and export prices remain the same, countries become poorer at least in the short term. There is little that governments can do to ease the immediate impact, apart from seeking to smooth out the shock for households through temporary income support, and trying to distribute the costs fairly, so that poorer people’s incomes are more protected than those of the rich.

European governments have mostly protected household incomes through the energy crunch by subsidising their energy consumption.

In the past year, EU imports of Russian natural gas have sharply dropped. This has been caused by Russia’s weaponisation of gas supplies, with Gazprom cutting pipeline gas flows, and by the EU’s determination to reduce Vladimir Putin’s revenues. Europe has had to turn to alternative gas suppliers to meet its demand: because gas imports via ship are more expensive than pipeline gas, Europe’s gas import costs have risen. Higher gas prices have fed into electricity prices, because gas power plants determine them at times of high power demand.1 And those high energy prices have pushed up inflation across the economy, alongside high import prices for goods, thanks to the global supply chain disruptions, which started during the Covid pandemic and persist because of the war in Ukraine.

So far, European governments have mostly protected household incomes by subsidising their energy consumption. This entails government borrowing, which means that future taxpayers are subsidising today’s consumption. In some ways, this is a legitimate policy: if households and businesses could not afford their bills they would be forced to cut back on their spending, and a deep recession would ensue, with high levels of unemployment and many poorer people being thrown into destitution. Support is best targeted on lower-income households to prevent energy poverty, because they spend a higher proportion of their income on energy. Additionally, they are most vulnerable because they are the most likely to be made unemployed in a recession and may not have savings to stay afloat.2 By smoothing out the price shock, governments allow the economy to adjust to higher prices with smaller rises in unemployment. But if imported energy prices remain permanently higher, governments should not sustain this policy for two reasons.

The first is that these subsidies are extremely expensive. In time, fiscal limits would be reached, and governments would struggle to manage increasingly unserviceable debt costs. Second, the best way for the European economy to adjust to higher imported gas prices is to reduce the volume of imports and find alternative sources of energy. That would lessen the terms of trade shock, by reducing the money spent on imports. As governments have lowered energy prices, however, they have lessened the incentives to invest in energy efficiency and alternative energy sources.

As well as allowing the price signal to stimulate private investment, governments can also invest themselves to help accelerate cuts to fossil fuel imports and foster renewable energy generation. They can subsidise energy efficiency measures like heat pumps and insulation, especially for poorer households, and guarantee prices or returns for low-carbon and investment-intensive energy generation such as nuclear and renewables, to encourage power companies to build new plants. Regulation matters too: faster permitting for wind and solar farms, and mandates for landlords and homeowners to insulate their properties are needed. Government borrowing is the best way to fund this investment, because it leads to permanently lower energy costs, which in turn allows citizens and businesses to buy other goods and services, increasing tax revenues.3

In sum, the ideal policy response to the energy crisis is to temporarily subsidise energy consumption, slowly let retail energy prices rise in line with global gas prices to allow price signals to encourage lower demand and changes in the energy mix, and to ramp up public and private investment in alternatives to Russian energy imports.

Why higher gas prices are here to stay

Despite gas prices falling from their August peak, European governments must avoid the temptation to declare victory, and take further action to reduce energy costs. European governments and the EU deserve praise for their success in reducing gas consumption and finding alternatives to Russian gas throughout 2022: Europe has cut its gas imports from Russia significantly: in the third quarter of 2022, Russian pipeline gas imports were down over 70 per cent year on year.4

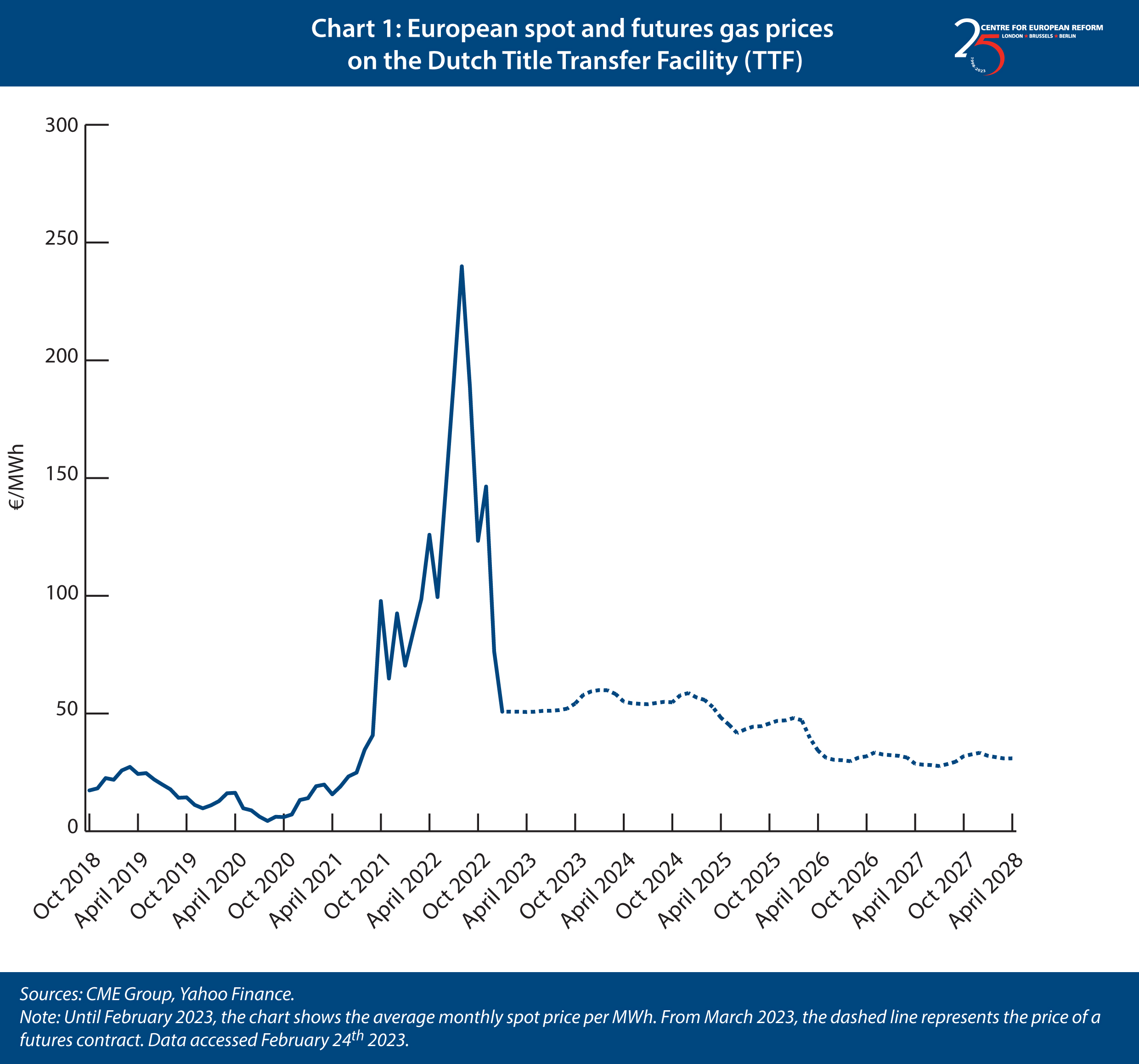

Fears that rationing would be needed this winter have proved misplaced, in part thanks to a mild winter. But gas prices are likely to be higher than pre-invasion levels for many years to come. The price of a megawatt hour (MWh) of natural gas has fallen from €240 in summer 2022 to €75 in January 2023. But that is nearly four times the pre-pandemic level, and contracts for future supplies of gas are currently trading at multiples of the pre-pandemic price, too (see Chart 1).

There are some reasons to worry that gas prices might rise again and remain structurally higher than before the war (although these worries should be reflected into futures prices in Chart 1). Continued lockdowns during 2022 meant that Chinese LNG imports fell, but now that China has abandoned its zero Covid policy, demand is likely to rise. A colder winter in 2023-24 might also mean gas storage is depleted faster than during the relatively mild winter of 2022-23. While it looks more likely than not that Putin’s attempt to turn Europe’s heating off has failed, investors think that gas supply to Europe will be more expensive without Russian imports. That is because shipping gas is less efficient than transporting it through a pipe. Russia is planning a new pipeline to transport more gas to China now that it has halted gas supplies to Europe, with construction to begin in 2024.5 That may somewhat reduce LNG prices globally, because China is a major importer, but Europe will continue to pay a premium for buying a substantive share of its gas as LNG.

This has obvious implications for Europe’s industrial competitiveness. Gas prices in the US are two to three times lower than in Europe.6 Without more investment to improve energy efficiency, lower power prices and develop cheaper alternatives to imported gas for industrial uses, energy-hungry companies could lose global market share to US competitors or shift their production outside Europe. At the same time, the EU also fears an exodus of clean tech production to the US, which aims to attract such investments with its recently approved subsidies in the Inflation Reduction Act (IRA – see below for further discussion).

How have European governments responded to the crisis so far?

Despite the likelihood that gas prices will remain higher than before the pandemic and Putin’s invasion, in the past year European governments have spent much more on subsidising energy than on finding cheaper and low-carbon energy alternatives. In the analysis below, we examine how much European governments have spent on three broad categories of interventions in response to energy price spikes:

- Price mitigation measures, which reduce retail energy prices. Examples are cuts to energy taxes and price caps.

- Income support measures, which are policies to support household and businesses’ incomes, such as cash transfers, tax credits and vouchers. These can be explicitly aimed at compensating households or businesses for higher energy costs, or broader measures to address the cost-of-living crisis, such as more generous social security transfers.

- Investment support measures, which are incentives for investments that can reduce reliance on expensive energy sources, particularly natural gas, to reduce consumers’ exposure to high prices and cut their energy bills. Examples are investments in energy efficiency, such as building renovations, and in energy grid infrastructure to support more renewables.

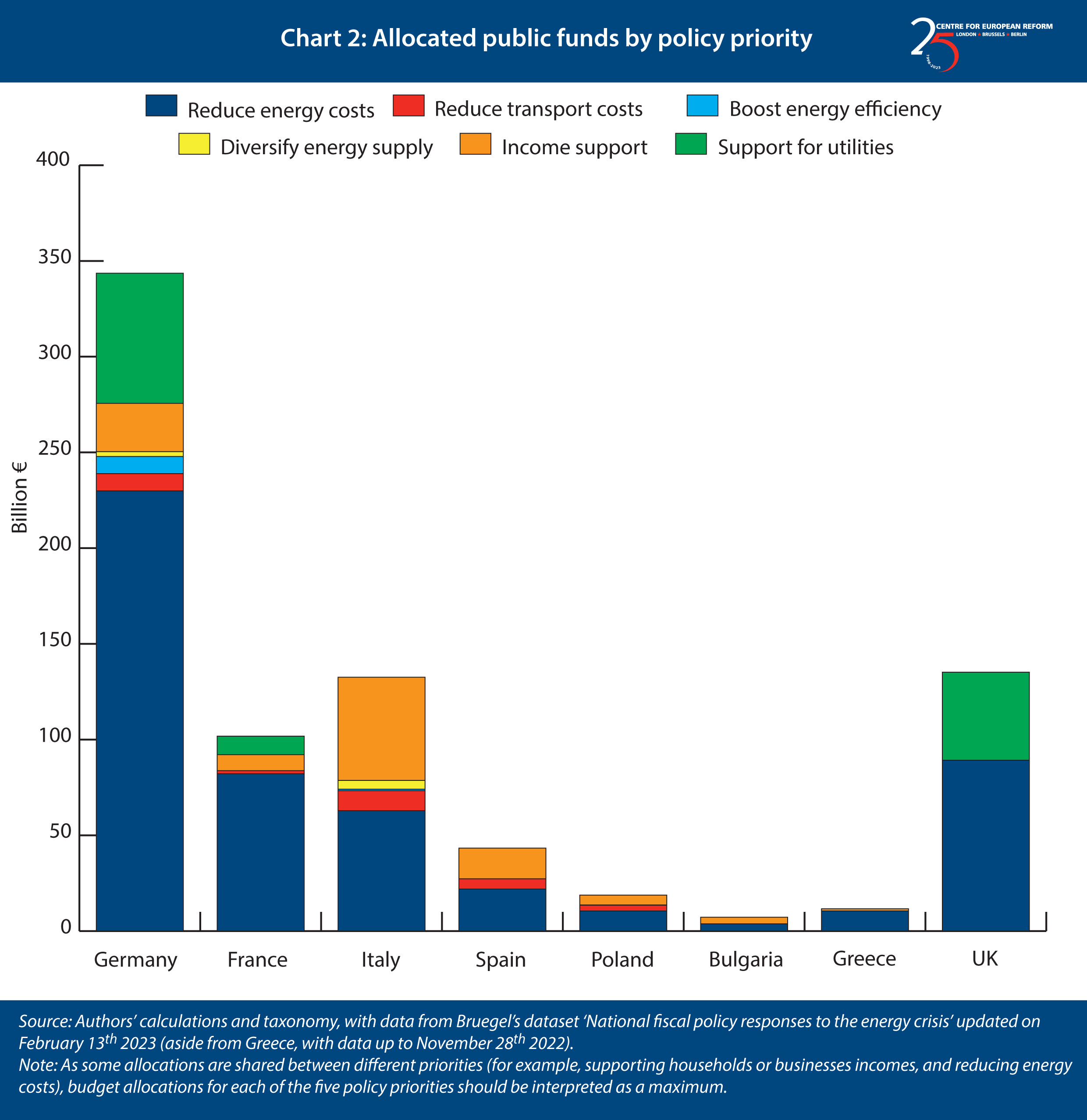

Most public funding has been spent on measures to keep the cost of energy and, to a lesser extent, transport in check, and to support household incomes. Some countries, such as Germany, France and the UK, have intervened with public funding to prop up or even nationalise energy utilities in need. Measures to support investment to boost energy efficiency are trailing by comparison. For example, in Germany, measures to reduce retail energy costs have absorbed ten times as much funding as energy efficiency investment. Chart 2 reports data from selected European countries.

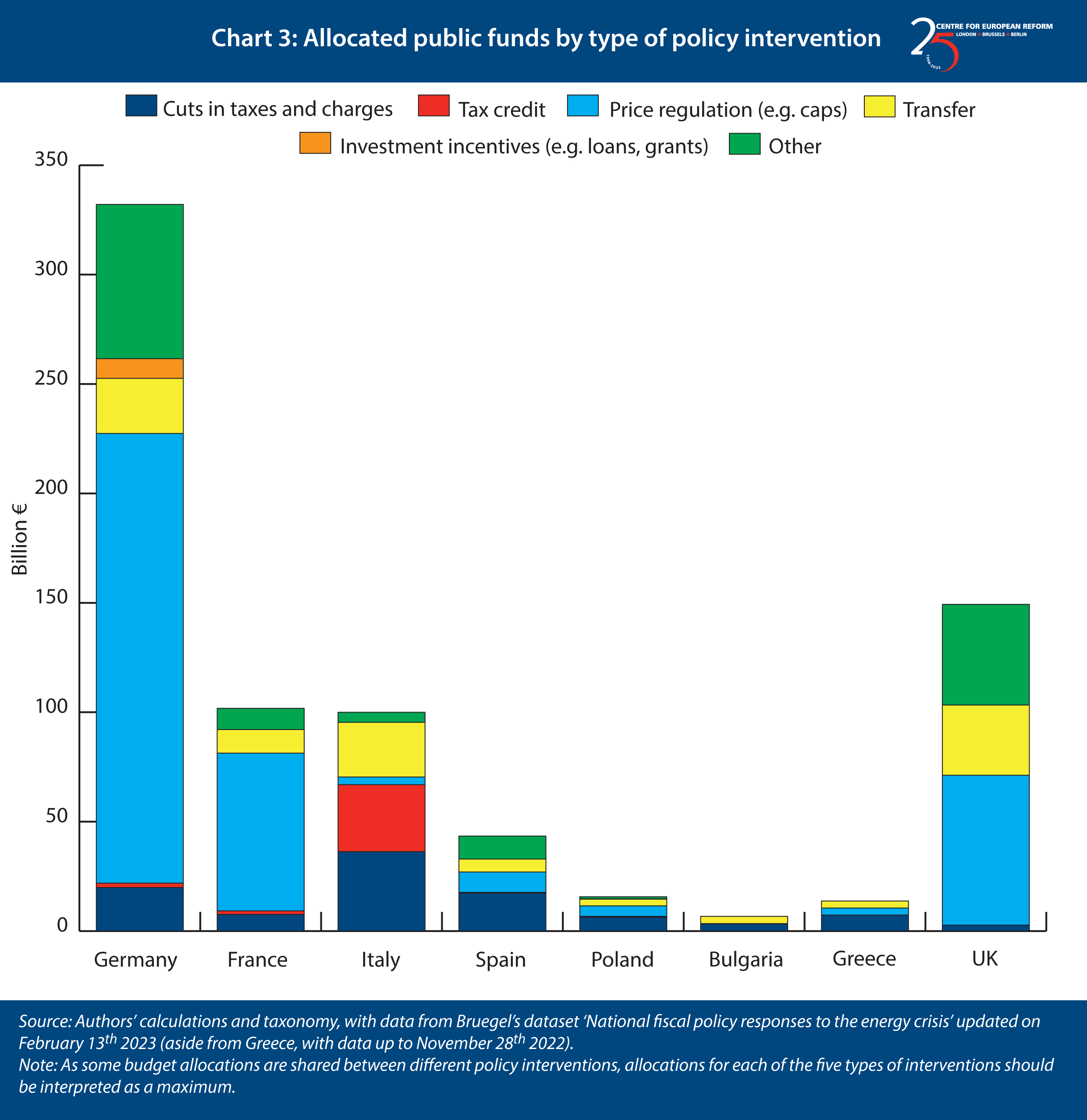

Governments have favoured price mitigation measures – such as price caps and freezes of regulated energy tariffs – which suppress energy price increases for all. These measures tend to be inefficient and regressive – compared to income support measures, such as cash transfers (Chart 3). Price mitigation measures include price caps and freezes of regulated energy tariffs. Many governments have cut VAT and excise duties on gas, electricity and motor fuels, alongside cuts to other energy charges (such as those covering transmission costs). This approach has been criticised by the IMF, among others.7 Cutting energy taxes is regressive because it reduces energy prices for all consumers, including high-income consumers who can shoulder higher prices. It is also ineffective, because curbing energy prices blunts incentives to save energy. Lump-sum transfers would be better because they preserve incentives to save energy. Targeting the transfers on lower-income consumers would restrict the support to those who really need it, while keeping government spending down.

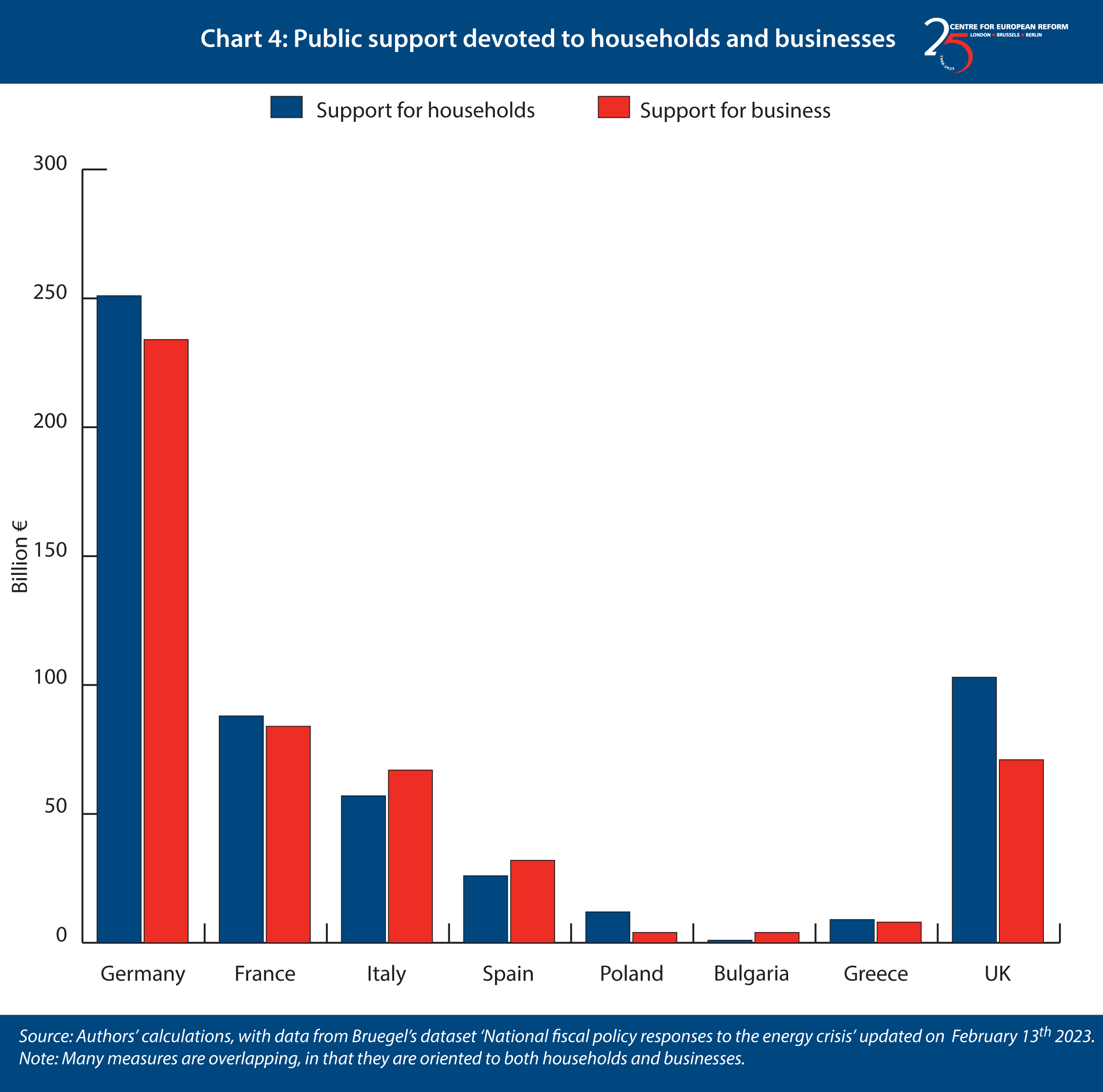

Large spenders like Germany and France have devoted similar support to households and businesses, while still being slightly more generous towards the former. Italy and Spain have instead been relatively more supportive towards businesses. In countries with smaller public budgets, trade-offs are more visible: Poland spent substantially more on household support, while Bulgaria did the opposite. While charts represent allocated funding as opposed to verified spending, it is clear that Germany has the potential to vastly outspend other major EU member-states with its emergency support measures (Chart 4).

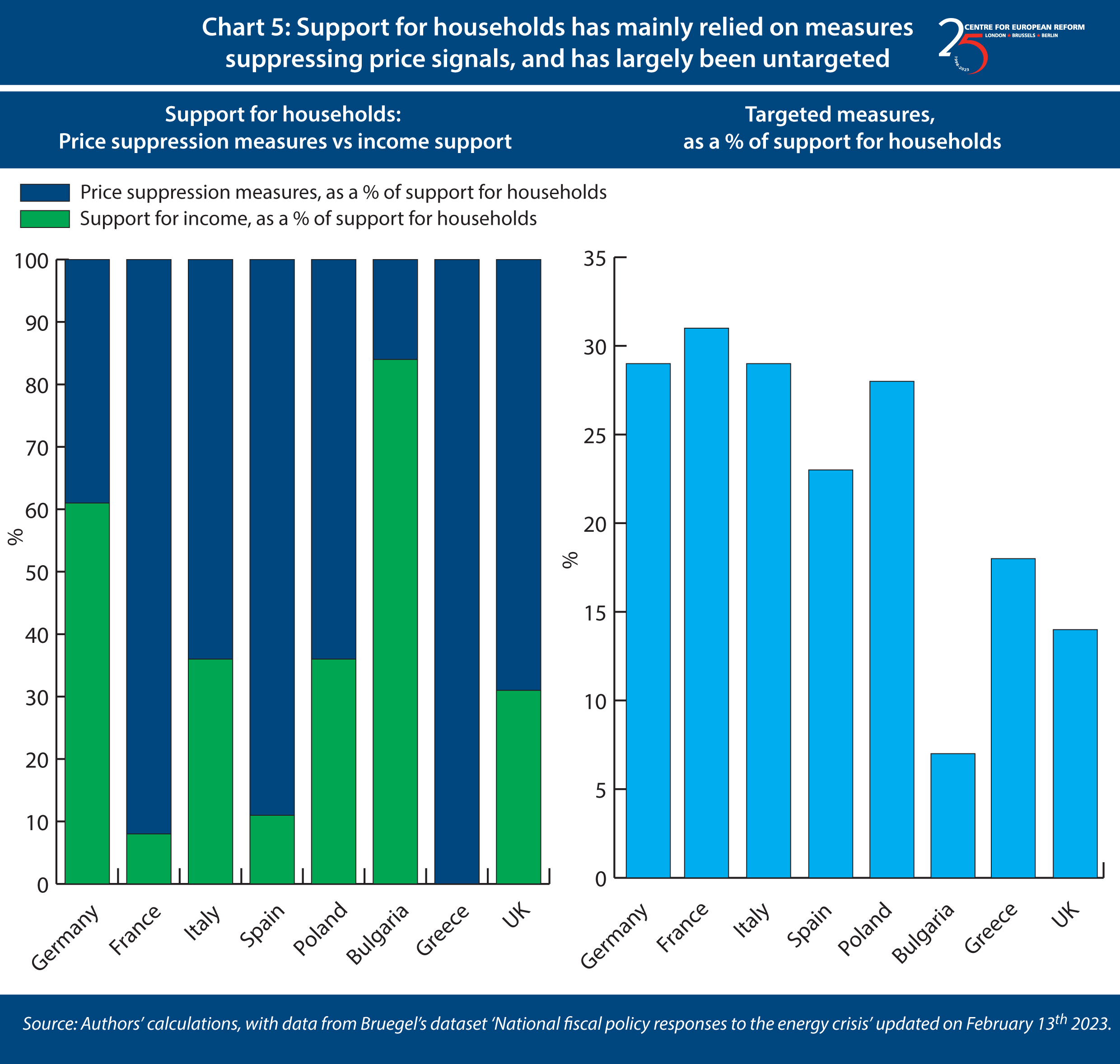

Chart 5 shows that governments have favoured measures for households that suppress prices, such as tax cuts, price caps or tariff freezes, rather than income support measures such as cash transfers to households. Regrettably, only about a third of measures supporting households have been targeted, most frequently based on income: this means that a large share of public money spent on household income support may have gone to people that did not necessarily need it. While this may have been necessary to roll out these support schemes as quickly as possible amidst the energy crunch, in the future, support schemes should be redesigned to target the most vulnerable, to make the best redistributive use of limited public funds, as called for by several observers.8

Governments’ generous tax reductions on energy and fuels starting in autumn 2021 were initially prompted by the conviction that the price spike would be short-lived, and that this would be a quick and simple way to help households and businesses. But there are now signs that governments are realising how costly these subsidies will be, with high energy prices likely to be persistent. For example, the Italian government has recently ended its discount on fuel excise taxes (€0.18 per litre), which cost about €1 billion per month.9

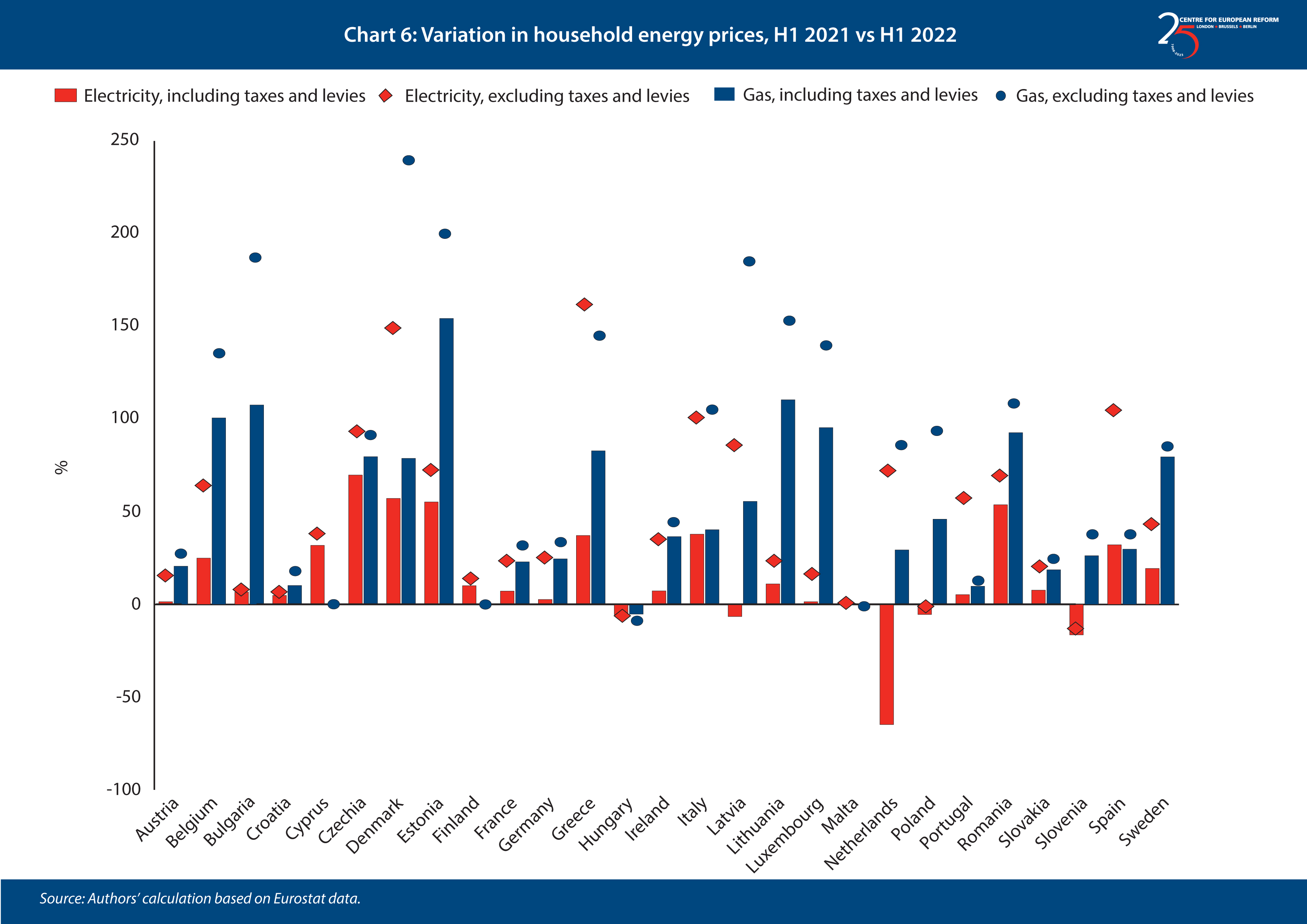

Chart 6 shows the rise in household electricity and gas prices between the first half of 2021 and the first half of 2022. The dots show prices before government interventions curbing energy taxes, and the bars show prices afterwards. Almost all governments have significantly cut prices for households.

Investment in REPowerEU: An appraisal

The government policies discussed in the previous section treated the spike in energy prices as a temporary shock. But energy prices will remain structurally higher than pre-pandemic levels in the near future. Accelerating the energy transition, which can curb both dependence on Russian energy imports and energy-related emissions, requires investment. In its REPowerEU plan, the Commission estimates that to get rid of Russian fossil fuel imports by 2027, €210 billion of additional investment by 2027 (and €300 billion by 2030) are necessary. These come on top of investments required by the Fit for 55 climate action plan to achieve Europe’s 2030 emissions targets. At the same time, by making energy demand more efficient and energy supply greener and more diversified, REPowerEU investments aim to cut spending on fossil fuel imports by about €90 billion per year by 2030.10

Accelerating the energy transition, which can curb both dependence on Russian energy imports and energy-related emissions, requires investment.

With this in mind, three medium-term priorities have emerged in EU and national energy policy to ensure fast cuts to Russian gas imports. These are investing in LNG regasification capacity and gas and power grid infrastructure; simplifying permitting regulation to accelerate the deployment of renewable energy; and boosting investments in energy efficiency. The first two aim to diversify energy supply from Russian gas. The third and most important aims to reduce energy demand and, with it, fossil fuel imports and emissions, without harming economic output.11

To diversify their gas supply, Northern European countries have made some big investments in LNG. Installations of ‘temporary’ terminals for the regasification of LNG are proceeding at record speed to allow countries previously reliant on pipeline gas imports from Russia’s Gazprom, such as Germany, to purchase LNG from other suppliers. After a decade of modest expansion, LNG regasification capacity in the EU and UK is set to increase by 34 per cent between 2021 and 2024. With new regasification terminals expected to start operations in seven EU countries, additional LNG capacity is expected to reach about 36 billion cubic metres (bcm) by the end of 2023. This amounts to about a quarter of the 155 bcm of gas that the EU imported from Russia in 2021.12

The EU as a whole has increased imports in pipelined gas from Norway, Algeria and Azerbaijan.13 This change in import patterns, together with record levels of LNG imports and substantive cuts to gas consumption in response to high prices, have helped secure gas supply against lower imports from Russia.14

To accelerate renewable energy deployment, the REPowerEU plan requires EU governments to simplify the bureaucratic procedures for the installation of renewable energy capacity. More permits for renewables installations, together with the increased cost advantage of renewables against a backdrop of high gas prices, has prompted the International Energy Agency to revise its forecasts of renewables investment upwards: it expects capacity in renewables in Europe to expand by 60 per cent in 2022-2027 (or by 425 GW), double the growth rate of the previous five years.15

The Commission estimates that in 2022-2030, an additional €56 billion should be devoted to investments in energy efficiency, including building retrofits and deployment of heat pumps, just over €6 billion on an annual basis, to speed up the electrification of heating and reduce the role of gas in this sector. That comes on top of the €190 billion in estimated necessary investments to deliver on pre-set 2030 energy efficiency goals, of which €115 billion are needed in the residential sector and the remainder for business and industrial efficiency.16

Investment in energy efficiency flatlined in Europe between 2014 and 2019.

But investment in energy efficiency flatlined in Europe between 2014 and 2019.17 Building renovation rates in Europe are around 1 per cent of building stock per year, but only one-fifth of that (0.2 per cent) pertains to deep renovations that cut energy consumption by at least 60 per cent. Renovation rates should reach 2 per cent by 2030, with a higher share of deep renovations, to meet the EU’s ‘Renovation Wave’ target.18 However, incentives for energy efficiency investment in 2023 budgets have not equally increased across the EU (see also Chart 2 above):

- Among countries that have prioritised energy efficiency within emergency measures, Poland for example has earmarked only €131 million for subsidies for the purchase and installation of heat pumps in housing, a booming market. This is about 1 per cent of the total Polish emergency spending measures so far.

- Germany has only earmarked €9 billion of its €264 billion emergency package of 2022 to support for energy-intensive businesses in their energy efficiency investments. As part of its Climate and Transformation Fund, Germany announced in August 2022 an increase in funding for investment incentives for energy efficiency and renewables in buildings to €17 billion in 2023, or by 75 per cent relative to 2022.19 Funds for energy efficiency in industry and commerce have about doubled to over €800 million.

- France has increased its budget for energy efficient housing renovations, including via the incentive scheme MaPrimeRenov, to €3 billion in 2023. Specifically, this will translate into more generous grants for households upgrading their heating systems.20 That is about 4 per cent of the amount it spent on emergency measures for households and industry in 2021-2022.

- Spain has allocated €200 million to energy efficiency investments in the tertiary and industrial sectors.21 This is about 3 per cent of the €6.3 billion necessary to finance the Iberian gas price cap.

- Italy has reduced the generosity of its Superbonus incentive for building renovation: applicants will be reimbursed 90 per cent of incurred expenses as opposed to 110 per cent, and will essentially have to pay renovation costs out of pocket to then claim them back as a tax credit.22 The scheme was a stimulus measure after the Covid crisis and was largely untargeted, including both energy efficient renovations and other construction works. It has absorbed an estimated €72 billion in public funds between 2020 and January 2023, allowing households of all income levels to obtain access to the same levels of incentives. The latest reform de facto limits the scheme’s applicability to households with a high enough income to pay for the renovation ex ante themselves and claim the entire tax credit.23

These examples indicate that public spending on energy efficiency remains orders of magnitude below energy subsidies allocated in the past year. Furthermore, public subsidies for energy efficiency are not always targeted on households and businesses that would need them most, or on buildings that would most benefit from deep renovations.

However, the speed of uptake of heat pumps in Germany and Poland shows that, if well-designed, appropriate incentives can convince consumers to undertake structural changes in their homes to shift away from fossil-fuelled heating.24 This signals the enormous potential for energy efficiency measures.

Is REPowerEU funding big enough?

REPowerEU amounts to an accelerated decarbonisation programme, which requires big rises in public and private investment. Before Russia’s invasion, the European Commission estimated that meeting the EU’s emissions reduction target for 2030 – a cut of 55 per cent relative to year 1990 – would entail €1,000 billion of public and private investment a year, including in transport.25 The European Investment Bank reckoned that the additional public and private investment needed to meet the target was about €300 billion.26 And Claudio Baccianti, a researcher at the Agora Energiewende think-tank, reckons that the required additional public investment by the EU and its member-states would be around €250 billion a year – which amounts to 1.8 per cent of EU GDP.27

The Recovery and Resilience Facility (RRF) – the core piece of the EU pandemic recovery fund – was agreed before the Ukraine war and has helped member-states fund about a tenth of the €250 billion energy investments they have to make by 2026 to meet the 55 per cent target. The RRF will provide member-states with €340 billion in grants and €385 billion in loans by the end of 2026, funded by joint EU borrowing, one-third of which have to be spent on the green transition by then. All 27 member-states took up the grants that were made available to them – some did not take up the loans – and their annual spending on green transport, energy efficiency, renewables, grids and other climate mitigation financed by the RRF will be about €23 billion to 2026.28 This is significant but only a fraction of the estimated additional investment that is necessary to meet 2030 climate goals.

Government borrowing costs have been rising as EU inflation has spiked, and some governments’ balance-sheets are feeling the strain.

The European Commission recognises that more EU money would be helpful, since the REPowerEU plan calls on member-states to act together, but largely in a voluntary way. Government borrowing costs have been rising across the EU as inflation has spiked, and some governments’ balance-sheets are feeling the strain after subsidising household energy costs. When Germany announced that it would allocate over €200 billion to fund measures countering the energy crunch, other member-states complained that its largesse would distort the single market by giving German companies a competitive advantage. The EU will provide €225 billion in RRF loans that member-states had not taken up to fund the plan, with an extra €20 billion funded from sales of emissions trading scheme permits. Member-states are currently drawing up REPowerEU addendums to their Recovery and Resilience Plans to show how they would spend the extra cash. Once the Commission approves them, they can borrow the money from the EU.

The problem with this plan is that grants are better than loans for poorer and highly indebted governments. RRF grants will be paid for by the EU collectively, with member-states funding the EU’s repayments to bond investors according to the relative size of their populations and level of national income over time. That means that the transfers involved are larger than loans, which, on the other hand, are beneficial to governments only if the EU’s cost of borrowing is lower than their own. The EU loan is added to their stock of debt, and they must finance the repayments themselves.

It is possible to make a stylized estimate of how much subsidy different member-states will receive from the REPowerEU loans. This can be done by:

- taking the difference between their cost of borrowing and that of the EU (the ‘spread’),

- applying, as a proxy, how much lending they would receive if the loans were shared as the RRF grants have been, and

- calculating how much they will save in their repayment to investors from borrowing via the EU rather than nationally.

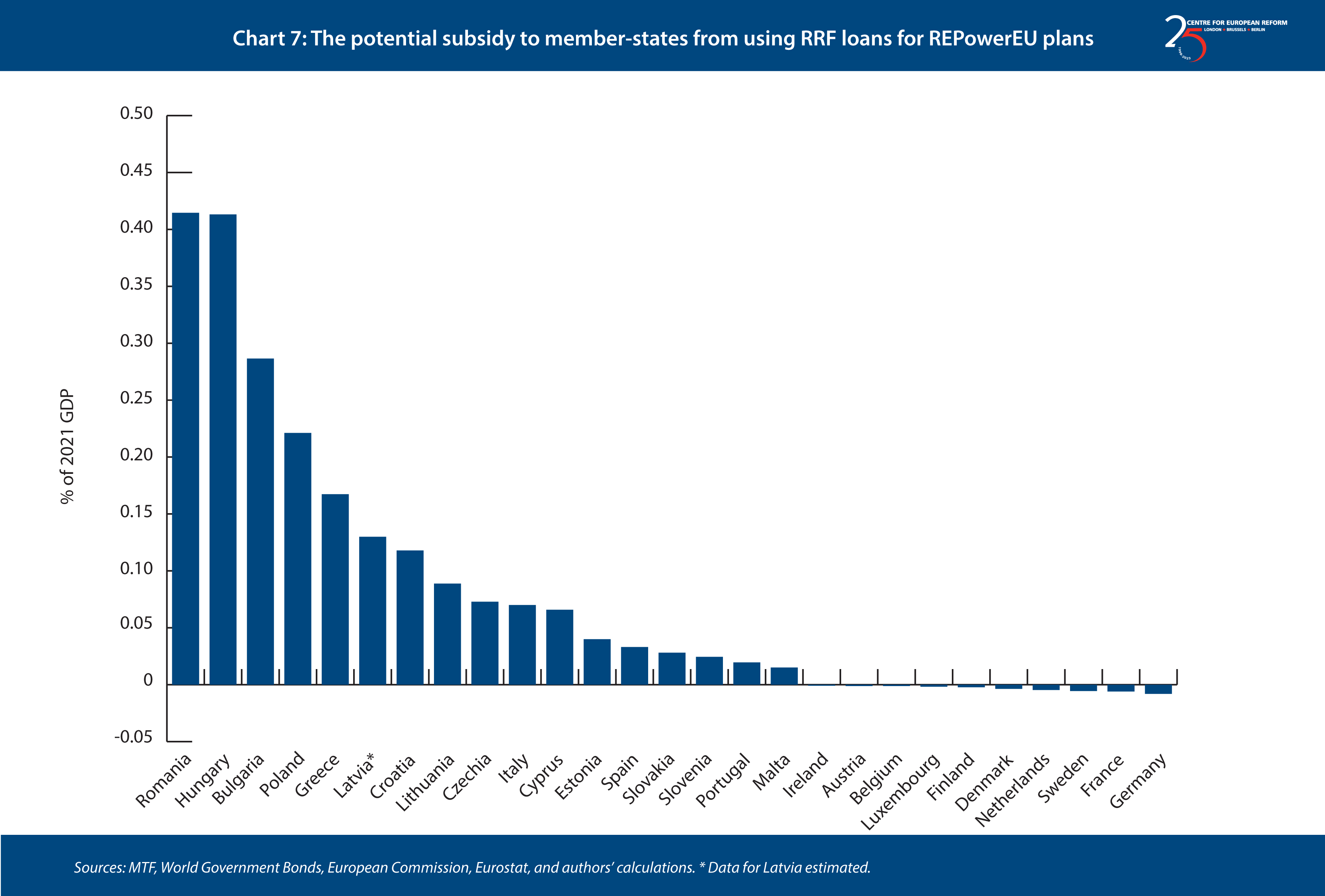

The results are shown in Chart 7. The overall subsidy for the entire EU-27 amounts to €24 billion by 2026 – or €6 billion a year – far smaller than the €225 billion in borrowing, because the EU’s collective cost of borrowing is not wildly different from that of the member-states, on average. That is not nothing, and some member-states would do well: Romania and Hungary, which are both struggling with high government borrowing costs, would receive around 0.4 per cent of GDP in loan subsidy a year to 2026. Bulgaria and Poland would receive between 0.2 and 0.3 per cent. However, the sums involved are far smaller than the EU’s public investment needs. It should be noted that, because we assume that REPowerEU loans are distributed in the same way as RRF grants, some countries with relatively high GDP per capita but also higher borrowing costs like Spain seem to benefit less, although they may in practice receive a larger share of the loans.

To sum up, the REPowerEU plan requires member-states to accelerate climate investment. The extra public investment needs for the EU-27 are estimated to be large – about €250-300 billion a year until 2030. The RRF has already provided around €23 billion of that through grants and loans. The additional subsidy through the additional lending will be around €6 billion a year. Thus, on current plans, the extra money the EU will collectively provide for ending dependence on Russian energy is small, and a large gap remains.

To raise the money available for subsidies, the EU has two choices. It could either borrow much more on the markets and pass those loans on to member-states, whose repayment would be proportional to the size of their loan. Or it could borrow smaller sums but give them as grants to poorer or more indebted member-states, with repayment being tied to the relative size of economies when the EU bonds mature. The latter option would be more progressive. As things stand, REPowerEU financing will only marginally speed the EU’s transition from fossil fuel imports.

Conclusion

As energy prices have fallen from last autumn’s highs, the European debate has shifted from energy costs onto the race to produce green technology. EU member-states are divided on how to respond to the IRA, with France and Italy pressing for EU-level subsidies for green tech, to which the Netherlands and the Nordics are opposed. Germany has hinted that the EU budget might be used to fund subsidies, perhaps in the knowledge that reopening the delicate compromises in the budget is unlikely.

The opponents of subsidies are right to be sceptical. The biggest factor undermining the competitiveness of European industry is relatively high energy costs, which will persist without state intervention. Industrial policy is more likely to be successful if support is broad-based, rather than targeted towards particular businesses or technologies. The US has designed the IRA subsidy package as its main strategy to accelerate climate investment. The EU instead has carbon pricing – which the US lacks at the federal level – and stringent emissions targets, which are more likely to be effective than subsidies in ending the use of fossil fuels. The problem is that ending Russian fossil fuel imports has raised the cost of energy in the short term and requires the EU to hasten decarbonisation. A faster shift away from expensive fossil fuels would also help European industry – including the manufacturers of electric vehicles (EVs), renewables and energy efficient appliances – to regain competitiveness.

Financing investments for the energy transition, from renewable electricity capacity to grid expansion to energy efficient renovations, must be one the EU’s biggest priorities over the next decade. All these are investments in a public good, as they will contribute to reducing Europe’s energy imports and carbon emissions. For this reason, these projects deserve cross-border co-ordination and joint financing at the EU level.

It is time to integrate the EU’s energy policy further, and to accompany this process with a serious fiscal infrastructure.

It is best to plan large-scale investments at the EU level for cost, efficiency and strategic reasons. First, cross-border investments can be most cost-effective if planned centrally. National energy decisions have spillover effects beyond borders, as shown by Germany’s decision to build the NordStream pipelines, and the Union should not let national energy policy damage its energy security again. Second, the energy crunch has led EU governments to agree to more centralised EU-level energy policy decisions, such as binding targets for gas storage, and voluntary targets for energy savings. This type of co-ordination should continue beyond the crisis. But if more energy policy decisions are taken at the EU level, this will increasingly lead to a mismatch between EU-level decisions and national-level spending, violating the principle that spending decisions and revenue-raising should be undertaken at the same level of government.

The urgent need to accelerate investment in projects for the energy transition requires not only collective borrowing, but also more co-ordinated investment on projects like interconnectors (power grid, gas and hydrogen pipelines), and large-scale renewable energy plants. This is slightly different from the approach spearheaded by the Recovery and Resilience Facility (RRF). The RRF involves joint borrowing but no central planning of investments, which are decided at national level based on EU guidelines. The EU needs a dedicated climate and energy fund, modelled on RRF, with EU grants funded by joint borrowing, to ensure that poorer and more indebted countries can easily fund the required investment. NGEU and REPowerEU financing together provide around €30 billion a year to EU member-states for energy-related spending, and that money will run out in 2026.29 Because the estimated investments needed to meet 2030 climate goals are around €1,000 billion of public and private investment a year, to fundamentally shift the pace of Europe’s energy transition, a new EU climate fund would need to be several times larger than the €30 billion a year that REPowerEU funding represents.

It is time to integrate the EU’s energy policy further, and to accompany this process with a serious fiscal infrastructure: to finance this type of investments, the EU needs higher, dedicated revenues, as opposed to promises by member-states to pay more in the future.

At present, it is not clear how EU borrowing will be repaid. Various measures have been proposed but not agreed, such as revenues from the emissions trading scheme or a carbon border tax, or a form of common corporate tax. The lack of clarity on repayment might be why the EU’s borrowing costs are higher than those of Germany and France.30 EU-level funding might also avoid a subsidy race in response to the IRA: if wealthier member-states splurged on state aid to attract investment, the single market could splinter.

Europe has led the world in cutting emissions, but Russia’s invasion of Ukraine means it must build a net-zero energy system more quickly. A common energy policy, backed by the EU’s collective fiscal firepower, would allow it to do so.

2: Balint Menyhert, ‘The effect of rising energy and consumer prices on household finances, poverty and social exclusion in the EU’, European Commission Joint Research Centre, October 2022.

3: John Springford, ‘In defence of borrowing for climate action’, CER, October 13th 2022.

4: European Commission, Market Observatory for Energy, DG Energy, ‘Quarterly report on European gas markets’, Vol. 15 issue 3, covering third quarter of 2022.

5: Euractiv, ‘Russia says pipeline to China will replace Nord Stream 2’, September 16th 2022.

6: Politico, ‘Why cheap US gas costs a fortune in Europe’, November 15th 2022.

7: David Amaglobeli et al, ‘Fiscal policy for mitigating the social impact of high energy and food prices’, IMF note, June 7th 2022.

8: Giovanni Sgaravatti, Simone Tagliapietra and Cecilia Trasi, ‘The fiscal side of Europe’s energy crisis: The facts, problems and prospects’, March 2nd 2023.

9: Il Post, ‘Il “decreto carburanti”, infine’, January 14th 2023.

10: European Commission, ‘Implementing the REPowerEU action plan: investment needs, hydrogen accelerator and achieving the bio-methane targets’, May 18th 2022.

11: Elisabetta Cornago, ’Europe may not find energy efficiency sexy – but it’s crucial’, Financial Times, December 13th 2022.

12: US Energy Information Administration, ‘Europe’s LNG import capacity set to expand by one-third by end of 2024’, November 28th 2022.

13: Symon Kardaś, ’Conscious uncoupling: Europeans’ Russian gas challenge in 2023’, European Council on Foreign Relations, February 13th 2023.

14: European Commission, Market Observatory for Energy, DG Energy, ‘Quarterly report on European gas markets’, Volume 15, Issue 3, covering third quarter of 2022.

15: IEA, ‘Renewables 2022: Analysis and forecast to 2027’, December 2022.

16: European Commission, ‘Identifying Europe’s recovery needs’, May 27th 2020.

17: European Investment Bank, ‘Investment report 2020/1: Building a smart and green Europe in the Covid-19 era’, January 2021.

18: European Commission, ‘A Renovation Wave for Europe - greening our buildings, creating jobs, improving lives’, October 14th 2020.

19: Deutscher Bundestag, ‘Investitionen aus Klima- und Transformationsfonds steigen’, August 15th 2022.

20: Ministère de l’Économie, des Finances et de la Souveraineté industrielle et numérique , ‘Projet de loi de finances 2023’, September 26th 2022.

21: Ministerio para la transición ecológica y el reto demográfico, ‘El Gobierno aprueba un Plan de ahorro y gestión energética en climatización para reducir el consumo en el contexto de la guerra en Ucrania’, August 1st 2022.

22: Ministero dell’economia e delle finanze, ‘Le principali misure della manovra 2023’, December 29th 2022.

23: Il Post, ‘Come è cambiato il superbonus’, February 20th 2023.

24: Politico, ‘Putin’s war accelerates the EU’s fossil fuel detox’, October 12th 2022.

25: European Commission, ‘Stepping up Europe’s 2030 climate ambition: Impact assessment’, September 2020.

26: European Investment Bank, ‘Investment report 2020/1: Building a smart and green Europe in the Covid-19 era’, January 2021.

27: Claudio Baccianti, ‘The public spending needs of reaching the EU’s climate targets’ in ‘Greening Europe: 2022 European public investment outlook’, December 2022.

28: Authors’ calculations, based on data in European Commission, ‘Recovery and resilience scoreboard, Green transition pillar: Breakdown of expenditure supporting the green transition per policy area’. These are the shares of grants and loans that the EU-27 have taken up and committed to spend on sustainable mobility, energy efficiency, renewable energy and networks, and other investments for climate change mitigation.

29: Elisabetta Cornago and John Springford, ’Why the EU’s recovery fund should be permanent’, CER policy brief, November 2021.

30: Giovanni Bonfanti and Luis Garicano, ’Do financial markets consider European common debt a safe asset?’, Bruegel, December 8th 2022.

Elisabetta Cornago is a senior research fellow and John Springford is deputy director of the Centre for European Reform.

March 2023

View press release

Download full publication