The EU emissions trading system after the energy price spike

- Before Putin’s invasion of Ukraine, the EU had planned to expand its emissions trading system (EU ETS) and strengthen the carbon price it generates. The economic recovery from the pandemic has led to an energy crunch, and war in Ukraine has contributed to increasing energy prices and complicated the politics of carbon pricing. This policy brief discusses how to make a higher and more comprehensive EU carbon price both effective and politically feasible.

- The EU’s existing ETS establishes a carbon price for heavy industry, electricity generation and intra-EU flights. However, to maintain the competitiveness of European industry, many emissions permits are handed out for free, which has so far dimmed the incentives for industries to cut CO2. Carbon emissions from road transport and building heating, so far excluded from the ETS, are priced unevenly across the EU, with energy and carbon taxes varying across countries.

- The EU’s Fit for 55 climate policy package aims to change this, strengthening the role of carbon pricing in the transition towards carbon neutrality by 2050.

- As part of this package, the European Commission has proposed a lower cap on emissions, to bring the ETS in line with tougher climate targets, and tighter conditions under which industrial plants can claim free permits. Free permits will be gradually phased out, while a carbon border adjustment mechanism (CBAM) will be introduced to level the playing field between the carbon price faced by EU and foreign producers. The Commission has also proposed that all ETS revenues that member-states receive should go towards climate investment.

- These reforms go in the right direction, but should be stricter and implemented more rapidly:

- A gradually increasing price floor, below which the price of emissions permits cannot fall, would provide investors with certainty of the direction of carbon prices.

- The current proposal envisions the full phase-out of free allowances in 2036, ten years after the CBAM’s full implementation. Scrapping free allowances for heavy industry by 2030 would force producers to innovate more quickly and would not make European industry less competitive.

- Member-states should devote ETS revenues to climate investment as planned – but more of that should go towards low-carbon innovation.

- The European Commission wants to introduce a new ETS (ETS2) covering emissions from road transport and buildings, where decarbonisation is lagging. This would impose a larger burden on poorer households and smaller businesses who cannot easily afford to insulate their home or upgrade to more energy efficient production processes. The EU wants to use part of the ETS2 revenues to help such vulnerable energy users and has proposed a Social Climate Fund (SCF) to do so, but it could do more:

- All revenues from the ETS2 should be devoted to the SCF.

- The Fund should start as soon as possible: it would provide a good EU-wide response to recent energy price spikes.

- The EU should clearly communicate that all revenues from ETS2 will be devoted to supporting citizens and businesses in the green energy transition. Without clarity on this link, popular support for carbon pricing may falter.

- A ‘price corridor’ for ETS2 carbon prices could help avoid excessive carbon price fluctuations. Households and small businesses are not equipped to deal with large fluctuations in their energy and fuel expenses.

- The EU should align all policies concerning road transport and buildings with climate targets: reform of the energy taxation directive is needed to remove energy subsidies (such as those for aviation) and to ensure that high energy taxes do not put electricity, which will become greener over time, at a cost disadvantage relative to fossil fuels.

In the EU, not all CO2 emissions are considered equal: heavy industry and electricity producers face an EU-wide carbon price under the EU Emissions Trading System EU (ETS), but road transport and the heating of buildings do not. All EU member-states tax fuel, but tax rates vary. And some member-states have their own national carbon taxes in addition to the ETS. This is about to change. In July 2021, the European Commission presented the ‘Fit for 55’ climate and energy package, a set of policies to cut carbon emissions by 55 per cent by 2030 relative to 1990 levels. The package proposes reforms to tighten the EU ETS cap on emissions from heavy industry and electricity generation, and to create a new scheme to put a price on carbon emissions from road transport and buildings.

Since 2005, the ETS has capped carbon emissions from over 10,500 installations in the European power sector and in energy-intensive industrial sectors such as oil refining, iron and steel, and cement. The cap covers about 36 per cent of total European emissions and is gradually tightened every year to reduce them.1 The cap is enforced via permits to emit, which are traded on carbon markets, leading to a price for carbon emissions. The problem is that, while the energy sector has cut its emissions by 15 per cent since 2005, the carbon price from the ETS has, so far, not driven down carbon emissions from heavy industry in a comparable way.

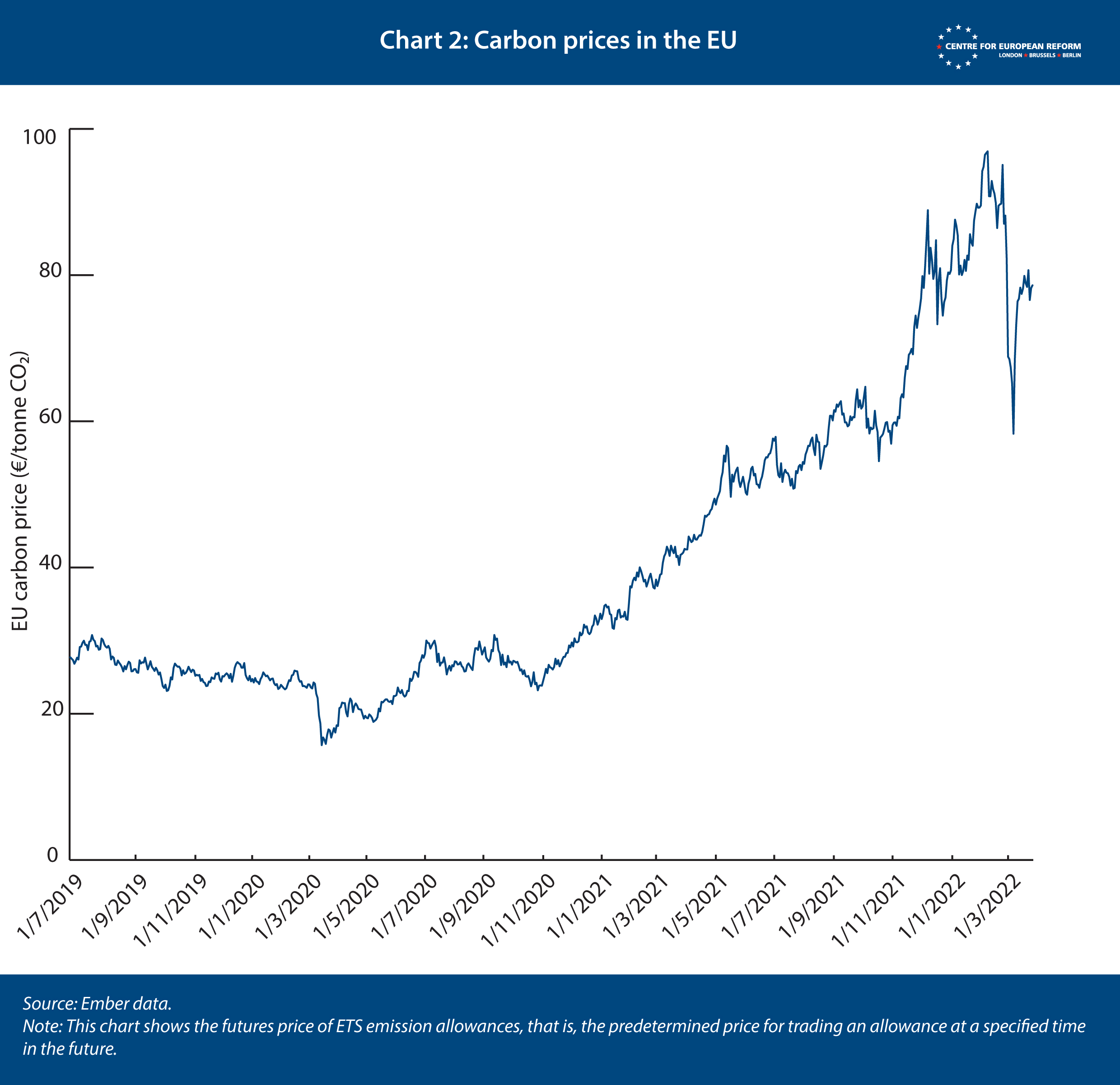

But prices on the European carbon market reached an all-time high of €100 per tonne of CO2 in early February 2022, as Europe’s climate targets – and its policies – have become more ambitious. That is a welcome change from the first 15 years of the EU ETS, when heavy industry found that emitting carbon was so cheap that reducing emissions was not worth the hassle. A carbon price with bite is a necessary tool to reach the EU’s climate goals. But a high price poses a challenge for Europe’s heavy industry, which competes globally with producers who are not (yet) subject to comparable carbon pricing.

The proposed ETS reform lowers the cap on emissions to bring the ETS in line with tougher climate targets. It also tightens the conditions under which industrial plants can claim free permits, paving the way for their gradual phase-out. This will be paired with the phase-in of a carbon border adjustment mechanism, which will charge importers of some heavy industry outputs to the EU a fee based on the EU carbon price, effectively levelling the playing field between domestic and foreign producers.

The other main policy change related to carbon pricing included in the Fit for 55 package is the proposal to introduce a new system to cap and trade carbon emissions from two major laggard sectors, road transport and buildings, which account for about 25 per cent and 15 per cent of EU-wide greenhouse gas emissions respectively.2

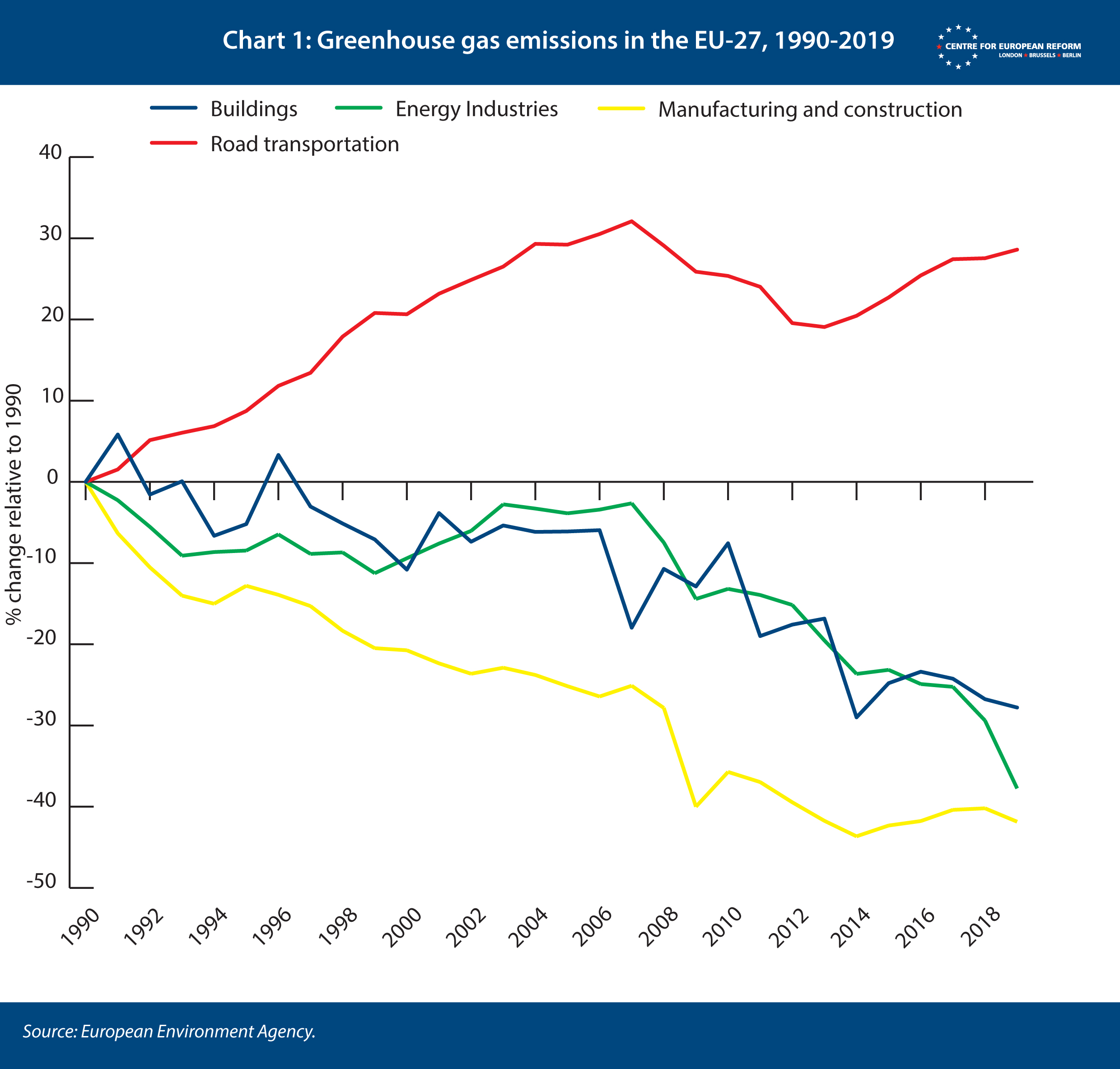

Manufacturing and energy industries, currently covered by the EU ETS, have cut greenhouse gas emissions since 1990 by about 40 per cent, while decarbonisation in the commercial and residential building sector has not been as fast, with emissions reductions below 30 per cent. However, emissions from road transport have increased by almost 30 per cent (see Chart 1). The new ETS aims to reverse this trend in transport emissions and accelerate decarbonisation in buildings, cutting combined emissions from these sectors by 45 per cent by 2030 relative to 2005 levels.

Eight months after the Commission made its ETS proposals, Vladimir Putin invaded Ukraine. This has massively raised the price of natural gas, which increased over five-fold from a year ago, and that of oil, up 50 per cent from a year ago.3 The European Commission and national leaders have called for an acceleration of the EU’s planned shift from fossil fuels to renewables: this would cut both emissions and the Kremlin’s revenues from energy exports to the EU. However, there are disagreements on the policies needed to do this: MEPs on the right and left are calling for the European Commission’s plans to expand carbon pricing to be shelved, and some member-states are also hesitant or openly against the plans.4

By strengthening and extending the ETS, the EU would be imposing sizeable costs on plants that emit a lot of carbon, and on households and small businesses that may struggle to invest in green heating and transport, in a period of higher energy prices. The energy price spikes arising from the post-pandemic recovery and the Ukraine war make decarbonisation both more essential and more politically fraught.

The next sections provide recommendations to strengthen the Commission’s proposals; to ensure that emissions trading and the ensuing carbon prices become a stronger driver of decarbonisation; and to ensure more support for poorer member-states, businesses and households to help them invest in green alternatives. The policy brief starts with a strategy to decarbonise heavy industry, then discusses how to deal with the fraught politics of extending the ETS to road transport and building heating, and concludes with reflections on the impact of the Ukraine war on the Commission’s proposals.

How the EU ETS can decarbonise European heavy industry

The reason why industrial decarbonisation has been slow in the EU is because between 2012 and 2018, carbon prices remained under €10 a tonne, in part because of a surplus of emission permits on the market, and in part because industrial installations under the ETS still enjoy free permits for carbon emissions. To prevent prices for carbon from falling too low, the EU recently created the so-called market stability reserve (MSR) to stash away the surplus of allowances that was flooding the carbon market. In effect, because the MSR is designed to withdraw or release allowances when the number in circulation goes below or above certain pre-defined thresholds, respectively, the ETS has become an unconventional cap and trade system. While generally cap and trade systems allow the price to fluctuate freely, the MSR introduces an indirect lower and upper bound on carbon prices.

The EU ETS should ensure a sufficiently high and stable carbon price

For a carbon price to provide an effective and predictable incentive for businesses, it has to be sufficiently high to make low-carbon technologies competitive with carbon-intensive ones, and it should not be too volatile.

As long as heavy industry is shielded from carbon prices, they can do precious little to prompt decarbonisation.

Short-term volatility has been a minor issue since the introduction of the MSR. After the European economy came to a halt during COVID-19 lockdowns in 2020, the carbon price dipped a little but quickly rebounded. The carbon price took a toll after Russia’s invasion of Ukraine, dropping to €58 per tonne, but it had recovered to €80 per tonne at the end of March. This dip in prices is of different nature, likely affected by concerns about possible disruption in Russian gas supply to Europe, and expected lower demand for emissions allowances in the event of import bans on fossil fuels.5

But since the energy price spike experienced in Europe in autumn 2021, some member-states, such as Spain and Poland, have been accusing financial investors of causing volatility by speculating about future prices.6 In November 2021, the European Securities and Markets Authority (ESMA) indicated that the number of active parties on the carbon market had increased since 2018, but that the share of transactions on the futures market involving financial institutions had remained low and relatively constant. This did not point to speculation being a major issue, ESMA argued.7 More participants and higher liquidity of the market are more likely to allow energy firms or industry to ‘hedge’ their position, taking out a form of insurance against prices rising faster than anticipated in the future. The in-depth report that ESMA published on March 28th indicated that carbon prices and their volatility seemed in line with market fundamentals. Nonetheless, ESMA suggested that monitoring market participants with buy-and-hold positions is in order, given their currently minor but growing role.8

Tightening the emissions cap is a good start to give clarity on the long-term trajectory of carbon prices. The carbon price has increased considerably in the past year, reaching an all-time high of about €100 per tonne of CO2 in early February 2022 (see Chart 2). At this price, the cost of electricity produced from solar and wind power is already lower than that from gas and coal power plants.9 But that may not be enough to decarbonise industry. The problem is that some industrial processes need high heat that cannot easily be produced from electricity: most low-carbon technologies needed in the steel, chemical and cement sectors will only be economically viable if the price of carbon is higher than €100 per tonne of CO2 in 2030, and up to €400 for some technologies, such as green hydrogen from electrolysis.10

Member-states should swiftly approve the Commission’s proposals to lower the ETS emissions cap and speed up the reduction in the number of permits on the market. If the member-states insist on a slower pace, even steeper emissions cuts will be needed in the future to meet the EU’s 2030 and 2050 emissions goals. Delaying reform of the ETS would also create uncertainty about the long-term trajectory of carbon prices, which could discourage investments urgently needed to drive down emissions. The lifetime of installations like steelworks and cement kilns is around 55 years: this means that investment today has to be green.11

The EU should also impose a gradually increasing price floor in the ETS, which would provide investors with further certainty about where carbon prices are headed, and indicate a benchmark cost of carbon for sectors that currently do not face it.12

But as long as heavy industry is shielded from carbon prices, they can do precious little to prompt decarbonisation.

The EU should accelerate the phase-out of free allowances to heavy industry

Free ETS allowances are granted to heavy industry to prevent job losses associated with ‘carbon leakage’, which happens if polluting businesses move their production from the EU to other countries with no carbon prices, or lower ones, and less stringent environmental regulations. That argument for free permits has some merit: heavy industry is in theory easier to offshore than power generation.

In 2013, heavy industry received 80 per cent of its allowances for free.13 Since then, the allocation of free allowances has been tied to benchmarks which identify the lowest possible carbon emissions for the production of 54 industrial goods. Installations meeting low-emissions, high-efficiency benchmarks receive more free allowances. High-emissions plants, instead, must buy enough permits on the carbon market. The aim is to push industry as a whole to invest in decarbonisation to get closer to sectoral benchmarks. The Commission proposes to introduce more frequent revisions of sector benchmarks, so free allowances are reduced more rapidly as technological progress accelerates, and to make free allocation to industrial players conditional on the green investments they make.

Benchmarks are an improvement on the prior system, which amounted to no-strings-attached freebies. But giving industry free permits is neither efficient nor just, and it translates into unfair extra profit for certain plants. Between 2008 and 2019, energy-intensive industries reaped an estimated €30 to 50 billion in windfall profits.14 In some cases, firms received more free allowances than they needed, which they sold at a profit. In other cases, firms passed on their purported carbon costs to consumers, according to their exposure to competition and other features of the market. Charging consumers for the carbon costs of a product, despite receiving the carbon permit for free, is rational for firms as long as consumers still pay for their products, yet it undermines the fairness of the ETS if it goes beyond preserving production at risk of offshoring.

Handouts of allowances are a ‘free lunch’, the size of which depends on the carbon price – thus, higher carbon prices make free allowances even more valuable. For example, the steel industry estimated that a carbon price of €60 per tonne would require the industry to spend €2.6 billion per year to purchase emissions permits.15 While this is substantial, steel manufacturers currently have to buy only about 20 per cent of their permits to comply with the emissions cap, given that they receive the rest for free.16

Some industrial players argue that higher carbon prices may drive some plants out of business, or force businesses overseas, if their small profit margins are eroded further. This would also mean shedding jobs in Europe. Importantly, costly and urgent investment in decarbonisation may not happen if domestic producers struggle to compete internationally. This is all the more critical in a period of high energy prices, including natural gas, oil and electricity.

In reforming the ETS, the EU has to find the right balance. It needs to ensure carbon prices that are high enough to prompt fast decarbonisation in carbon-intensive industries, and it needs to create a level-playing field between domestic heavy industry and foreign producers who do not face similar costs and regulations.

Rather than subsidising industry with free allowances, the EU should support it by scaling up its support for green innovation and investment.

The EU should focus on creating a level-playing field with foreign competitors through a CBAM

To create a level-playing field, the EU has proposed a carbon border adjustment mechanism (CBAM), which will be piloted between 2023 and 2025, and fully implemented from 2026. That scheme would charge foreign producers of selected ETS goods (cement, iron and steel, aluminium, fertilisers and electricity) a carbon price, derived from the EU’s market price, to export to the EU. This means that both domestic and foreign producers would face the same carbon price when selling to EU customers.

To avoid trade disputes when implementing CBAM, the EU should consult with international trade partners and the WTO. Developing countries are concerned that the financial and bureaucratic costs of CBAM would make exporting to Europe prohibitively expensive for their industry. The CER has suggested solutions to address this concern, particularly using CBAM revenues to support decarbonisation efforts in least developed countries.17

At the same time, some industrialised countries are likely to be hostile to the measure. Non-European G20 countries made firmer commitments on climate action in the run-up to the Glasgow COP26 climate conference, but not all are committed to carbon prices. For example, the United States pledged to halve its greenhouse gas emissions by 2030 relative to 2005 levels, and is considering its own version of a CBAM – though it remains unclear how that would be designed given there is no US-wide federal carbon price.

Once CBAM is fully operational, there would be no need to shield European industry from international competitors by giving them free ETS allowances. That is why the Commission proposes to combine CBAM with the gradual phase-out of free emission allowances for heavy industry between 2025 and 2036, when they will be entirely eliminated in CBAM-covered sectors. The 2036 sunset date is not sufficiently ambitious: 2030 would be more appropriate, in line with the goal to curb EU emissions by 55 per cent by 2030 relative to 1990 levels.

The EU also needs to strike a balance in how the costs of decarbonisation are shared between households and businesses: delaying the full exposure of heavy industry to carbon prices to 2036 would be politically difficult, given that the introduction of EU-wide carbon prices in consumer-oriented sectors such as road transport and buildings is proposed to take place in 2026. Once CBAM is implemented, all carbon allowances should be auctioned rather than given out for free, in order to avoid double protection of heavy industry.

Some businesses argue that phasing out free allowances would endanger profits and jobs. With CBAM in force, and without free allowances, some European exporters fret that they will be forced to charge prices that are higher than world prices, and EU companies will lose competitiveness internationally. One solution could be export subsidies, but these are inefficient too, and would fall foul of WTO rules. Rather than subsidising industry with free allowances, the EU should support it by scaling up its support for green innovation and investment.

ETS revenues should be used to support low-carbon innovation

Since its inception, the ETS has worked best at promoting innovations that were close to being profitable rather than encouraging ‘moonshot’ innovations, which require more substantial R&D budgets.18 For example, carbon prices have helped replace coal power plants with gas and renewables. But it was substantial subsidies for renewable energy that initiated the boom of solar and wind in Europe in the first place. Those subsidised investments brought down the costs of renewable technologies substantially, and made them much more competitive with fossil-based power generation. Carbon prices then did the rest. Learning from this experience, the EU should directly support heavy industry investment in decarbonisation.

Increasing public investment for R&D and for commercial deployment of low-carbon industrial technologies would amount to transferring some of the risks and costs of innovation investment from industry to taxpayers. The rationale for this type of intervention is similar to that of public support for vaccine development: the benefits of those inventions do not all accrue to the innovators but to society more broadly, and as a result, the private sector may not invest enough in innovation without public money.

The Commission’s proposal to devote the entirety of the ETS revenues that member-states receive to climate investment goes in the right direction – but more of that should go towards innovation.

The EU directly supports investment in industrial decarbonisation with the Innovation Fund, introduced in 2020 and funded through ETS revenues. The Innovation Fund will absorb ETS revenues from the auction of 450 million allowances between 2020 and 2030 (valued at over €40 billion at the current carbon market price). The Fit for 55 package aims to increase this by another 200 million allowances (50 million from the current ETS, and 150 from the proposed new ETS covering buildings and road transport). Demand for innovation funds is high: the first round of proposals bidding for Innovation Fund cash far exceeded the amount of money on offer.19 While the value of the fund will increase as carbon prices rise, more investment support to speed up the transition of heavy industry is needed. The Commission’s proposal to devote the entirety of the ETS revenues that member-states receive to climate investment goes in the right direction – but more of that should go towards innovation.

Most green technologies for heavy industry are not financially viable at the current carbon price and will be more expensive than their ‘brown’ counterparts for some time. In order to speed up their market deployment, comparable to the successes in renewable power generation, the Commission wants to use the Innovation Fund to finance ‘carbon contracts for difference’ (CCfDs).20

CCfDs give innovators a guaranteed carbon price to work with. Industrial firms will only invest in a new green production method if they expect carbon prices to be sufficiently high to make it viable. This is where public institutions should provide a guaranteed future carbon price through CCfDs. If the market price is below that fixed price when the contract expires, the firm receives the difference. This contract reduces the risks that industry faces when investing in emerging, costly decarbonisation technology. As CCfDs are potentially expensive for governments, not all may be ready to bear the fiscal risk. Hence it is a good idea for the EU to fund these contracts via the Innovation Fund, and for an EU-wide institution to be the counterpart of investors in such contracts, particularly as CCfDs would finance industrial innovation of common interest to all member-states.

All these proposed changes to the ETS and to the use of its revenues are necessary to ensure that, from now on, carbon prices push industry to build or upgrade plants only if they are compatible with net-zero emissions. Carbon-intensive plants would lead to unsustainably high emissions, and risk quickly becoming liabilities, taking a toll on the competitiveness of EU business. Heavy industry must urgently move away from business-as-usual.

How to make the new ETS work for consumers

Under the Commission’s proposals, in 2026 the EU’s new ETS (let us call it ‘ETS2’) would cap emissions from road transport and buildings and gradually tighten the cap year by year. Intermediaries such as companies selling fuel for cars and heating (as opposed to final consumers such as households and businesses) would be required to show compliance with regulation by buying pollution permits.

As discussed, in the existing ETS, heavy industry receives some permits for free. Conversely, in ETS2 there will be no freebies: all permits would be auctioned. This is because there is no reason to think that households would leave the EU due to carbon pricing.

The behavioural impacts of carbon pricing

Under the new system, fuel retailers will largely pass the carbon price onto their customers, so final consumers will face higher prices for fossil fuels for transport and heating. But, while commercial consumers like shopkeepers might be able to pass on higher energy costs at least partly by raising their own prices, households will not be able to do that.

Both transport and heating are essential needs, but different people meet those needs in different ways. Some cycle and have a heat pump, others drive a car to work and still burn oil at home. How households respond to an energy price increase will thus differ. In cities there are plenty of options to move around – walking and cycling, public transport, private cars or scooters. If the price of motor fuel increased due to carbon pricing, city dwellers could quickly adjust their behaviour by shifting to other means of transportation. Sparsely populated areas, on the other hand, often have fewer transport alternatives. Driving a private car is much more convenient in some rural and suburban areas, so households there are more vulnerable to fuel price increases than their urban counterparts.

Governments are subsidising insulation and electric cars, but in the short-term, vulnerable energy consumers will feel the pain.

For these reasons, fuel demand weakly responds to price increases (or, as economists say, is inelastic): as the price of gasoline at the pump goes up by 1 per cent, gasoline demand drops less than proportionally, by only about 0.3 per cent in the short term (immediate response, up to one year after the price increase) and by 0.8 per cent in the long term (beyond one year after). Demand for heating fuels is even less responsive: when natural gas prices increase by 1 per cent, gas demand drops only by an estimated 0.2 per cent in the short run and 0.7 per cent in the long run.21 Households could respond to price increases by lowering their thermostat or limiting heating time. But without support to help consumers cope with higher prices, carbon pricing could cause a political backlash against decision-makers and possibly climate action more broadly.

The main aim of carbon pricing is to reduce emissions – but the way in which these emissions cuts are achieved matters politically. In road transport, higher fuel prices should encourage drivers to opt for electric vehicles and bikes instead of cars with combustion engines. Infrastructural changes are also necessary to make behaviour change feasible: in urban areas, more public transport and bike lanes could reduce dependence on private vehicles; in rural areas, if viability of public transport is a challenge, charging infrastructure for electric vehicles will be critical. In the buildings sector, carbon pricing aims to encourage investment in energy efficiency, including better insulation and a shift from fossil fuels to more efficient electric heating.

Governments are subsidising insulation and electric cars, but transformative renovations in buildings and new transport infrastructure take time, meaning that in the short term, vulnerable energy consumers will feel the pain.

The distributional impacts of carbon pricing

Carbon prices have a larger impact on lower-income households, on households living in energy-inefficient buildings with carbon-intensive heating systems and on users depending on fossil-fuelled vehicles. These categories can overlap, but need not necessarily – a lower-income household living in a small apartment in an urban setting may be less affected than a middle-income household living in an old house in a rural area.

The most commonly used types of heating fuel vary across the EU – as does their carbon intensity. In Poland, for example, coal provides over 40 per cent of residential space heating; oil and petroleum products are the main energy source for space heating in Ireland, Greece and Cyprus; and natural gas is the main space heating source for another 8 member-states, including Germany, France and Italy.22

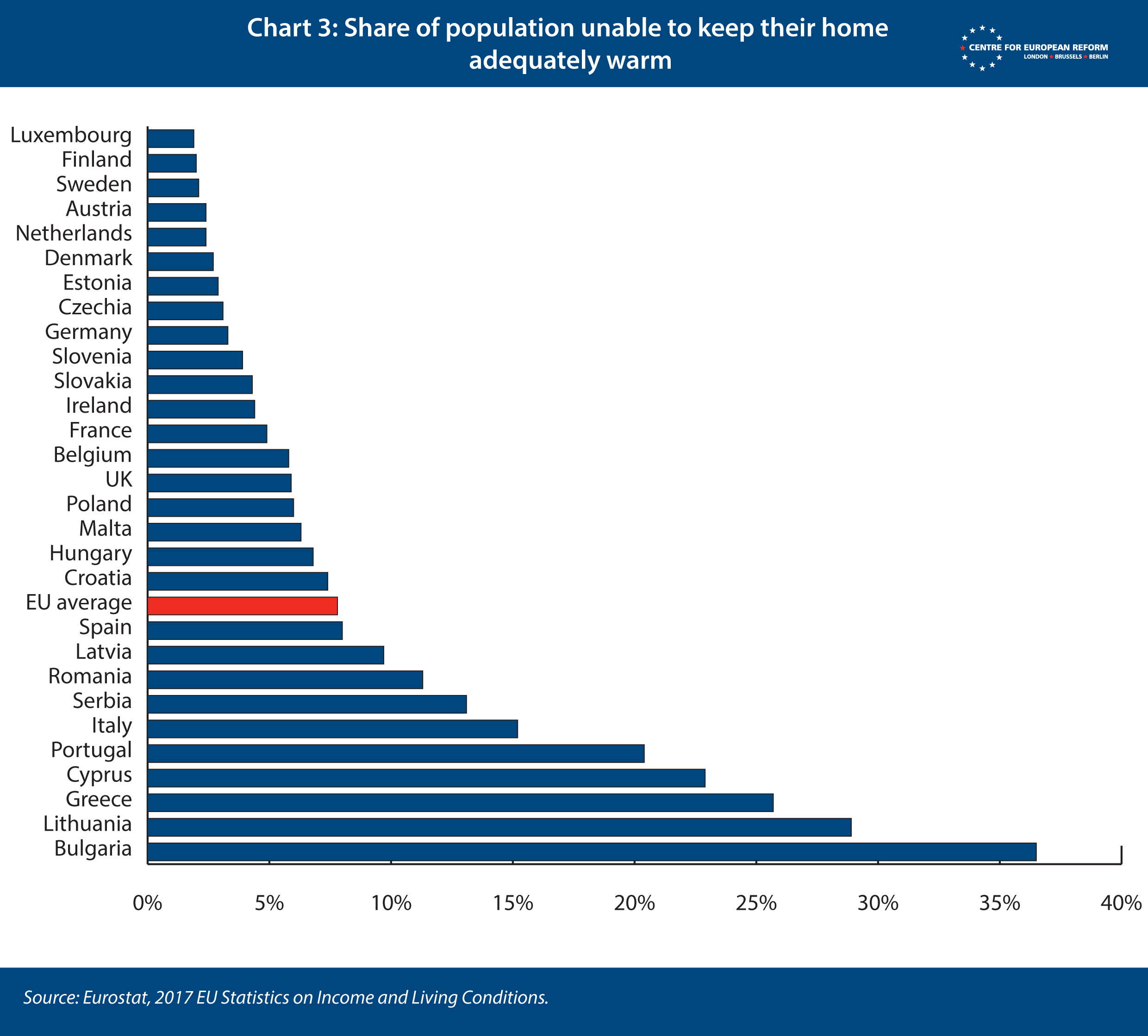

Energy poverty affected 31 million Europeans in 2019,23 and this will have increased recently because of the unprecedented spikes in gas prices.24 While on average, 7.8 per cent of the EU population was not able to adequately heat their home in 2017, the share in poorer countries was higher (Chart 3). Energy poverty also varies across urban and rural areas, and in 11 EU countries, including France, Hungary and Romania, the difficulty in keeping homes warm was higher in sparsely populated areas than in densely populated ones.25

Transport poverty is also a multifaceted problem, with some people unable to afford any transport (owning a car or paying public transport fees), while others living in remote areas or peripheral urban neighbourhoods have no access to public transport services.26 About 40 per cent of the EU population in rural areas has difficulties accessing public transport. Only 20 per cent of those living in towns or suburbs and 10 per cent of those living in cities encounter the same problem (Chart 4).

Mitigating the distributional impacts of carbon pricing

An EU-wide carbon price created by ETS2 would have different impacts across the Union because of differences in per capita income levels, dependence on private vehicles and the carbon intensity of heating. On its own, carbon pricing on road transport and building heating would be regressive, meaning that it would hit the poorest worst. But if the EU makes good use of the revenues raised by pricing carbon emissions, it could turn ETS2 into a progressive policy, benefitting more vulnerable households and businesses.

If the EU makes good use of the revenues raised by pricing carbon emissions, it could turn the new ETS on road transport and buildings into a progressive policy, benefitting more vulnerable households and businesses.

There are several ways to redistribute carbon pricing revenues. Switzerland, for example, gives two-thirds of its carbon tax revenues back to households and businesses, while the remaining third is earmarked for green investment. After introducing carbon pricing, Sweden lowered the level of income taxes and social security contributions.27

The Commission’s proposal for ETS2 wants to earmark part of the ETS2 revenues for a Social Climate Fund (SCF), which would be used to finance temporary income support measures (like cash transfers to households, or vouchers for energy bills). It would also provide investment subsidies for households and businesses to adopt green transport and heating technologies, such as building renovations, heat pumps and low-carbon transport. The Fund would target specific social groups at risk of transport and energy poverty, as opposed to the entire EU population: vulnerable consumers, transport users and micro-enterprises.

The fund would start operating in 2025, one year before the proposed entry into force of the ETS2, financed by anticipating the auctions of emissions permits. To access funds, member-states would need to prepare social climate plans, which the Commission would assess and approve. Plans would need to detail the specific measures and investments they aim to finance, as well as milestones and targets for implementation by 2032. The plans would also need to provide regional estimates of the effects of ETS2 on households and micro-enterprises.

The SCF would receive 25 per cent of revenues from ETS2 over its 2025-2032 budget cycle, for an estimated €72 billion. Under the proposal, member-states are required to match that amount, contributing at least half of the estimated costs of their social climate plans, including by auctioning allowances under the new cap and trade scheme: this would bring the fund to an estimated €144 billion. Under the SCF, transfers would be paid out to countries according to a set of criteria such as income per capita; the share of the population at risk of poverty, with particular attention to rural areas; the carbon intensity of households’ heating options; and energy poverty indicators such as the share of the population with arrears on utility bills.

The EU’s proposal is a good start, but does not go far enough in compensating vulnerable households and businesses.

All ETS2 revenues should be devoted to the Social Climate Fund. Under the European Commission’s proposal, the SCF would be given 25 per cent of ETS2 auction revenues, while the remaining 75 per cent would go to member-states who would be obliged to finance climate and energy projects with the money. However, this does not ensure that funds go to vulnerable energy consumers. All ETS2 revenues, and not only 25 per cent, should be devoted to the Social Climate Fund. This would bring the SCF to an estimated €288 billion over 2025-2032, or €36 billion per year – though this would vary according to the carbon price. Member-states should contribute to the SCF to cover part of the costs of their social climate plans via their national budget, but poorer member-states should contribute less than 50 per cent of the total costs, and richer ones more (as opposed to the Commission’s proposal that all countries pay 50 per cent).28

If carbon prices reached €80 per tonne in 2030, estimated EU-wide carbon costs for households could amount to €633 billion between 2025 and 2040,29 or about €40 billion per year. A larger SCF would provide income support to more households, and it would help more energy consumers reduce their dependence on fossil fuels. For example, €275 billion per year is needed in additional building renovation investment to meet EU 2030 climate goals:30 the SCF would ensure that poorer households get help insulating their homes.

The Social Climate Fund should start as soon as possible. It is crucial that investment support via the SCF is frontloaded, so that it starts providing subsidies for green transport and heating to poorer households well before the ETS2 starts to bite. The current Commission proposal aims for the Fund to go live in 2025, but the quick launch of the Recovery and Resilience Facility tells us that the EU can be speedier than that. The SCF should start operating as soon as possible. That would allow EU member-states to redistribute the costs of addressing the continuing energy crises, which has only been made more acute by the ripples that Russia’s invasion of Ukraine has been sending through global energy markets. An earlier start of the SCF would give poorer Europeans more time to invest in reducing fossil fuel consumption before ETS2 starts: given high energy prices, demand for energy efficiency should be encouraged.

The SCF could start as soon as possible, financed with EU joint borrowing and, later, revenues from auctions of emissions permits once ETS2 starts operating. And the SCF should continue beyond 2032, the date the Commission proposes it should end, to help households and businesses decarbonise to 2050.

The quick launch of the recovery fund tells us the EU can be speedy: the Social Climate Fund should start as soon as possible.

The EU should clearly communicate that all revenues from ETS2 are devoted to supporting citizens and businesses in the green energy transition. The Social Climate Fund’s aims are sensible, but it is important that people know that it is there to help them. Making SCF transfers visible is fundamental, as is ensuring that consumers understand their connection to the ETS2 and to carbon prices. Without clarity on this link, popular support for carbon pricing may falter.

Transfers could be either unconditional or specifically aimed at relieving pressure on energy and fuel expenditures, such as energy vouchers. However, vouchers specifically tied to fuel expenses for driving or heating may dampen the incentive to reduce such fuel consumption. Making SCF transfers unconditional would be better, so that vulnerable households are free to spend them as they wish.

The new ETS should be designed to avoid excessive carbon price fluctuations. Cap and trade systems target a specific level of emissions, but that means that prices for emissions permits can fluctuate. The ETS2 proposal includes the idea of a ‘market stability mechanism’ to stabilise the price, just as it was introduced in the original ETS. It is a good way to prevent short-lived carbon price spikes, but it is not suitable for large price fluctuations. If such fluctuations were to happen, final consumers would feel the burden: unlike businesses exposed to the existing ETS, households cannot hedge their exposure to carbon prices.

Instead of the market stability mechanism, the EU should introduce a price corridor, to give households some certainty on the band within which carbon prices will be in the future.31 Concretely, it would amount to establishing a floor and a ceiling for the carbon price: if the market price stepped outside this corridor, the market stability mechanism would intervene. This resembles the German emissions trading system for road transport and buildings: when the system started in 2021, German ETS permits were sold at set prices of €25 per tonne of carbon.32 The set price will increase to €55/tonne by 2025, and in 2026 emission permits will be auctioned within a price corridor of €55 to €65/tonne.

All policies concerning road transport and buildings should be aligned with climate targets: carbon pricing is a piece of the puzzle. Largely unpriced carbon emissions are not the only market failure preventing decarbonisation in road transport and buildings. While energy taxes vary widely across EU member-states and between fuels,33 in most member-states existing energy taxes favour fossil fuels such as natural gas instead of electricity: tax levels inconsistent with climate goals blur the price signals that consumers see in their bills and at the pump, ultimately discouraging efficiency investment.34

The EU should ensure that both new carbon prices and existing energy taxes on heating and transport fuels encourage decarbonisation. Energy taxes are set at national level, but the EU is reviewing its energy taxation directive and should use that opportunity to increase minimum tax levels and ensure that they are set according to carbon content.

Finally, market-based policy instruments such as carbon prices and energy taxes are only one part of the many policy measures needed for decarbonisation of road transport and buildings. Regulations such as vehicle emissions standards and energy efficiency building standards are also needed. Just as vehicle emissions standards will mandate an end to internal combustion engines in 2035, there should be a sunset date for fossil-fuel heating of buildings.

Carbon prices are more important after Putin’s invasion, not less

The extension of carbon pricing under ETS2 will raise heating and fuel bills at a time when consumers are struggling with high energy prices. The phase-out of free allowances will fully expose energy-intensive heavy industry to the price of carbon. So why is carbon pricing still a good idea?

In a policy document published in October 2021, the Commission argued that the spike in energy prices would be temporary, and that a faster transition from fossil fuels to renewables would be the best antidote to high energy prices.35 Vladimir Putin’s invasion of Ukraine has accelerated the energy transition agenda. The Commission has proposed that the EU cut Russian gas imports by two-thirds by the end of 2022, and fully phase out all energy imports from Russia (including gas, oil and coal) by 2027. This will be challenging, given the EU’s dependency on Russian energy imports (in 2019, 41, 27 and 47 per cent of EU imports of gas, oil and coal came from Russia).36 In some countries this dependency is even higher: about half of natural gas imports to Germany and Italy come from Russia, while this is above 75 per cent for member-states such as Bulgaria, Hungary and Austria.37 Finding substitutes for all energy imports from Russia will be expensive and take time. Meanwhile, prices of fossil energy may remain substantially higher than pre-2021 levels for the foreseeable future.

Higher carbon prices are needed to strengthen incentives to cut emissions – for example by reducing energy consumption, shifting from fossil fuels to renewables for electricity generation.

But this is not a reason to freeze plans to make EU carbon prices bite harder and to expand emissions trading to more sectors of the economy. Higher carbon prices are needed to strengthen incentives to cut emissions – for example by reducing energy consumption, shifting from fossil fuels to renewables for electricity generation, and electrifying processes that would otherwise require fossil fuels. Additionally, many ETS emissions permits are auctioned (although not enough of them), bringing in revenues that governments can re-invest in the energy transition. Part of the revenues from the existing ETS go towards funds for green innovation and for the modernisation of power systems. The Commission wants some of the revenues from ETS2 to go to the Social Climate Fund. This fund would be distributed among member-states to help vulnerable consumers with higher energy bills, and to finance subsidies for green investment by households and businesses – such as building renovations, installation of heat pumps, and replacement of combustion engine cars with electric vehicles and bikes.

Quitting Russian fossil fuels will mean moving to more carbon-intensive alternatives such as coal in the short term – carbon prices are particularly important because they will help to ensure this shift is only temporary, not the new normal. In the past few months, lower Russian gas pipeline imports have partially been replaced by higher imports of liquefied natural gas,38 and by coal to power electricity generation.39 Switching away from gas might help to keep European industry going and avoid larger cuts to energy demand, but Europe is very dependent on Russian oil and coal as well. While still expensive due to increased competition with other fuel buyers, sourcing alternatives to Russian oil and coal would be somewhat easier than Russian gas, given that global markets for these commodities are more fluid.40 Swift approval of reforms of the ETS and implementation of ETS2 would provide the necessary certainty for investors to plan ahead and increase investment in renewables and energy efficiency.

EU member-states need to act on two fronts – both demand and supply of energy – and on two timescales. They must reduce fossil fuel imports from Russia as rapidly as possible, even if that means procuring more polluting fossil fuels in the short term. At the same time, they must keep their eyes firmly anchored on 2030 and 2050 climate goals. On the supply side, governments should immediately facilitate accelerated investments in renewable energy, but also in waste-based biogas and in green hydrogen. On the demand side, they should encourage energy efficiency improvements and the use of low-carbon solutions such as electric vehicles and heat pumps, to cut consumption of oil and gas. Both supply and demand measures are critical to reducing dependence on Russia. Carbon prices are the most efficient way to incentivise both types of measures – but they are also politically difficult.

Governments might be tempted to shield consumers from high energy prices. In its ‘RepowerEU’ communication of March 8th, the European Commission highlighted that governments could temporarily cut energy taxes and cap electricity retail prices. Many EU governments have already cut VAT and energy taxes since the October price spike,41 and are now doubling down on similar measures to limit price increases of both electricity and fuel at the pump.42 But artificially limiting energy prices amounts to providing fossil fuel subsidies and would dim the incentive to reduce energy consumption that high prices provide. Europe needs to adjust to a period of higher and more volatile energy prices – fossil fuel subsidies are neither helpful for decarbonisation nor tenable for public budgets. Instead, governments should give unconditional transfers to consumers, making them more generous for the most vulnerable. That way, high energy prices will encourage households and businesses to reduce energy and fuel consumption and invest in energy efficiency, while cash transfers will allow those who can’t afford to do so to pay their bills. Support for energy efficiency investment, already a priority of the Recovery Fund, should first and foremost address poorest households, who otherwise would find it difficult to renovate or heat their homes.

Leaving carbon unpriced is not just: carbon pricing is a tool to make climate action equitable, by making polluters pay and using revenues to help the most vulnerable reduce their dependence on fossil fuels.

Pausing efforts to expand the coverage of European carbon prices is the wrong way to go about this energy crisis. The EU should keep its carbon pricing plans, reforming the existing ETS by swiftly removing free allowances while a carbon border adjustment mechanism is introduced, and creating the ETS2 to cover road transport and buildings, backed up with the SCF. Given the urgency of redistributing the cost impacts of the energy crisis, compounded by the war in Ukraine, it would make sense to bring forward the implementation of the SCF. This fund could start as soon as possible, financed with EU joint borrowing and, later, revenues from auctions of emissions permits.

Critiques of extending emissions trading to consumer-oriented sectors such as buildings and road transport complain about the distributional impacts of higher energy prices. That is a valid critique, but fails to recognise that making good use of revenues from ETS2 would make the scheme progressive.43 Leaving carbon unpriced is not just: it just lets polluters continue emitting carbon for free, ignoring the disparity of the implications of climate change.

There will be winners and losers from climate action. To be successful, the Green Deal needs to support both consumers and industry in reducing their consumption of fossil fuels, and carbon prices nudge them to do so. It also needs to help poorer member-states replace older energy infrastructure, in order to shift away from coal dependence.

In the industrial sector, the winners from climate action are low-carbon activities – renewables, electric vehicles manufacturing, recycling – whereas the losers are carbon-intensive ones – fossil fuel extraction and refinery, the traditional (internal combustion engine) automotive sector. Among businesses, small and medium-sized enterprises may lack the credit needed to invest in cutting fossil fuel use. Because of the regional clustering of these industries, some regions will suffer more throughout the energy transition, and will need to rethink their economic model.

Among citizens, higher carbon prices would hit the incomes of lower-income households harder, especially those living in poorly insulated buildings and with no other transport options to driving a car. But in Europe, per capita emissions from the top 10 per cent of the income distribution (about 30 tonnes of CO2 equivalent per person in year 2019) are three times larger than emissions from the middle 40 per cent, and six times larger than for the bottom 50 per cent. And on a macro level, half of global CO2 emissions are generated by the top 10 per cent of emitters – whereas the bottom 50 per cent of emitters only generate 12 per cent of emissions. Europe’s average per capita emissions are about half of North America’s average – but 6 times as large as Sub-Saharan Africa’s average.44 Higher-income countries are more responsible for historical and current emissions, yet the impact of climate change will disproportionately be borne by more vulnerable people and regions, according to the IPCC.45

Rather than scaling back plans to strengthen European emissions trading, the EU should move towards pricing all carbon emissions, and use revenues from auctions of emissions allowances to address the distributional impact. Carbon pricing is a tool to make climate action equitable, by making polluters pay and using revenues to help the most vulnerable reduce their dependence on fossil fuels.

Conclusion

The EU needs to accelerate the decarbonisation of its economy to meet its 2030 emissions reduction goals. In the wake of Russia’s invasion of Ukraine, it also needs to do it in order to reduce its dependence on fossil fuels from Russia – Europe’s largest external supplier of coal, natural gas and crude oil.

The Commission’s proposed changes to the EU ETS point in the right direction, but they are neither sufficient on their own nor speedy enough to accelerate the decarbonisation of heavy industry to meet its 2030 emissions reduction goals. To hit those targets, the EU needs to ensure a high and stable carbon price and eliminate free emissions permits sooner. But the Union should also move quickly to create a level-playing field with foreign competitors and use ETS revenues to support investment in low-carbon innovation.

The Commission’s proposed creation of a new ETS to cover road transport and buildings would cap ever-increasing transport emissions and speed up efficient building renovations. But to offset the distributional impacts of higher energy and fuel prices, all revenues from the auctioning of emissions permits under ETS2 should be devoted to a Social Climate Fund. The EU should clearly communicate both the origin and the purpose of the SCF to households and businesses.

Carbon prices are not the only policy the EU needs in order to cut its emissions and meet its climate targets. All policies relating to ETS-covered sectors should be aligned with climate targets: reform of the energy taxation directive is fundamental to removing implicit energy subsidies (such as those for aviation) and to ensuring that electricity is not at a disadvantage relative to fossil fuels. But the ETS is the cornerstone of EU climate policy, and its strengthening and expansion are necessary to reach 2030 and 2050 emissions reductions targets.

2: European Environment Agency, ‘Greenhouse gases - data viewer’, April 13th 2021.

3: ICE data on prices of futures contracts for natural gas on the Dutch Title Transfer Facility. Markets Insider data on prices of Brent crude oil.

4: ‘Opposition to second EU ETS deepens, as divisions emerge among largest political group’, Carbon Pulse, March 3rd 2022. ‘High energy costs intensify debate over EU plan to decarbonise heating and transport’, Euractiv with Reuters, March 18th 2022.

5: ESMA, ‘Final report. Emission allowances and associated derivatives’, March 28th 2022.

6: ‘Europe’s energy price hike fuelled by speculators, Spain and Poland say’, Euractiv, November 25th 2021.

7: ESMA, ‘Preliminary report. Emission allowances and derivatives thereof’, November 15th 2021.

8: ESMA, ‘Final report. Emission allowances and associated derivatives’, March 28th 2022.

9: Lazard, ‘Levelized cost of energy, levelized cost of storage, and levelized cost of hydrogen’, October 28th 2021.

10: Agora Energiewende and Wuppertal Institute, ‘State of play of the industry transition in Europe’, webinar slides, June 1st 2021.

11: Agora Energiewende and Wuppertal Institute, ‘Breakthrough strategies for climate neutral industry in Europe: Policy and technology Pathways for raising EU climate ambition’, April 2021.

12: Maria Demertzis and Simone Tagliapietra, ‘Carbon price floors: An addition to the European Green Deal arsenal’, Bruegel, March 4th 2021.

13: European Commission, ‘Allocation to industrial installations’, webpage last accessed on March 30th 2022.

14: CE Delft, ‘Additional profits of sectors and firms from the EU ETS 2008-2019’, May 2021.

15: ‘Scholz’s top Europe aide to hit ground running’, Financial Times, December 9th 2021.

16: Eurofer, ‘Making sense of EU climate policy’, webinar, March 17th 2021.

17: Elisabetta Cornago and Sam Lowe, ‘Avoiding the pitfalls of an EU carbon border adjustment mechanism’, July 5th 2021.

18: Johanna Lehne and others, ‘The EU ETS: from cornerstone to catalyst. The role of carbon pricing in driving green innovation’, April 2021.

19: European Commission, ‘Speeding up European climate action towards a green, fair and prosperous future’, November 2021.

20: Oliver Sartor and Chris Bataille, ‘Decarbonising basic materials in Europe: How Carbon Contracts-for Difference could help bring breakthrough technologies to market’, IDDRI, October 2021.

21: Xavier Labandeira and others, ‘A meta-analysis on the price elasticity of energy demand’, Energy policy, March 2017.

22: Eurostat data, ‘Disaggregated final energy consumption in households – quantities’.

23: European Commission, ‘State of the Energy Union 2021 – Contributing to the European green deal and the Union’s recovery’, October 26th 2021.

24: Ian Bond, Elisabetta Cornago and Zach Meyers, ‘Why have Europe’s energy prices spiked and what can the EU do about them?’, October 28th 2021.

25: Energy Poverty Observatory, Indicators and data.

26: Civitas, ‘Transport poverty’, Civitas thematic policy note, October 2016.

27: World Bank, ‘Using Carbon Revenues’, August 2019.

28: Camille Defard and Karin Thalberg, ‘An inclusive social climate fund for the just transition’, Jacques Delors Institute, January 2022.

29: Magdalena Maj and others, ‘Impact on households of the inclusion of transport and residential buildings in the EU ETS’, Polish Economic Institute, June 2021.

30: European Commission, ‘A renovation wave for Europe - greening our buildings, creating jobs, improving lives’, October 14th 2020.

31: Ottmar Edenhofer and others, ‘A whole-economy carbon price for Europe and how to get there’, Bruegel, June 2021.

32: ICAP, ‘German national emissions trading system’, International Carbon Action Partnership, last updated on November 17th 2021.

33: European Commission, ‘Energy prices and costs in Europe’, October 14th 2020.

34: Samuel Thomas, Louise Sunderland and Marion Santini, ‘Pricing is just the icing: The role of carbon pricing in a comprehensive policy framework to decarbonise the EU buildings sector’, Regulatory Assistance Project, June 2021.

35: European Commission, ‘Tackling rising energy prices: A toolbox for action and support’, October 13th 2021.

36: Eurostat, ‘From where do we import energy?’.

37: Eurostat, ‘Energy trade’.

38: Ben McWilliams, Giovanni Sgaravatti and Georg Zachmann, ‘European natural gas imports’, Bruegel Datasets, updated on March 29th 2022.

39: European Commission, ‘Quarterly report on European electricity markets, Q3 2021’.

40: Ben McWilliams and others, ‘Can Europe manage if Russian oil and coal are cut off?’, Bruegel, March 17th 2022.

41: Giovanni Sgaravatti, Simone Tagliapietra and Georg Zachmann, ‘National policies to shield consumers from rising energy prices’, Bruegel dataset, updated on March 19th 2022.

42: ‘EU to subsidise household fuel prices surging amid Ukraine crisis’, Euractiv with Reuters, March 16th 2022.

43: Tim Gore, ‘Can polluter pays policies in the buildings and transport sectors be progressive? Assessing the distributional impacts on households of the proposed reform of the Energy Taxation Directive and extension of the Emissions Trading Scheme’, IEEP, March 2022.

44: Lucas Chancel and others, ‘World inequality report 2022’, World Inequality Lab, December 2021.

45: IPCC, ‘Climate change 2022: Impacts, adaptation, and vulnerability. Contribution of Working Group II to the sixth assessment report of the Intergovernmental Panel on Climate Change’, February 2022.

Elisabetta Cornago is a senior research fellow at the Centre for European Reform.

April 2022

This paper is published in partnership with the Open Society European Policy Institute.

View press release

Download full publication